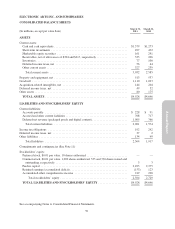

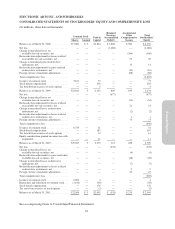

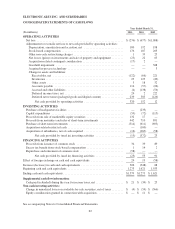

Electronic Arts 2011 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2011 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

Similarly, significant judgment is required to estimate our allowance for doubtful accounts in any accounting

period. We analyze customer concentrations, customer credit-worthiness, current economic trends, and historical

experience when evaluating the adequacy of the allowance for doubtful accounts.

Royalties and Licenses

Royalty-based obligations with content licensors and distribution affiliates are either paid in advance and

capitalized as prepaid royalties or are accrued as incurred and subsequently paid. These royalty-based obligations

are generally expensed to cost of goods sold generally at the greater of the contractual rate for contracts with

guaranteed minimums, or an effective royalty rate based on the total projected net revenue. Significant judgment

is required to estimate the effective royalty rate for a particular contract. Because the computation of effective

royalty rates requires us to project future revenue, it is inherently subjective as our future revenue projections

must anticipate a number of factors, including (1) the total number of titles subject to the contract, (2) the timing

of the release of these titles, (3) the number of software units we expect to sell, which can be impacted by a

number of variables, including product quality, the timing of the title’s release and competition, and (4) future

pricing. Determining the effective royalty rate for our titles is particularly challenging due to the inherent

difficulty in predicting the popularity of entertainment products. Accordingly, if our future revenue projections

change, our effective royalty rates would change, which could impact the amount and timing of royalty expense

we recognize.

Each quarter, we evaluate the expected future realization of our royalty-based assets, as well as any unrecognized

minimum commitments not yet paid to determine amounts we deem unlikely to be realized through product

sales. Any impairments or losses determined before the launch of a product are charged to research and

development expense. Impairments or losses determined post-launch are charged to cost of goods sold. We

evaluate long-lived royalty-based assets for impairment generally using undiscounted cash flows when

impairment indicators exist. Unrecognized minimum royalty-based commitments are accounted for as executory

contracts and, therefore, any losses on these commitments are recognized when the underlying intellectual

property is abandoned (i.e., cease use) or the contractual rights to use the intellectual property are terminated.

Advertising Costs

We generally expense advertising costs as incurred, except for production costs associated with media

campaigns, which are recognized as prepaid assets (to the extent paid in advance) and expensed at the first run of

the advertisement. Cooperative advertising costs are recognized when incurred and are included in marketing and

sales expense if there is a separate identifiable benefit for which we can reasonably estimate the fair value of the

benefit identified. Otherwise, they are recognized as a reduction of revenue and are generally accrued when

revenue is recognized. We then reimburse the channel partner when qualifying claims are submitted.

We are also reimbursed from our vendors for advertising costs, and such amounts are recognized as a reduction

of marketing and sales expense if the advertising (1) is specific to the vendor, (2) represents an identifiable

benefit to us, and (3) represents an incremental cost to us. Otherwise, vendor reimbursements are recognized as a

reduction of cost of goods sold as the related revenue is recognized. Vendor reimbursements of advertising costs

of $31 million, $39 million, and $31 million reduced marketing and sales expense for the fiscal years ended

March 31, 2011, 2010 and 2009, respectively. For the fiscal years ended March 31, 2011, 2010 and 2009,

advertising expense, net of vendor reimbursements, totaled approximately $312 million, $326 million, and $270

million, respectively.

Software Development Costs

Research and development costs, which consist primarily of software development costs, are expensed as

incurred. We are required to capitalize software development costs incurred for computer software to be sold,

leased or otherwise marketed after technological feasibility of the software is established or for development

costs that have alternative future uses. Under our current practice of developing new products, the technological

feasibility of the underlying software is not established until substantially all product development and testing is

complete, which generally includes the development of a working model. The software development costs that

have been capitalized to date have been insignificant.

68