Toyota 2005 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2005 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS >67

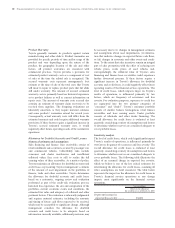

OFF-BALANCE SHEET ARRANGEMENTS

Securitization Funding

Toyota uses its securitization program as part of its

funding for its financial services operations. Toyota

believes that the securitizations are an important element

of its financial services operations as it provides a cost-

effective funding source.

Securitization of receivables allows Toyota to access a

highly liquid and efficient capital market while providing

Toyota with an alternative source of funding and investor

diversification. See note 7 to the consolidated financial

statements with respect to the impact on the balance sheet,

income statement, and cash flows of these securitizations.

Toyota’s securitization program involves a two-step

transaction. Toyota sells discrete pools of retail finance

receivables to a wholly-owned, bankruptcy remote special

purpose entity (“SPE”), which in turn transfers the

receivables to a qualified special purpose entity (“QSPE”

or “securitization trust”) in exchange for the proceeds

from securities issued by the securitization trust. Once the

receivables are transferred to the QSPE, the receivables are

no longer assets of Toyota and, therefore, no longer

appear in Toyota’s consolidated balance sheet. These

securities are secured by collections on the sold receivables

and structured into senior and subordinated classes.

The following flow chart diagrams a typical securitiza-

tion transaction:

Toyota’s use of SPEs in securitizations is consistent with

conventional practices in the securitization markets. The

sale to the SPE isolates the sold receivables from other

creditors of Toyota for the benefit of securitization

investors and, assuming accounting requirements are

satisfied, the sold receivables are accounted for as a sale.

While Toyota retains subordinated interests, investors in

securitizations have no recourse to Toyota, any cash

reserve funds, or any amounts available or funded under

the revolving liquidity notes discussed below. Toyota does

not guarantee any securities issued by the securitization

trust. Each SPE has a limited purpose and may only be

used to purchase and sell the receivables. The individual

securitization trusts have a limited duration and generally

terminate when investors holding the asset-backed

securities have been paid all amounts owed to them.

The SPE retains an interest in the securitization trust.

The retained interest includes subordinated securities

issued by the securitization trust and interest-only strips

representing the right to receive any excess interest. The

retained interests are subordinated and serve as credit

enhancements for the more senior securities issued by the

securitization trust. The retained interests are held by the

SPE as restricted assets and are not available to satisfy any

obligations of Toyota. If forecasted future cash flows result

in an other-than-temporary decline in the fair value of the

retained interests, then an impairment loss is recognized

to the extent that the fair value is less than the carrying

amount. Such losses would be included in the consoli-

dated statement of income. These retained interests as well

as senior securities purchased by Toyota are reflected in

the consolidated balance sheet for accounting purposes.

Various other forms of credit enhancements are

provided to reduce the risk of loss for senior classes of

securities. These credit enhancements may include the

following:

Cash reserve funds or restricted cash

A portion of the proceeds from the sale of asset-backed

securities may be held by the securitization trust in

segregated reserve funds and may be used to pay principal

and interest to investors if collections on the sold

receivables are insufficient. In the event a trust experiences

charge-offs or delinquencies above specified levels,

additional excess amounts from collections on receivables

held by the securitization trusts will be added to such

reserve funds.

Off-balance

sheet

transaction

Toyota SPE

(Wholly-owned

by Toyota)

Investors

QSPE

(Securitization

Trust)

Receivables Receivables Securities

Proceeds

Proceeds Proceeds

Bankruptcy

remote

transaction