Toyota 2005 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2005 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

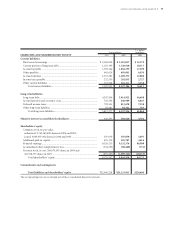

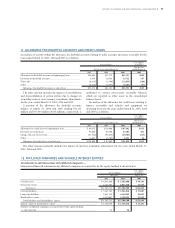

86 >NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FAS 154 applies to all voluntary changes in accounting

principle. It also applies to changes required by an

accounting pronouncement when the pronouncement

does not include specific transition provisions. APB

Opinion 20 previously required that most voluntary changes

in accounting principle be recognized by including in net

income of the period of the change the cumulative effect

of changing to the new accounting principle. FAS 154

requires retrospective application to prior periods’ finan-

cial statements of changes in accounting principle. FAS

154 is effective for accounting changes and corrections of

errors made in fiscal years beginning after December 15,

2005. The impact of applying FAS 154 will depend on the

change, if any, that Toyota may identify and record in

future periods.

Reclassifications—

Certain prior year amounts have been reclassified to conform

to the presentations for the year ended March 31, 2005.

U.S. dollar amounts presented in the consolidated

financial statements and related notes are included solely

for the convenience of the reader and are unaudited.

These translations should not be construed as

representations that the yen amounts actually represent,

or have been or could be converted into, U.S. dollars. For

this purpose, the rate of ¥107.39 = U.S. $1, the approxi-

mate current exchange rate at March 31, 2005, was used

for the translation of the accompanying consolidated

financial amounts of Toyota as of and for the year ended

March 31, 2005.

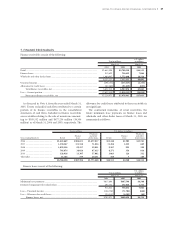

3. U.S. DOLLAR AMOUNTS

Cash payments for income taxes were ¥584,969 million,

¥627,483 million and ¥694,985 million ($6,472 million)

for the years ended March 31, 2003, 2004 and 2005,

respectively. Interest payments during the years ended

March 31, 2003, 2004 and 2005 were ¥216,888 million,

¥203,257 million and ¥226,615 million ($2,110 million),

respectively.

Capital lease obligations of ¥13,461 million, ¥4,826

million and ¥3,571 million ($33 million) were incurred

for the years ended March 31, 2003, 2004 and 2005,

respectively.

For the year ended March 31, 2005, Toyota decided to

change its presentation of cash flows attributed to a

certain portion of finance receivables in the consolidated

statements of cash flows. Certain prior-period amounts

have been reclassified to conform to the current year

presentation. The decision to change the classification was

based on concerns raised by the staff of the Division of

Corporation Finance of the Securities and Exchange

Commission. Historically, Toyota had reported the origi-

nation and collection activities of its wholesale financing

transactions as investing activities in the consolidated

statements of cash flows. Consequently, when Toyota’s

products were sold to its dealers through the use of

Toyota’s wholesale financing program, investing cash

outflows were reported on the basis that the Financial

Services operations originated the wholesale finance

receivables, while operating cash inflows were reported on

the basis that the Automotive sales operations collected

the trade receivables despite the fact that no cash received

from a consolidated perspective related to the trade

receivables as it was an intercompany transaction. The

change in classification in the statements of cash flows for

all periods presented reflects the fact that no cash was

received by Toyota upon a sale to dealers and as a result,

eliminates the effects of the intercompany transactions

and reflects cash receipts from the sale of inventory as

operating activities. In addition, the cash flows from

finance receivables relating to the sale of Toyota product

inventories, other than the above-described wholesale

receivables, were also reclassified from investing activities

to operating activities. Such cash flows include cash flows

from sales-type lease receivables attributed to sales-type

lease transactions involving inventories of Toyota

products. The current presentation in the statements of

cash flows reflects all cash flows relating to the sale of

inventories as “Changes in accounts and notes receivable”

in operating activities. Net cash outflows from finance

receivables relating to the sale of inventories reported in

operating activities in the consolidated statements of cash

flows for the year ended March 31, 2005 was ¥55,951

million ($521 million).

The table below is a reconciliation of Toyota’s current

year presentation of cash flows attributed to finance

receivables compared to the presentation of cash flows

reported in prior years.

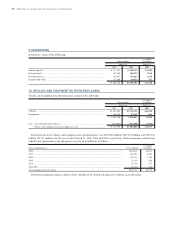

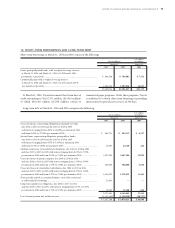

4. SUPPLEMENTAL CASH FLOW INFORMATION