McDonalds 2007 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2007 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

The Company uses foreign currency debt and derivatives to

hedge the foreign currency risk associated with certain royalties,

intercompany fi nancings and long-term investments in foreign

subsidiaries and affi liates. This reduces the impact of fl uctuating

foreign currencies on cash fl ows and shareholders’ equity. Total

foreign currency-denominated debt, including the effects of foreign

currency exchange agreements, was $6.1 billion and $6.8 billion at

December 31, 2007 and 2006, respectively. In addition, where

practical, the Company’s restaurants purchase goods and

services in local currencies resulting in natural hedges.

The Company does not have signifi cant exposure to any

individual counterparty and has master agreements that contain

netting arrangements. Certain of these agreements also require

each party to post collateral if credit ratings fall below, or aggregate

exposures exceed, certain contractual limits. At December 31,

2007 and 2006, the Company was required to post collateral of

$55 million and $49 million, respectively, which was used to

reduce the carrying value of the derivatives recorded in other

long-term liabilities.

The Company’s net asset exposure is diversifi ed among a

broad basket of currencies. The Company’s largest net asset

exposures (defi ned as foreign currency assets less foreign

currency liabilities) at year end were as follows:

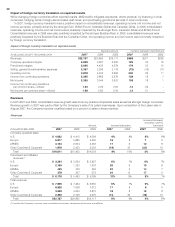

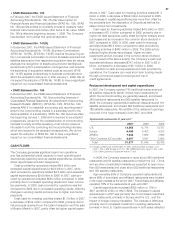

Foreign currency net asset exposures

IN MILLIONS OF U.S. DOLLARS

2007 2006

Euro $3,999 $2,758

Australian Dollars 1,147 837

Canadian Dollars 929 1,099

British Pounds Sterling 634 770

Russian Ruble 463 359

The Company prepared sensitivity analyses of its fi nancial

instruments to determine the impact of hypothetical changes

in interest rates and foreign currency exchange rates on the

Company’s results of operations, cash fl ows and the fair value

of its fi nancial instruments. The interest rate analysis assumed

a one percentage point adverse change in interest rates on

all fi nancial instruments but did not consider the effects of the

reduced level of economic activity that could exist in such an

environment. The foreign currency rate analysis assumed that

each foreign currency rate would change by 10% in the same

direction relative to the U.S. Dollar on all fi nancial instruments;

however, the analysis did not include the potential impact on

sales levels, local currency prices or the effect of fl uctuating cur-

rencies on the Company’s anticipated foreign currency royalties

and other payments received in the U.S. Based on the results of

these analyses of the Company’s fi nancial instruments, neither

a one percentage point adverse change in interest rates from

2007 levels nor a 10% adverse change in foreign currency rates

from 2007 levels would materially affect the Company’s results of

operations, cash fl ows or the fair value of its fi nancial instruments.

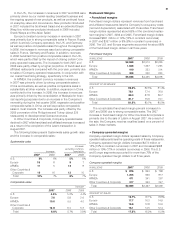

Contractual obligations and commitments

The Company has long-term contractual obligations primarily

in the form of lease obligations (related to both Company-

operated and franchised restaurants) and debt obligations. In

addition, the Company has long-term revenue and cash fl ow

streams that relate to its franchise arrangements. Cash provided

by operations (including cash provided by these franchise

arrangements) along with the Company’s borrowing capacity

and other sources of cash will be used to satisfy the obligations.

The following table summarizes the Company’s contractual

obligations and their aggregate maturities as well as future

minimum rent payments due to the Company under existing

franchise arrangements as of December 31, 2007. (See discus-

sions of cash fl ows and fi nancial position and capital resources

as well as the Notes to the consolidated fi nancial statements for

further details.)

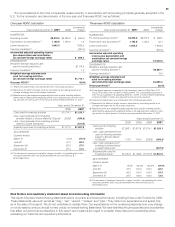

Contractual cash outfl ows Contractual cash infl ows

Operating Debt Minimum rent under

IN MILLIONS leases obligations

(1)

franchise arrangements

2008 $ 1,054 $1,991 $ 2,054

2009 974 449 1,990

2010 898 540 1,920

2011 822 552 1,834

2012 757 2,217 1,768

Thereafter 6,009 3,467 12,532

Total $10,514 $9,216 $22,098

(1) The maturities refl ect reclassifi cations of short-term obligations to long-term obliga-

tions of $1.3 billion, as they are supported by a long-term line of credit agreement

expiring in 2012. Debt obligations do not include $85 million of SFAS No. 133

noncash fair value adjustments because these adjustments have no impact on the

obligation at maturity, as well as $148 million of accrued interest.

The Company maintains certain supplemental benefi t plans

that allow participants to (i) make tax-deferred contributions and

(ii) receive Company-provided allocations that cannot be made

under the qualifi ed benefi t plans because of IRS limitations. The

investment alternatives and returns are based on certain market-rate

investment alternatives under the Company’s qualifi ed Profi t

Sharing and Savings Plan. Total liabilities for the supplemental

plans were $415 million at December 31, 2007 and $379 million

at December 31, 2006 and were included in other long-term

liabilities in the Consolidated balance sheet. Also included in

other long-term liabilities at December 31, 2007 were gross

unrecognized tax benefi ts of $250 million and liabilities for

international retirement plans of $129 million.

In connection with the Latam transaction, the Company

has agreed to indemnify the buyers for certain tax and other

claims, certain of which are refl ected as liabilities in McDonald’s

Consolidated balance sheet totaling $179 million at year-end 2007.

OTHER MATTERS

Critical accounting policies and estimates

Management’s discussion and analysis of fi nancial condition

and results of operations is based upon the Company’s

consolidated fi nancial statements, which have been prepared

in accordance with accounting principles generally accepted in

the U.S. The preparation of these fi nancial statements requires

the Company to make estimates and judgments that affect the

reported amounts of assets, liabilities, revenues and expenses

as well as related disclosures. On an ongoing basis, the Com-

pany evaluates its estimates and judgments based on historical

experience and various other factors that are believed to be

reasonable under the circumstances. Actual results may differ

from these estimates under various assumptions or conditions.

40