McDonalds 2007 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2007 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

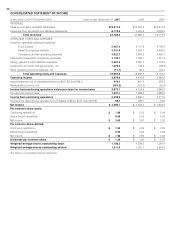

Consolidated net deferred tax liabilities included tax assets,

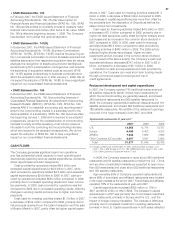

net of valuation allowance, of $1.4 billion in 2007 and $1.2 billion

in 2006. Substantially all of the net tax assets arose in the U.S.

and other profi table markets.

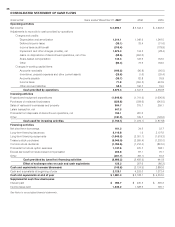

Discontinued operations

The Company continues to focus its management and fi nancial

resources on the McDonald’s restaurant business as it believes

the opportunities for long-term growth remain signifi cant.

Accordingly, during the third quarter 2007, the Company sold

its investment in Boston Market. In 2006, the Company dis-

posed of its investment in Chipotle via public stock offerings

in the fi rst and second quarters and a tax-free exchange for

McDonald’s common stock in the fourth quarter. As a result

of the disposals during 2007 and 2006, both Boston Market’s

and Chipotle’s results of operations and transaction gains are

refl ected as discontinued operations for all periods presented.

In connection with the Company’s sale of its investment in

Boston Market in August 2007, the Company received proceeds

of approximately $250 million and recorded a gain of $69 million

after tax. In addition, Boston Market’s net income (loss) for

2007, 2006 and 2005 was ($9) million, $7 million and $9 million,

respectively.

In fi rst quarter 2006, Chipotle completed an IPO of 6.1 million

shares resulting in a tax-free gain to McDonald’s of $32 million

to refl ect an increase in the carrying value of the Company’s

investment as a result of Chipotle selling shares in the public

offering. Concurrent with the IPO, McDonald’s sold 3.0 million

Chipotle shares, resulting in net proceeds to the Company of

$61 million and an additional gain of $14 million after tax. In

second quarter 2006, McDonald’s sold an additional 4.5 million

Chipotle shares, resulting in net proceeds to the Company of

$267 million and a gain of $128 million after tax, while still

retaining majority ownership. In fourth quarter 2006, the Company

completely separated from Chipotle through a noncash, tax-free

exchange of its remaining Chipotle shares for its common

stock. McDonald’s accepted 18.6 million shares of its common

stock in exchange for the 16.5 million shares of Chipotle class

B common stock held by McDonald’s and recorded a tax-free

gain of $480 million. In addition, Chipotle’s net income for 2006

and 2005 was $18 million and $16 million, respectively.

Accounting changes

• SFAS Statement No. 158

In September 2006, the Financial Accounting Standards Board

(FASB) issued Statement of Financial Accounting Standards

No. 158, Employers’ Accounting for Defi ned Benefi t Pension and

Other Postretirement Plans, an amendment of FASB Statements

No. 87, 88, 106 and 132(R) (SFAS No. 158). SFAS No. 158

requires the Company to recognize the overfunded or

underfunded status of a defi ned benefi t postretirement plan as

an asset or liability in the Consolidated balance sheet and to

recognize changes in that funded status in the year changes

occur through other comprehensive income. The Company

adopted the applicable provisions of SFAS No. 158 effective

December 31, 2006, as required. This resulted in a net

adjustment to other comprehensive income of $89 million,

for a limited number of applicable international markets.

• EITF Issue 06-2

In June 2006, the FASB ratifi ed Emerging Issues Task Force

(EITF) Issue 06-2, Accounting for Sabbatical Leave and Other

Similar Benefi ts Pursuant to FASB Statement No. 43, Accounting

for Compensated Absences (EITF 06-2). Under EITF 06-2,

compensation costs associated with a sabbatical should be

accrued over the requisite service period, assuming certain

conditions are met. Previously, the Company expensed

sabbatical costs as incurred. The Company adopted EITF 06-2

effective January 1, 2007, as required and accordingly, we

recorded a $36 million cumulative adjustment, net of tax, to

decrease the January 1, 2007 balance of retained earnings.

The annual impact to earnings of this accounting change is

not signifi cant.

• FASB Interpretation No. 48

In July 2006, the FASB issued Interpretation No. 48, Accounting

for Uncertainty in Income Taxes (FIN 48), which is an interpretation

of FASB Statement No. 109, Accounting for Income Taxes. FIN

48 clarifi es the accounting for income taxes by prescribing the

minimum recognition threshold a tax position is required to

meet before being recognized in the fi nancial statements. FIN 48

also provides guidance on derecognition, measurement,

classifi cation, interest and penalties, accounting in interim

periods, disclosure and transition. The Company adopted the

provisions of FIN 48 effective January 1, 2007, as required. As

a result of the implementation of FIN 48, the Company recorded

a $20 million cumulative adjustment to increase the January 1,

2007 balance of retained earnings. FIN 48 requires that a

liability associated with an unrecognized tax benefi t be classifi ed

as a long-term liability except for the amount for which cash

payment is anticipated within one year. Upon adoption of

FIN 48, $339 million of tax liabilities, net of deposits, were

reclassifi ed from current to long-term and included in other

long-term liabilities.

• SFAS Statement No. 157

In September 2006, the FASB issued Statement of Financial

Accounting Standards No. 157, Fair Value Measurements

(SFAS No. 157). SFAS No. 157 defi nes fair value, establishes a

framework for measuring fair value in accordance with gener-

ally accepted accounting principles, and expands disclosures

about fair value measurements. This statement does not require

any new fair value measurements; rather, it applies to other

accounting pronouncements that require or permit fair value

measurements. The provisions of SFAS No. 157, as issued, are

effective January 1, 2008. However, in February 2008, the FASB

deferred the effective date of SFAS No. 157 for one year for

certain non-fi nancial assets and non-fi nancial liabilities, except

those that are recognized or disclosed at fair value in the fi nan-

cial statements on a recurring basis (i.e., at least annually).

We adopted the required provisions of SFAS No. 157 related to

debt and derivatives as of January 1, 2008. The annual impact

of this accounting change is not expected to be signifi cant.

36