Toyota 2005 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2005 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

74 >MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

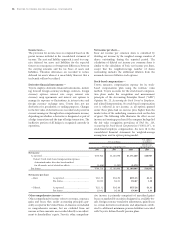

Sensitivity analysis

The following table illustrates the effect of assumed

changes in discount rates and the expected rate of return

on plan assets, which we believe are critical estimates in

determining pension costs and obligations, assuming all

other assumptions are consistent.

Yen in millions

Effect on pre-tax income Effect on PBO

for the year ending as of March 31,

March 31, 2006 2005

Discount rates

0.5% decrease .............. ¥(10,496) ¥ 128,713

0.5% increase............... 8,814 (110,883)

Expected rate of return

on plan assets

0.5% decrease .............. ¥ (4,673)

0.5% increase............... 4,673

Derivatives and Other Contracts at Fair Value

Toyota uses derivatives in the normal course of business

to manage its exposure to foreign currency exchange rates

and interest rates. The accounting is complex and con-

tinues to evolve. In addition, there are the significant

judgments and estimates involved in the estimating of fair

value in the absence of quoted market values. These

estimates are based upon valuation methodologies deemed

appropriate in the circumstances; however, the use of

different assumptions may have a material effect on the

estimated fair value amounts.

Marketable securities

Toyota’s accounting policy is to record a write-down of

such investments to realizable value when a decline in fair

value below the carrying value is other-than-temporary. In

determining if a decline in value is other-than-temporary,

Toyota considers the length of time and the extent to

which the fair value has been less than the carrying value,

the financial condition and prospects of the company and

Toyota’s ability and intent to retain its investment in the

company for a period of time sufficient to allow for any

anticipated recovery in market value.

MARKET RISK DISCLOSURE

Toyota is exposed to market risk from changes in foreign

currency exchange rates, interest rates and certain com-

modity and equity security prices. In order to manage the

risk arising from changes in foreign currency exchange

rates and interest rates, Toyota enters into a variety of

derivative financial instruments.

A description of Toyota’s accounting policies for deriva-

tive instruments is included in note 2 to the consolidated

financial statements and further disclosure is provided in

notes 20 and 21 to the consolidated financial statements.

Toyota monitors and manages these financial exposures

as an integral part of its overall risk management program,

which recognizes the unpredictability of financial markets

and seeks to reduce the potentially adverse effects on

Toyota’s operating results.

The financial instruments included in the market risk

analysis consist of all of Toyota’s cash and cash equi-

valents, marketable securities, finance receivables, securities

investments, long-term and short-term debt and all deriva-

tive financial instruments. Toyota’s portfolio of derivative

financial instruments consists of forward foreign currency

exchange contracts, foreign currency options, interest rate

swaps, interest rate currency swap agreements and interest

rate options. Anticipated transactions denominated in

foreign currencies that are covered by Toyota’s derivative

hedging are not included in the market risk analysis.

Although operating leases are not required to be included,

Toyota has included these instruments in determining

interest rate risk.