McDonalds 2007 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2007 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

The Company reviews its fi nancial reporting and disclosure

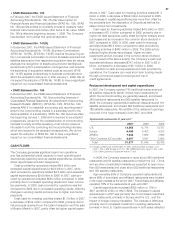

practices and accounting policies quarterly to ensure that they

provide accurate and transparent information relative to the

current economic and business environment. The Company

believes that of its signifi cant accounting policies, the following

involve a higher degree of judgment and/or complexity:

• Property and equipment

Property and equipment are depreciated or amortized on a

straight-line basis over their useful lives based on manage-

ment’s estimates of the period over which the assets will generate

revenue (not to exceed lease term plus options for leased

property). The useful lives are estimated based on historical

experience with similar assets, taking into account anticipated

technological or other changes. The Company periodically

reviews these lives relative to physical factors, economic factors

and industry trends. If there are changes in the planned use

of property and equipment, or if technological changes occur

more rapidly than anticipated, the useful lives assigned to these

assets may need to be shortened, resulting in the recognition of

increased depreciation and amortization expense or write-offs

in future periods.

• Share-based compensation

The Company has a share-based compensation plan which

authorizes the granting of various equity-based incentives

including stock options and restricted stock units (RSUs) to

employees and nonemployee directors. The expense for these

equity-based incentives is based on their fair value at date of

grant and generally amortized over their vesting period.

The fair value of each stock option granted is estimated on

the date of grant using a closed-form pricing model. The pricing

model requires assumptions, such as the expected life of the

stock option and expected volatility of the Company’s stock

over the expected life, which signifi cantly impact the assumed

fair value. The Company uses historical data to determine these

assumptions and if these assumptions change signifi cantly for

future grants, share-based compensation expense will fl uctuate

in future years. The fair value of each RSU granted is equal

to the market price of the Company’s stock at date of grant less

the present value of expected dividends over the vesting period.

• Long-lived assets impairment review

Long-lived assets (including goodwill) are reviewed for impairment

annually in the fourth quarter and whenever events or changes

in circumstances indicate that the carrying amount of an asset

may not be recoverable. In assessing the recoverability of the

Company’s long-lived assets, the Company considers changes

in economic conditions and makes assumptions regarding

estimated future cash fl ows and other factors. Estimates of

future cash fl ows are highly subjective judgments based on the

Company’s experience and knowledge of its operations. These

estimates can be signifi cantly impacted by many factors

including changes in global and local business and economic

conditions, operating costs, infl ation, competition, and con-

sumer and demographic trends. A key assumption impacting

estimated future cash fl ows is the estimated change in

comparable sales. If the Company’s estimates or underlying

assumptions change in the future, the Company may be

required to record impairment charges.

When the Company sells an existing business to a develop-

mental licensee, it determines when these businesses are “held

for sale” in accordance with the requirements of SFAS No. 144,

Accounting for the Impairment or Disposal of Long-lived Assets.

Impairment charges on assets held for sale are recognized when

management and, if required, the Company’s Board of Directors

have approved and committed to a plan to dispose of the as-

sets, the assets are available for disposal, the disposal is prob-

able of occurring within 12 months, and the net sales proceeds

are expected to be less than the assets’ net book value, among

other factors. An impairment charge is recognized for the dif-

ference between the net book value of the business (including

foreign currency translation adjustments recorded in accumulated

other comprehensive income in shareholders’ equity) and the

estimated cash sales price, less costs of disposal.

An alternative accounting policy would be to recharacterize

some or all of any loss as an intangible asset and amortize

it to expense over future periods based on the term of the

relevant licensing arrangement and as revenue is recognized

for royalties and initial fees. Under this alternative for the Latam

transaction, approximately $900 million of the $1.7 billion

impairment charge could have been recharacterized as an

intangible asset and amortized over the franchise term of

20 years, resulting in about $45 million of expense annually.

This policy would be based on a view that the consideration for

the sale consists of two components–the cash sales price and

the future royalties and initial fees.

The Company bases its accounting policy on management’s

determination that royalties payable under its developmental

license arrangements are substantially consistent with market

rates for similar license arrangements. The Company does not

believe it would be appropriate to recognize an asset for the

right to receive market-based fees in future periods, particularly

given the continuing support and services provided to the

licensees. Therefore, the Company believes that the recognition

of an impairment charge based on the net cash sales price

refl ects the substance of the sale transaction.

• Litigation accruals

From time to time, the Company is subject to proceedings,

lawsuits and other claims related to competitors, customers,

employees, franchisees, government agencies, intellectual

property, shareholders and suppliers. The Company is required

to assess the likelihood of any adverse judgments or outcomes

to these matters as well as potential ranges of probable losses.

A determination of the amount of accrual required, if any, for

these contingencies is made after careful analysis of each matter.

The required accrual may change in the future due to new

developments in each matter or changes in approach such as

a change in settlement strategy in dealing with these matters.

The Company does not believe that any such matter currently

being reviewed will have a material adverse effect on its fi nancial

condition or results of operations.

41