McDonalds 2007 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2007 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

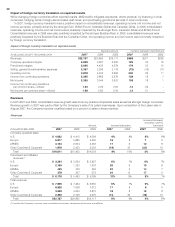

Venezuela and 13 other countries in Latin America and the

Caribbean to a developmental license structure. The Company

refers to these markets as “Latam.”

Based on approval by the Company’s Board of Directors

on April 17, 2007, the Company concluded Latam was “held

for sale” as of that date in accordance with the requirements

of SFAS No. 144, Accounting for the Impairment or Disposal of

Long-lived Assets. As a result, the Company recorded an im-

pairment charge of $1.7 billion in 2007, substantially all of which

was noncash. The charge included $896 million for the differ-

ence between the net book value of the Latam business and

approximately $675 million in cash proceeds received. This loss

in value was primarily due to a historically diffi cult economic

environment coupled with volatility experienced in many of the

markets included in this transaction. The charges also included

historical foreign currency translation losses of $769 million

recorded in shareholders’ equity. The Company recorded a

tax benefi t of $62 million in connection with this transaction.

As a result of meeting the “held for sale” criteria, the Company

ceased recording depreciation expense with respect to Latam

effective April 17, 2007. In connection with the sale, the Company

has agreed to indemnify the buyers for certain tax and other

claims, certain of which are refl ected as liabilities in McDonald’s

Consolidated balance sheet totaling $179 million at year-end

2007.

The buyers of the Company’s operations in Latam have

entered into a 20-year master franchise agreement that requires

the buyers, among other obligations to (i) pay monthly royalties

commencing at a rate of approximately 5% of gross sales of

the restaurants in these markets, substantially consistent with

market rates for similar license arrangements; (ii) commit to

adding approximately 150 new McDonald’s restaurants over the

fi rst three years and pay an initial fee for each new restaurant

opened; and (iii) commit to specifi ed annual capital expenditures

for existing restaurants.

In addition, we transitioned another fi ve small markets in

Europe with a total of 24 restaurants to the developmental

license structure in 2007.

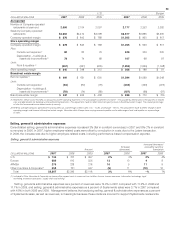

We also made progress franchising certain Company-operated

restaurants in key markets. As a result of our developmental

license strategy and franchising initiatives, the percent of

franchised and affi liated restaurants worldwide increased

from 74% at year-end 2006 to 78% at year-end 2007.

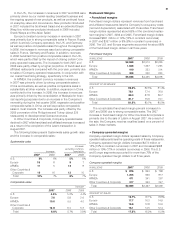

Highlights from the year included:

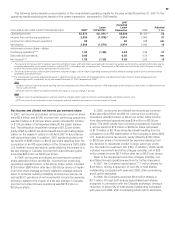

• Comparable sales increased 6.8% building on a 5.7%

increase in 2006.

• Systemwide sales increased 12% (8% in constant currencies).

• Company-operated margins reached an eight-year high

of 17.3%. Franchised margins were 81.5%— a level not

achieved in over ten years.

• Cash provided by operations totaled $4.9 billion and capital

expenditures totaled $1.9 billion.

•

The Company announced that for 2007 through 2009, we

expect to return $15 billion to $17 billion to shareholders

through share repurchases and dividends, subject to business

and market conditions. In 2007, the Company raised its

annual dividend by 50% to $1.50 per share, or $1.8 billion,

and repurchased 77.1 million shares for $3.9 billion, driving

a reduction of over 3% of total shares outstanding at year end

compared with 2006.

• One-year ROIIC was 49.9% and three-year ROIIC was 39.4%

for 2007.

Outlook for 2008

The McDonald’s System is energized by our current worldwide

momentum. We intend to build on this momentum by continuing

to execute our Plan to Win with its strategic focus on our

customers and restaurants while exercising disciplined fi nancial

management. As we do so, we are confi dent we will continue

to meet or exceed the long-term fi nancial targets previously

discussed.

We will continue to drive success in 2008 and beyond by

leveraging key consumer insights and our global experience,

while relying on our strengths in developing, testing and im-

plementing initiatives surrounding our global business drivers

of convenience, branded affordability, daypart expansion and

menu variety.

In the U.S., our key areas of focus will be breakfast, chicken,

beverages and convenience. In 2008, we expect to build on our

breakfast momentum and at the same time extend our leadership

in the chicken category with the launch of the Southern Style

Chicken Biscuit Sandwich for breakfast and the Southern Style

Chicken Sandwich for the remainder of the day. We will also

continue to provide value and convenience to solidify our

connection with consumer lifestyles. In addition, as part of a

comprehensive, multi-year beverage business strategy designed

to take advantage of the signifi cant and growing beverage

category, we will begin introducing hot specialty coffee offerings in

2008, on a market-by-market basis. It will not be until late 2009

when we will begin to recognize the full sales benefi t of

our beverage opportunity. This fi rst component of our beverage

business may require construction, new equipment, new

processes and training in our restaurants; all of which will

serve as a platform for the anticipated future introduction of

smoothies, frappes and other beverage options.

In Europe, we plan to strengthen our local relevance using a

tiered menu approach featuring premium selections, classic menu

favorites and everyday affordable offerings. We will complement

these with new products and limited-time food promotions developed

in our European food studio. Building greater brand transparency

will remain a priority in Europe, especially in the U.K., with ongoing

communication efforts highlighting the quality of our food and

building our reputation as an employer of choice. We will also

create stronger bonds of trust by being accessible and main-

taining an open dialogue with customers and key stakeholders.

As part of our efforts to upgrade the customer experience, we

will continue remodeling additional restaurants in the U.K. and

Germany. In Germany, an integral part of our reimaging program

includes adding about 100 McCafes in 2008. We will also

continue installing our new kitchen operating system to ensure

that we can consistently deliver high food quality, with a goal for

this new system to be in virtually all of our European restaurants

by the end of 2009.

In APMEA, locally-relevant execution of our strategies sur-

rounding convenience, breakfast, core menu extensions and

value is essential to sustaining momentum in this diverse and

dynamic part of the world. Convenience initiatives include

leveraging the success of 24-hours or extended hours of

service, offering delivery service in certain countries and building

our drive-thru business, particularly in China. In addition, we will

continue to emphasize breakfast to further build this daypart,

26