GE 2014 Annual Report Download - page 237

Download and view the complete annual report

Please find page 237 of the 2014 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

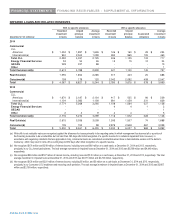

GE 2014 FORM 10-K 217

FINANCIAL STATEMENTS FINANCING RECEIVABLES – SUPPLEMENTAL INFORMATION

Impaired loans classified as TDRs in our Consumer business were $2,132 million and $2,874 million at December 31, 2014

and 2013, respectively. We utilize certain loan modification programs for borrowers experiencing financial difficulties in our

Consumer loan portfolio. These loan modification programs primarily include interest rate reductions and payment deferrals in

excess of three months, which were not part of the terms of the original contract, and are primarily concentrated in our non-

U.S. residential mortgage and U.S. credit card portfolios. For the year ended December 31, 2014, we modified $981 million of

consumer loans for borrowers experiencing financial difficulties, which are classified as TDRs, and included $506 million of

non-U.S. consumer loans, primarily residential mortgages, credit cards and personal loans and $475 million of U.S. consumer

loans, primarily credit cards. We expect borrowers whose loans have been modified under these programs to continue to be

able to meet their contractual obligations upon the conclusion of the modification. Of our $981 million and $1,441 million of

modifications classified as TDRs during 2014 and 2013, respectively, $102 million and $266 million have subsequently

experienced a payment default in 2014 and 2013, respectively.

We also utilize certain short-term (three months or less) loan modification programs for borrowers experiencing temporary

financial difficulties in our Consumer loan portfolio, which are not classified as TDRs. These loan modification programs are

primarily concentrated in our non-U.S. residential mortgage and non-U.S. installment and revolving portfolios. We sold our

U.S. residential mortgage business in 2007 and, as such, do not participate in the U.S. government-sponsored mortgage

modification programs. For the year ended December 31, 2014, we provided short-term modifications of $45 million of

consumer loans for borrowers experiencing financial difficulties, substantially all in our non-U.S. residential mortgage, credit

card and personal loan portfolios. For these modified loans, we provided insignificant interest rate reductions and payment

deferrals, which were not part of the terms of the original contract. We expect borrowers whose loans have been modified

under these short-term programs to continue to be able to meet their contractual obligations upon the conclusion of the short-

term modification.

SUPPLEMENTAL CREDIT QUALITY INFORMATION

COMMERCIAL

Substantially all of our Commercial financing receivables portfolio is secured lending and we assess the overall quality of the

portfolio based on the potential risk of loss measure. The metric incorporates both the borrower’s credit quality along with any

related collateral protection.

Our internal risk ratings process is an important source of information in determining our allowance for losses and represents a

comprehensive approach to evaluate risk in our financing receivables portfolios. In deriving our internal risk ratings, we stratify

our Commercial portfolios into 21 categories of default risk and/or six categories of loss given default to group into three

categories: A, B and C. Our process starts by developing an internal risk rating for our borrowers, which is based upon our

proprietary models using data derived from borrower financial statements, agency ratings, payment history information, equity

prices and other commercial borrower characteristics. We then evaluate the potential risk of loss for the specific lending

transaction in the event of borrower default, which takes into account such factors as applicable collateral value, historical loss

and recovery rates for similar transactions, and our collection capabilities. Our internal risk ratings process and the models we

use are subject to regular monitoring and internal controls. The frequency of rating updates is set by our credit risk policy,

which requires annual Risk Committee approval.

As described above, financing receivables are assigned one of 21 risk ratings based on our process and then these are

grouped by similar characteristics into three categories in the table below. Category A is characterized by either high-credit-

quality borrowers or transactions with significant collateral coverage that substantially reduces or eliminates the risk of loss in

the event of borrower default. Category B is characterized by borrowers with weaker credit quality than those in Category A, or

transactions with moderately strong collateral coverage that minimizes but may not fully mitigate the risk of loss in the event of

default. Category C is characterized by borrowers with higher levels of default risk relative to our overall portfolio or

transactions where collateral coverage may not fully mitigate a loss in the event of default.