Coca Cola 2013 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2013 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

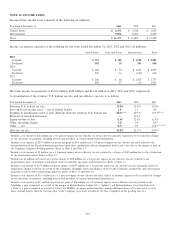

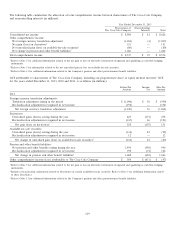

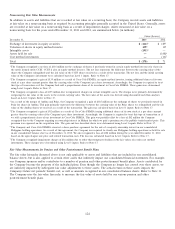

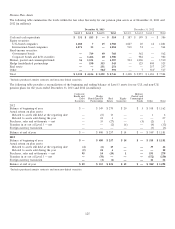

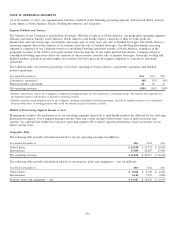

Nonrecurring Fair Value Measurements

In addition to assets and liabilities that are recorded at fair value on a recurring basis, the Company records assets and liabilities

at fair value on a nonrecurring basis as required by accounting principles generally accepted in the United States. Generally, assets

are recorded at fair value on a nonrecurring basis as a result of impairment charges. Assets measured at fair value on a

nonrecurring basis for the years ended December 31, 2013 and 2012, are summarized below (in millions):

Gains (Losses)

December 31, 2013 2012

Exchange of investment in equity securities $ (114)1$ 1854

Valuation of shares in equity method investee 1392105

Intangible assets (195)3—

Assets held for sale —(108)6

Cost method investments —(16)7

Total $ (170) $71

1The Company recognized a net loss of $114 million on the exchange of shares it previously owned in certain equity method investees for shares in

the newly formed entity CCEJ. CCEJ is also an equity method investee. The net loss represents the difference between the carrying value of the

shares the Company relinquished and the fair value of the CCEJ shares received as a result of the transaction. The net loss and the initial carrying

value of the Company’s investment were calculated based on Level 1 inputs. Refer to Note 17.

2The Company recognized a gain of $139 million as a result of Coca-Cola FEMSA, an equity method investee, issuing additional shares of its own

stock at a per share amount greater than the carrying value of the Company’s per share investment. Accordingly, the Company is required to treat

this type of transaction as if the Company had sold a proportionate share of its investment in Coca-Cola FEMSA. These gains were determined

using Level 1 inputs. Refer to Note 17.

3The Company recognized a loss of $195 million due to impairment charges on certain intangible assets. The charges were primarily determined by

comparing the fair value of the assets to the current carrying value. The fair value of the assets was derived using discounted cash flow analyses

based on Level 3 inputs. Refer to Note 17.

4As a result of the merger of Andina and Polar, the Company recognized a gain of $185 million on the exchange of shares we previously owned in

Polar for shares in Andina. This gain primarily represents the difference between the carrying value of the Polar shares we relinquished and the fair

value of the Andina shares we received as a result of the transaction. The gain was calculated based on Level 1 inputs. Refer to Note 17.

5The Company recognized a gain of $92 million as a result of Coca-Cola FEMSA issuing additional shares of its own stock at a per share amount

greater than the carrying value of the Company’s per share investment. Accordingly, the Company is required to treat this type of transaction as if

we sold a proportionate share of our investment in Coca-Cola FEMSA. This gain was partially offset by a loss of $82 million the Company

recognized due to the Company acquiring an ownership interest in Mikuni for which we paid a premium over the publicly traded market price. This

premium was expensed on the acquisition date. The gain and loss described above were determined using Level 1 inputs. Refer to Note 17.

6The Company and Coca-Cola FEMSA executed a share purchase agreement for the sale of a majority ownership interest in our consolidated

Philippine bottling operations. As a result of this agreement, the Company was required to classify our Philippine bottling operations as held for sale

in our consolidated balance sheet as of December 31, 2012. We also recognized a loss of $108 million during the year ended December 31, 2012,

based on the agreed-upon sale price and related transaction costs. The loss was calculated based on Level 3 inputs. Refer to Note 17.

7The Company recognized impairment charges of $16 million due to other-than-temporary declines in the fair values of certain cost method

investments. These charges were determined using Level 3 inputs. Refer to Note 17.

Fair Value Measurements for Pension and Other Postretirement Benefit Plans

The fair value hierarchy discussed above is not only applicable to assets and liabilities that are included in our consolidated

balance sheets, but is also applied to certain other assets that indirectly impact our consolidated financial statements. For example,

our Company sponsors and/or contributes to a number of pension and other postretirement benefit plans. Assets contributed by

the Company become the property of the individual plans. Even though the Company no longer has control over these assets, we

are indirectly impacted by subsequent fair value adjustments to these assets. The actual return on these assets impacts the

Company’s future net periodic benefit cost, as well as amounts recognized in our consolidated balance sheets. Refer to Note 13.

The Company uses the fair value hierarchy to measure the fair value of assets held by our various pension and other

postretirement benefit plans.

124