Toyota 2005 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2005 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

develops several potential loss scenarios, and reviews

allowance levels to determine whether reserves are consid-

ered adequate to cover the probable range of losses.

The allowance for residual value losses is maintained in

amounts considered by Toyota to be appropriate in

relation to the estimated losses on its owned portfolio.

Upon disposal of the assets, the allowance for residual

losses is adjusted for the difference between the net book

value and the proceeds from sale.

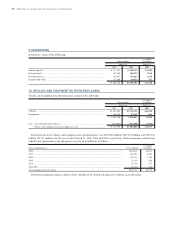

Inventories—

Inventories are valued at cost, not in excess of market, cost

being determined on the “average-cost” basis, except for

the cost of finished products carried by certain subsidiary

companies which is determined on the “specific identifi-

cation” basis or “last-in, first-out” (“LIFO”) basis.

Inventories valued on the LIFO basis totaled ¥190,642

million and ¥233,440 million ($2,174 million) at March

31, 2004 and 2005, respectively. Had the “first-in, first-

out” basis been used for those companies using the LIFO

basis, inventories would have been ¥21,463 million and

¥31,894 million ($297 million) higher than reported at

March 31, 2004 and 2005, respectively.

Property, plant and equipment—

Property, plant and equipment are stated at cost. Major

renewals and improvements are capitalized; minor

replacements, maintenance and repairs are charged to

current operations. Depreciation of property, plant and

equipment is mainly computed on the declining-balance

method for the parent company and Japanese subsidiaries

and on the straight-line method for foreign subsidiary

companies at rates based on estimated useful lives of the

respective assets according to general class, type of

construction and use. The estimated useful lives range

from 3 to 60 years for buildings and from 2 to 20 years for

machinery and equipment.

Vehicles and equipment on operating leases to third

parties are originated by dealers and acquired by certain

consolidated subsidiaries. Such subsidiaries are also the

lessors of certain property that they acquire directly.

Vehicles and equipment on operating leases are depre-

ciated primarily on a straight-line method over the lease

term, generally three years, to the estimated residual value.

Long-lived assets—

Toyota reviews its long-lived assets, including investments

in affiliated companies, for impairment whenever events

or changes in circumstances indicate that the carrying

amount of an asset may not be recoverable. An impairment

loss would be recognized when the carrying amount of an

asset exceeds the estimated undiscounted future cash flows

expected to result from the use of the asset and its eventual

disposition. The amount of the impairment loss to be

recorded is calculated by the excess of the carrying value of

the asset over its fair value. Fair value is determined mainly

using a discounted cash flow valuation method.

Goodwill and intangible assets—

Goodwill is not material to Toyota’s consolidated balance

sheets.

Intangible assets consist mainly of software. Intangible

assets with a definite life are amortized on a straight-line

basis with estimated useful lives mainly of 5 years.

Intangible assets with an indefinite life are tested for

impairment whenever events or circumstances indicate

that a carrying amount of an asset (asset group) may not

be recoverable. An impairment loss would be recognized

when the carrying amount of an asset exceeds the estimated

undiscounted cash flows used in determining the fair

value of the asset. The amount of the impairment loss to

be recorded is generally determined by the difference

between the fair value of the asset using a discounted cash

flow valuation method and the current book value.

Employee benefit obligations—

Toyota has both defined benefit and defined contribution

plans for employees’ retirement benefits. Retirement benefit

obligations are measured by actuarial calculations in accor-

dance with a Statement of Financial Accounting Standard

(“FAS”) No. 87 Employers’ accounting for pensions (“FAS

87”), “Accrued pension and severance costs” are determined

by amounts of obligations, plan assets, unrecognized prior

service costs and unrecognized actuarial gains/losses. A

minimum pension liability is recorded for plans where the

accumulated benefit obligation net of plan assets exceeds

the accrued pension and severance costs.

Environmental matters—

Environmental expenditures relating to current operations

are expensed or capitalized as appropriate. Expenditures

relating to existing conditions caused by past operations,

which do not contribute to current or future revenues, are

expensed. Liabilities for remediation costs are recorded

when they are probable and reasonably estimable,

generally no later than the completion of feasibility studies

or Toyota’s commitment to a plan of action. The cost of

each environmental liability is estimated by using current

technology available and various engineering, financial

and legal specialists within Toyota based on current law.

Such liabilities do not reflect any offset for possible recov-

eries from insurance companies and are not discounted.

There were no material changes in these liabilities for all

periods presented.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS >83