GE 2014 Annual Report Download - page 236

Download and view the complete annual report

Please find page 236 of the 2014 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

216 GE 2014 FORM 10-K

FINANCIAL STATEMENTS FINANCING RECEIVABLES – SUPPLEMENTAL INFORMATION

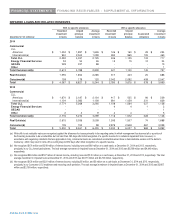

Impaired loans classified as TDRs in our CLL business were $1,869 million and $2,961 million at December 31, 2014 and

2013, respectively, and were primarily attributable to CLL Americas ($1,031 million and $1,770 million, respectively). At

December 31, 2014, we modified $926 million of loans classified as TDRs, primarily in CLL Americas ($515 million). Changes

to these loans primarily included extensions, interest only payment periods, debt to equity exchange and forbearance or other

actions, which are in addition to, or sometimes in lieu of, fees and rate increases. Of our $926 million and $1,509 million of

modifications classified as TDRs at December 31, 2014 and 2013, respectively, $36 million and $71 million have subsequently

experienced a payment default at December 31, 2014 and 2013, respectively.

Real Estate TDRs decreased from $3,625 million at December 31, 2013 to $1,757 million at December 31, 2014, primarily

driven by resolution of TDRs through paydowns. For borrowers with demonstrated operating capabilities, we work to

restructure loans when the cash flow and projected value of the underlying collateral support repayment over the modified

term. We deem loan modifications to be TDRs when we have granted a concession to a borrower experiencing financial

difficulty and we do not receive adequate compensation in the form of an effective interest rate that is at current market rates

of interest given the risk characteristics of the loan or other consideration that compensates us for the value of the concession.

The limited liquidity and higher return requirements in the real estate market for loans with higher loan-to-value (LTV) ratios

has typically resulted in the conclusion that the modified terms are not at current market rates of interest, even if the modified

loans are expected to be fully recoverable. For the year ended December 31, 2014, we modified $672 million of loans

classified as TDRs. Changes to these loans primarily included forbearance, maturity extensions and changes to collateral or

covenant terms or other actions, which are in addition to, or sometimes in lieu of, fees and rate increases. We received the

same or additional compensation in the form of rate increases and fees for the majority of these TDRs. Of our $672 million and

$1,595 million of modifications classified as TDRs during 2014 and 2013, respectively, $252 million and $197 million have

subsequently experienced a payment default in 2014 and 2013, respectively.

The substantial majority of the Real Estate TDRs have reserves determined based upon collateral value. Our specific reserves

on Real Estate TDRs were $25 million and $70 million and were 1.4% and 1.9%, of Real Estate TDRs, respectively, at

December 31, 2014 and 2013. In many situations these loans did not require a specific reserve as collateral value adequately

covered our recorded investment in the loan. While these modified loans had adequate collateral coverage, we were still

required to complete our TDR classification evaluation on each of the modifications without regard to collateral adequacy.

Impaired loans in our Consumer business represent restructured smaller balance homogeneous loans meeting the definition

of a TDR, and are therefore subject to the disclosure requirement for impaired loans, and commercial loans in our Consumer–

Other portfolio. The recorded investment of these impaired loans totaled $2,180 million (with an unpaid principal balance of

$2,271 million) and comprised $138 million with no specific allowance, primarily all in our Consumer–Other portfolio, and

$2,042 million with a specific allowance of $408 million at December 31, 2014. The impaired loans with a specific allowance

included $70 million with a specific allowance of $7 million in our Consumer–Other portfolio and $1,972 million with a specific

allowance of $401 million across the remaining Consumer business and had an unpaid principal balance and average

investment of $2,092 million and $2,547 million, respectively, at December 31, 2014.