McDonalds 2007 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2007 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

communicate our everyday value offerings and feature limited-time

variations of classic menu favorites.

We believe locally-owned and operated restaurants are at

the core of our competitive advantage and make us not just a

global brand but a locally relevant one. To that end, we

continually evaluate ownership structures in our markets to

maximize brand performance and further enhance the reliability

of our cash fl ow and returns. We completed a detailed analysis

of the appropriate ownership mix in key markets around the

world taking into account our plans for each of those markets,

the risks associated with operating in the market and restaurant-

level results. This analysis also considered the current legal and

regulatory environment which, in some countries such as China

and Russia, may make it prudent for the Company to own and

operate the restaurants. Based on this analysis, we expect to

refranchise a total of 1,000 to 1,500 existing Company-operated

restaurants, primarily in our major markets, over the next three

or more years. This will be dependent on our ability to identify

the appropriate prospective franchisees with the experience

and fi nancial resources in the relevant markets.

In addition, we will continue to evaluate several small markets

in APMEA and Europe for potential transition to developmental

license structures. We will only convert such markets when we

believe that we have identifi ed a qualifi ed licensee and our

business is ready for transition to optimize the transaction for

the long term.

Our evolution toward a more heavily franchised, less capital-

intensive business model has favorable implications for the

amount of capital we invest, the strength and stability of our

cash fl ow and for our returns. As a result, we expect free cash

fl ow — cash from operations less capital expenditures — will

continue to grow and be a signifi cant source of cash used to

fund our total cash returned to shareholders target for 2007

through 2009 of $15 billion to $17 billion. In addition, we expect

our share repurchase activity will continue to yield reductions in

the share count in the years ahead.

While the Company does not provide specifi c guidance on

net income per share, the following information is provided to

assist in analyzing the Company’s results:

• Changes in Systemwide sales are driven by comparable

sales and net restaurant unit expansion. The Company

expects net restaurant additions to add slightly more than

1 percentage point to 2008 Systemwide sales growth (in

constant currencies), most of which will be due to the

503 net traditional restaurants added in 2007.

• The Company does not generally provide specifi c guidance

on changes in comparable sales. However, as a perspective,

assuming no change in cost structure, a 1 percentage point

increase in U.S. comparable sales would increase annual net

income per share by about 2.5 cents. Similarly, an increase

of 1 percentage point in Europe’s comparable sales would

increase annual net income per share by about 2.5 cents.

• In 2008, U.S. beef costs are expected to be relatively fl at

and chicken costs are expected to rise about 4% to 5%. In

Europe, beef costs are expected to be relatively fl at in 2008,

while chicken costs are expected to increase approximately

6% to 8%. Some volatility may be experienced between

quarters in the normal course of business.

• The Company expects full-year 2008 selling, general &

administrative expenses to decline, in constant currencies,

although fl uctuations may be experienced between the quar-

ters due to items such as the 2008 biennial worldwide owner/

operator convention, the 2008 Beijing Summer Olympics and

the August 2007 sale of the Company’s businesses in Latam.

• Based on current interest and foreign currency exchange

rates, the Company expects interest expense in 2008 to in-

crease approximately 15% to 20% compared with 2007, while

2008 interest income is expected to be about half of 2007

interest income.

• A signifi cant part of the Company’s operating income is

generated outside the U.S., and about 65% of its total debt

is denominated in foreign currencies. Accordingly, earnings

are affected by changes in foreign currency exchange rates,

particularly the Euro and the British Pound. If the Euro and the

British Pound both move 10% in the same direction compared

with 2007, the Company’s annual net income per share

would change by about 8 cents to 9 cents.

• The Company expects the effective income tax rate for the

full-year 2008 to be approximately 30% to 32%, although

some volatility may be experienced between the quarters in

the normal course of business.

• The Company expects capital expenditures for 2008 to be

approximately $2 billion. About half of this amount will be

reinvested in existing restaurants while the rest will primarily

be used to open 1,000 restaurants (950 traditional and 50

satellites). We expect net additions of about 600 (700 net

traditional additions and 100 net satellite closings).

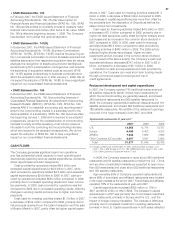

• For 2007 through 2009, the Company expects to return $15

billion to $17 billion to shareholders through share repurchases

and dividends, subject to business and market conditions.

In 2007, the Company returned $5.7 billion of this goal to

shareholders.

• As a result of the new developmental licensee structure, the

Company’s operating results in Latin America will refl ect royalty

income of approximately 5% of sales and minimal selling,

general & administrative expenses to support the business.

• We continually review our restaurant ownership structures

to maximize cash fl ow and returns and to enhance local

relevance. We expect to optimize our restaurant ownership

mix by refranchising 1,000 to 1,500 Company-operated

restaurants over the next three or more years, primarily in our

major markets, and by continuing to execute our developmental

license strategy.

• In February 2008, a European private equity fi rm agreed to

acquire U.K.-based Pret a Manger. As part of that transaction

and consistent with its focus on the McDonald’s restaurant

business, McDonald’s has agreed to sell its minority interest

in Pret a Manger. The Company expects to recognize a non-

operating gain upon the closing of the transaction in late fi rst

quarter or early second quarter of 2008, subject to regulatory

approvals and other closing conditions.

27