Electronic Arts 2011 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2011 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

Annual Report

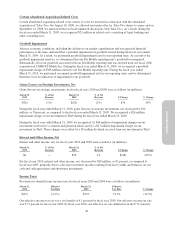

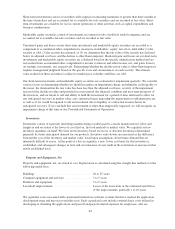

potential changes in interest rates. The modeling technique estimates the change in fair value from immediate

hypothetical parallel shifts in the yield curve of plus or minus 50 basis points (“BPS”), 100 BPS, and 150 BPS.

Valuation of Securities

Given an Interest Rate

Decrease of X Basis Points

Fair Value

as of

March 31,

2011

Valuation of Securities

Given an Interest Rate

Increase of X Basis Points

(In millions) (150 BPS) (100 BPS) (50 BPS) 50 BPS 100 BPS 150 BPS

Corporate bonds .................... $258 $257 $255 $253 $252 $250 $249

U.S. Treasury securities .............. 126 125 124 124 123 122 121

U.S. agency securities ................ 104 103 103 102 101 101 100

Commercial paper .................. 18 18 18 18 18 18 18

Total short-term investments ........ $506 $503 $500 $497 $494 $491 $488

The following table presents the hypothetical changes in the fair value in our short-term investment portfolio as

of March 31, 2010, arising from selected potential changes in interest rates.

Valuation of Securities

Given an Interest Rate

Decrease of X Basis Points

Fair Value

as of

March 31,

2010

Valuation of Securities

Given an Interest Rate

Increase of X Basis Points

(In millions) (150 BPS) (100 BPS) (50 BPS) 50 BPS 100 BPS 150 BPS

Corporate bonds .................... $237 $236 $234 $233 $231 $229 $228

U.S. agency securities ............... 117 116 115 115 114 114 113

U.S. Treasury securities .............. 85 85 84 83 83 82 82

Commercial paper .................. 1 1 1 1 1 1 1

Total short-term investments ........ $440 $438 $434 $432 $429 $426 $424

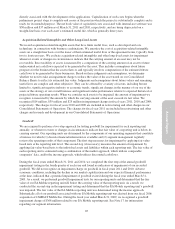

Market Price Risk

The fair value of our marketable equity securities in publicly traded companies is subject to market price

volatility and foreign currency risk for investments denominated in foreign currencies. As of March 31, 2011 and

2010, our marketable equity securities were classified as available-for-sale securities and, consequently, were

recorded on our Consolidated Balance Sheets at fair market value with unrealized gains or losses resulting from

changes in fair value reported as a separate component of accumulated other comprehensive income, net of tax,

in stockholders’ equity. The fair value of our marketable equity securities as of March 31, 2011 and 2010 was

$161 million and $291 million, respectively.

Our marketable equity securities have been, and may continue to be, adversely impacted by volatility in the

public stock markets. At any time, a sharp change in market prices in our investments in marketable equity

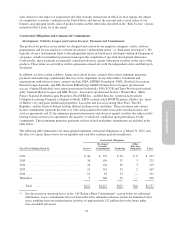

securities could have a significant impact on the fair value of our investments. The following table presents

hypothetical changes in the fair value of our marketable equity securities as of March 31, 2011, arising from

changes in market prices of plus or minus 25 percent, 50 percent, and 75 percent.

Valuation of Securities

Given an X Percentage

Decrease in Each

Stock’s Market Price

Fair Value

as of

March 31,

2011

Valuation of Securities

Given an X Percentage

Increase in Each

Stock’s Market Price

(In millions) (75%) (50%) (25%) 25% 50% 75%

Marketable equity securities ...................... $40 $81 $121 $161 $201 $242 $282

The following table presents hypothetical changes in the fair value of our marketable equity securities as of

March 31, 2010, arising from changes in market prices of plus or minus 25 percent, 50 percent, and 75 percent.

Valuation of Securities

Given an X Percentage

Decrease in Each

Stock’s Market Price

Fair Value

as of

March 31,

2010

Valuation of Securities

Given an X Percentage

Increase in Each

Stock’s Market Price

(In millions) (75%) (50%) (25%) 25% 50% 75%

Marketable equity securities ...................... $73 $146 $218 $291 $364 $437 $509

57