McDonalds 2007 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2007 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

(9) Includes pretax operating charges of $853 million ($700 million after tax or $0.55 per share) primarily related to restructuring certain international markets and eliminating

positions, restaurant closings/asset impairment and the write-off of technology costs.

(10) Includes pretax operating charges of $378 million primarily related to the U.S. business reorganization and other global change initiatives, and restaurant closings/asset

impairment as well as net pretax nonoperating income of $125 million primarily related to a gain on the initial public offering of McDonald’s Japan, for a total pretax

expense of $253 million ($143 million after tax or $0.11 per share).

(11) Includes pretax operating charges of $322 million ($219 million after tax or $0.16 per share) consisting of $162 million of “Made For You” costs and $160 million related to a

home offi ce productivity initiative.

(12) Includes a $37 million after tax charge ($0.03 per share) to refl ect the cumulative effect of the adoption of Statement of Financial Accounting Standards (SFAS) No.143,

“Accounting for Asset Retirement Obligations,” which requires legal obligations associated with the retirement of long-lived assets to be recognized at their fair value at

the time the obligations are incurred.

(13) Includes a $99 million after tax charge ($0.07 per share) to refl ect the cumulative effect of the adoption of SFAS No.142, “Goodwill and Other Intangible Assets” (SFAS

No.142), which eliminates the amortization of goodwill and instead subjects it to annual impairment tests. Adjusted for the nonamortization provisions of SFAS No.142,

net income per common share would have been $0.02 higher in 2001 and 2000 and $0.01 higher in 1999 –1997.

(14) While franchised and affi liated sales are not recorded as revenues by the Company, management believes they are important in understanding the Company’s fi nancial

performance because these sales are the basis on which the Company calculates and records franchised and affi liated revenues and are indicative of the fi nancial health

of the franchisee base.

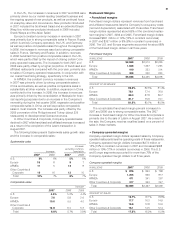

100

150

200

250

300

350

400

$450

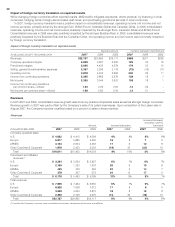

Dec ’02 ’03 ’04 ’05 ’06 ’07

McDonald’s

S&P 500 Index

DJIA companies

100

100

100

157

129

128

206

143

135

221

150

138

298

173

164

406

183

178

Source: Standard & Poor’s Compustat

Stock performance graph

At least annually, we consider which companies comprise a readily identifi able investment peer group. McDonald’s is included

in published restaurant indices; however, unlike most other companies included in these indices, which have no or limited inter-

national operations, McDonald’s does business in more than 100 countries and a substantial portion of our revenues and income is

generated outside the U.S. In addition, because of our size, McDonald’s inclusion in those indices tends to skew the results.

Therefore, we believe that such a comparison is not meaningful.

Our market capitalization, trading volume and importance in an industry that is vital to the U.S. economy have resulted in McDonald’s

inclusion in the Dow Jones Industrial Average (DJIA) since 1985. Like McDonald’s, many DJIA companies generate meaningful

revenues and income outside the U.S. and some manage global brands. Thus, we believe that the use of the DJIA companies as

the group for comparison purposes is appropriate.

The following performance graph shows McDonald’s cumulative total shareholder returns (i.e., price appreciation and reinvest-

ment of dividends) relative to the Standard & Poor’s 500 Stock Index (S&P 500 Index) and to the DJIA companies for the fi ve-year

period ended December 31, 2007. The graph assumes that the value of an investment in McDonald’s common stock, the S&P

500 Index and the DJIA companies (including McDonald’s) was $100 at December 31, 2002. For the DJIA companies, returns are

weighted for market capitalization as of the beginning of each period indicated. These returns may vary from those of the Dow Jones

Industrial Average Index, which is not weighted by market capitalization, and may be composed of different companies during the

period under consideration.

Comparison of fi ve-year cumulative total shareholder returns

23