Electronic Arts 2011 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2011 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

Annual Report

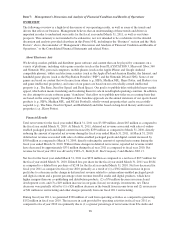

digital products, which have higher margins than our co-publishing and distribution products, (2) the timing of

payments related to our inventory purchases, (3) our cost reduction initiatives, including decreases in external

development and contracted services, and (4) lower marketing and advertising spend as a result of a decrease in

the number of titles released as compared to the prior year.

Trends in Our Business

Digital Content Distribution and Services. Consumers are spending an ever-increasing portion of their money

and time on interactive entertainment that is accessible online, or through mobile digital devices such as smart

phones, or through social networks such as Facebook. We provide a variety of online-delivered products and

services. Many of our games that are available as packaged goods products are also available through direct

online download through the Internet. We also offer online-delivered content and services that are add-ons or

related to our packaged goods products such as additional game content or enhancements of multiplayer

services. Further, we provide other games, content and services that are available only via electronic delivery,

such as Internet-only games and game services, and games for mobile devices.

Advances in mobile technology have resulted in a variety of new and evolving devices that are being used to play

games by an ever-broadening base of consumers. We have responded to these advances in technology and

consumer acceptance of digital distribution by offering different sales models, such as subscription services,

online downloads for a one-time fee, and advertising-supported free-to-play games and game sites. In addition,

we offer our consumers the ability to play a game across platforms on multiple devices. We significantly

increased the revenues that we derive from online-delivered products and services from $432 million in fiscal

year 2009, to $522 million in fiscal year 2010 and $743 million in fiscal year 2011 and we expect this portion of

our business to continue to grow in fiscal 2012 and beyond.

Wireless and other Emerging Platforms. Advances in technology have resulted in a variety of platforms for

interactive entertainment. Examples include wireless technologies, streaming gaming services, and Internet-

connected televisions. Our efforts in wireless interactive entertainment are focused in two areas – games for

handheld game systems and downloadable games for mobile devices. These platforms grow the consumer base

for our business while also providing competition to existing established video game platforms. We expect sales

of games for wireless and other emerging platforms to continue to be an important part of our business.

Concentration of Sales Among the Most Popular Games. We see a larger portion of packaged goods games

sales concentrated on the most popular titles, and that those titles are typically sequels of prior games. We have

responded to this trend by significantly reducing the number of games that we produce to provide greater focus

on our most promising intellectual properties from 67 primary titles in fiscal year 2009 to 54 in fiscal year 2010

and 36 primary titles in fiscal year 2011. In fiscal year 2012, we expect to release approximately 22 primary

titles. Consequently, we have decreased the number of games that we distribute, which have lower margins, as

well as reduced our exposure to the declining music games genre.

Catalog Sales. The video game industry is experiencing a change in retail sales patterns, which is decreasing

revenue from catalog sales (sales of games in the periods following the launch quarter). Currently, many console

games experience sales cycles that are shorter than in the past. To mitigate this trend, we offer our consumers a

direct-to-consumer service (such as “head-to-head” play or other multiplayer options) and/or additional content

available through online services to further enhance the gaming experience and extend the time that consumers

play our games after their initial purchase. We anticipate that in some cases these additional online services will

also generate revenue to mitigate the effect of reduced catalog sales.

Used Games. Some retailers sell used video games, which are generally priced lower than new video games

and do not result in revenue to the publisher of the games from the sale. We have observed that the market for

used video games has been growing. If retailers continue to increase their sales of used video games, it could

negatively affect our sales of new video games and have an adverse impact on our operating results.

29