Toyota 2009 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2009 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

Financial Section

TOYOTA MOTOR CORPORATION

76

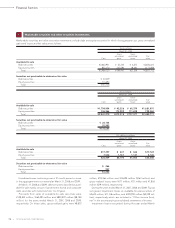

Toyota maintains a program to sell retail and finance lease

receivables. Under the program, Toyota’s securitization transac-

tions are generally structured as qualifying SPEs (“QSPE”s), thus

Toyota achieves sale accounting treatment under the provisions

of FAS No. 140, Accounting for Transfers and Servicing of

Financial Assets and Extinguishments of Liabilities (“FAS 140”).

Toyota recognizes a gain or loss on the sale of the finance

receivables upon the transfer of the receivables to the securiti-

zation trusts structured as a QSPE. Toyota retains servicing rights

and earns a contractual servicing fee of 1% per annum on the

total monthly outstanding principal balance of the related secu-

ritized receivables. In a subordinated capacity, Toyota retains

interest-only strips, subordinated securities, and cash reserve

funds in these securitizations, and these retained interests are

held as restricted assets subject to limited recourse provisions

and provide credit enhancement to the senior securities in

Toyota’s securitization transactions. The retained interests are

not available to satisfy any obligations of Toyota. Investors in the

securitizations have no recourse to Toyota beyond the contrac-

tual cash flows of the securitized receivables, retained subordi-

nated interests, any cash reserve funds and any amounts

available or funded under the revolving liquidity notes. Toyota’s

exposure to these retained interests exists until the associated

securities are paid in full. Investors do not have recourse to

other assets held by Toyota for failure of obligors on the receiv-

ables to pay when due or otherwise.

During the year ended March 31, 2008, Toyota sold mortgage

loan receivables, while no other retail and finance lease receiv-

ables were securitized. During the year ended March 31, 2009,

no retail and finance lease receivables were securitized.

Toyota sold finance receivables under the program and rec-

ognized pretax gains resulting from these sales of ¥1,589 million

and ¥1,688 million for the years ended March 31, 2007 and 2008,

respectively, after providing an allowance for estimated credit

losses. The gain on sale recorded depends on the carrying

amount of the assets at the time of the sale. The carrying

amount is allocated between the assets sold and the retained

interests based on their relative fair values at the date of the

sale. The key economic assumptions initially and subsequently

measuring the fair value of retained interests include the market

interest rate environment, severity and rate of credit losses, and

the prepayment speed of the receivables. All key economic

assumptions used in the valuation of the retained interests are

reviewed periodically and are revised as considered necessary.

At March 31, 2008 and 2009, Toyota’s retained interests relating

to these securitizations include interest in trusts, interest-only

strips, and other receivables, amounting to ¥23,876 million and

¥19,581 million ($199 million), respectively.

Toyota recorded no impairments on retained interests for the

years ended March 31, 2007, 2008 and 2009. Impairments are

calculated, if any, by discounting cash flows using management’s

estimates and other key economic assumptions.

Expected cumulative static pool losses over the life of the

securitizations are calculated by taking actual life to date losses

plus projected losses and dividing the sum by the original bal-

ance of each pool of assets. Expected cumulative static pool

credit losses for finance receivables securitized for the years

ended March 31, 2007, 2008 and 2009 were 0.16%, 0.26% and

0.26%, respectively.

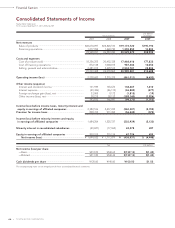

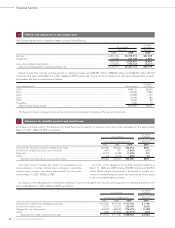

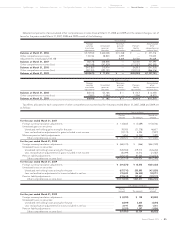

The following table summarizes certain cash flows received from and paid to the securitization trusts for the years ended March 31,

2007, 2008 and 2009.

U.S. dollars

Yen in millions in millions

For the year ended

For the years ended March 31, March 31,

2007 2008 2009 2009

Proceeds from new securitizations, net of purchased and retained securities .............. ¥69,018 ¥91,385 ¥ — $—

Servicing fees received ....................................................................................................... 1,881 1,682 777 8

Excess interest received from interest only strips ............................................................. 2,818 1,865 356 4

Repurchases of receivables................................................................................................. — (4,681) (48) (0)

Servicing advances .............................................................................................................. (234) (114) — —

Reimbursement of servicing and maturity advances ........................................................ 234 114 — —

Key economic assumptions used in measuring the fair value of retained interests at the sale date of securitization transactions com-

pleted during the years ended March 31, 2007, 2008 and 2009 were as follows:

For the years ended March 31,

2007 2008 2009

Prepayment speed related to securitizations ......................................................................... 0.7%–1.4% 6.0% —

Weighted-average life (in years) .............................................................................................. 1.90–2.57 9.00 —

Expected annual credit losses ................................................................................................. 0.05%–0.12% 0.05% —

Discount rate used on the retained interests ......................................................................... 5.0% 3.8% —