Coca Cola 2013 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2013 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

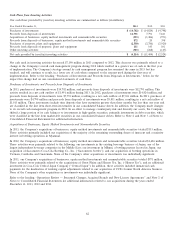

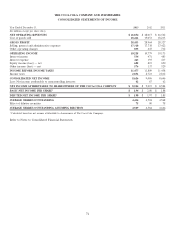

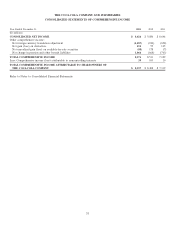

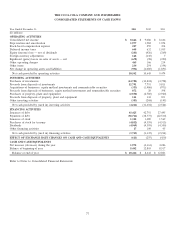

Interest Rates

The Company is subject to interest rate volatility with regard to existing and future issuances of debt. We monitor our mix of

fixed-rate and variable-rate debt, as well as our mix of short-term debt versus long-term debt. From time to time, we enter into

interest rate swap agreements to manage our exposure to interest rate fluctuations.

Based on the Company’s variable-rate debt and derivative instruments outstanding as of December 31, 2013, a 1 percentage point

increase in interest rates would have increased interest expense by $146 million in 2013. However, this increase in interest expense

would have been partially offset by the increase in interest income related to higher interest rates.

In 2012, we changed our overall cash management program and made additional investments in highly liquid debt securities. As a

result, we are exposed to interest rate risk related to these investments. These investments are primarily managed by external

managers within the guidelines of the Company’s investment policy. Our policy requires investments to be investment grade, with

the primary objective of minimizing the potential risk of principal loss. In addition, our policy limits the amount of credit exposure

to any one issuer. We estimate that a 1 percentage point increase in interest rates would result in a $35 million decrease in the

fair market value of the portfolio.

Commodity Prices

The Company is subject to market risk with respect to commodity price fluctuations, principally related to our purchases of

sweeteners, metals, juices and fuels. Whenever possible, we manage our exposure to commodity risks primarily through the use of

supplier pricing agreements that enable us to establish the purchase prices for certain inputs that are used in our manufacturing

and distribution business. We also use derivative financial instruments to manage our exposure to commodity risks at times.

Certain of these derivatives do not qualify for hedge accounting, but they are effective economic hedges that help the Company

mitigate the price risk associated with the purchases of materials used in our manufacturing processes and the fuel used to

operate our extensive vehicle fleet.

Open commodity derivatives that qualify for hedge accounting had notional values of $26 million and $17 million as of

December 31, 2013 and 2012, respectively. The fair value of the contracts that qualify for hedge accounting resulted in an asset of

less than $1 million. The potential change in fair value of these commodity derivative instruments, assuming a 10 percent decrease

in underlying commodity prices, would have resulted in a net loss of $3 million.

Open commodity derivatives that do not qualify for hedge accounting had notional values of $1,441 million and $1,084 million as

of December 31, 2013 and 2012, respectively. The fair value of the contracts that do not qualify for hedge accounting resulted in

an asset of $11 million. The potential change in fair value of these commodity derivative instruments, assuming a 10 percent

decrease in underlying commodity prices, would have eliminated our net unrealized gain and created an unrealized loss of

$79 million.

72