McDonalds 2007 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2007 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

Impairment and other charges (credits), net reduced/

(increased) return on average assets by 5.4 percentage points,

0.4 percentage points and (0.2) percentage points in 2007,

2006 and 2005, respectively. In addition, these items along with

the 2007 and 2005 net tax benefi t resulting from the completion

of IRS examinations and incremental tax expense in connection

with HIA, reduced/(increased) return on average common equity

by 8.5 percentage points, 0.6 percentage points and (0.5)

percentage points in 2007, 2006 and 2005, respectively.

In 2007 and 2006, return on average assets and return on

average common equity both benefi ted from strong operating

results in the U.S. and Europe, as well as improved results in

APMEA. During 2008, the Company will continue to concentrate

restaurant openings and new capital invested in markets with

acceptable returns or opportunities for long-term growth.

Financing and market risk

The Company generally borrows on a long-term basis and is

exposed to the impact of interest rate changes and foreign

currency fl uctuations. Debt obligations at December 31, 2007

totaled $9.3 billion, compared with $8.4 billion at December 31,

2006. The net increase in 2007 was primarily due to net issuances

of $573 million and the impact of changes in exchange rates on

foreign currency denominated debt of $342 million, partly offset

by Statement of Financial Accounting Standards No. 133,

Accounting for Derivative Instruments and Hedging Activities

(SFAS No. 133) noncash fair value adjustments of $23 million.

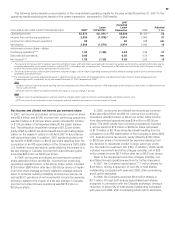

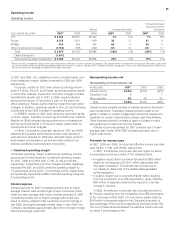

Debt highlights

(1

)

2007 2006 2005

Fixed-rate debt as a percent

of total debt

(2,3)

58% 49% 46%

Weighted-average annual

interest rate of total debt 4.7 4.1 4.1

Foreign currency-denominated

debt as a percent of total debt

(2,3)

66 80 80

Total debt as a percent of total

capitalization (total debt and

total shareholders‘ equity)

(2)

38 35 40

Cash provided by operations

as a percent of total debt

(2)

53 52 44

(1) All percentages are as of December 31st, except for the weighted-average annual

interest rate, which is for the year.

(2) Based on debt obligations before the effect of SFAS No. 133 fair value adjust-

ments. This effect is excluded, as these adjustments have no impact on the

obligation at maturity. See Debt fi nancing note to the consolidated fi nancial

statements.

(3) Includes the effect of interest rate and foreign currency exchange agreements.

Fitch, Standard & Poor’s and Moody’s currently rate the

Company’s commercial paper F1, A-1 and P-2, respectively;

and its long-term debt A, A and A3, respectively. Historically,

the Company has not experienced diffi culty in obtaining fi nanc-

ing or refi nancing existing debt. The Company’s key metrics for

monitoring its credit structure are shown in the preceding table.

While the Company targets these metrics for ease of focus, it

also considers similar credit ratios that incorporate capitalized

operating leases to estimate total adjusted debt. Total adjusted

debt, a term that is commonly used by the rating agencies

referred to above, includes debt outstanding on the Company’s

balance sheet plus an adjustment to capitalize operating

leases. Based on their most recent calculations, these agencies

add between $7 billion and $11 billion to debt for lease capitaliza-

tion purposes, which increases total debt as a percent of total

capitalization and reduces cash provided by operations as a

percent of total debt for credit rating purposes. The Company

believes the rating agency methodology for capitalizing leases

requires certain adjustments. These adjustments include:

excluding percent rents in excess of minimum rents; exclud-

ing certain Company-operated restaurant lease agreements

outside the U.S. that are cancelable with minimal penalties

(representing approximately 25% of Company-operated restau-

rant minimum rents outside the U.S., based on the Company’s

estimate); capitalizing non-restaurant leases using a multiple of

three times rent expense; and reducing total rent expense by

a percentage of the annual minimum rent payments due to the

Company from franchisees operating on leased sites. Based on

this calculation, for credit analysis purposes, approximately $4

billion of future operating lease payments would be capitalized.

Certain of the Company’s debt obligations contain cross-

acceleration provisions and restrictions on Company and sub-

sidiary mortgages and the long-term debt of certain subsidiaries.

There are no provisions in the Company’s debt obligations that

would accelerate repayment of debt as a result of a change

in credit ratings or a material adverse change in the Company’s

business. The Company has approximately $7.3 billion of

authority to issue debt securities, including debt securities

registered on a U.S. shelf registration statement and in con-

nection with a Euro Medium-Term Notes program. The Com-

pany also has $1.3 billion available under a committed line of

credit agreement (see Debt fi nancing note to the consolidated

fi nancial statements) and authority to issue commercial paper.

In 2008, the Company expects to issue commercial paper and

long-term debt in order to refi nance maturing debt and fi nance

a portion of the Company’s previously disclosed expectation to

return $15 billion to $17 billion to shareholders. Debt maturing in

2008 includes approximately $1.8 billion of outstanding

borrowings under the HIA multi-currency term loan facility

and $800 million of long-term corporate debt.

The Company uses major capital markets, bank fi nancings

and derivatives to meet its fi nancing requirements and reduce

interest expense. The Company manages its debt portfolio

in response to changes in interest rates and foreign currency

rates by periodically retiring, redeeming and repurchasing debt,

terminating exchange agreements and using derivatives. The

Company does not use derivatives with a level of complexity or

with a risk higher than the exposures to be hedged and does

not hold or issue derivatives for trading purposes. All exchange

agreements are over-the-counter instruments.

In managing the impact of interest rate changes and foreign

currency fl uctuations, the Company uses interest rate exchange

agreements and fi nances in the currencies in which assets are

denominated. Derivatives were recorded at fair value in the

Company’s Consolidated balance sheet at December 31, 2007

and 2006 in miscellaneous other assets of $64 million and

$41 million, respectively, and other long-term liabilities of $70

million and $117 million, respectively. See Summary of signifi -

cant accounting policies note to the consolidated fi nancial state-

ments related to fi nancial instruments for additional information

regarding their use and the impact of SFAS No. 133 regarding

derivatives.

39