Coca Cola 2013 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2013 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

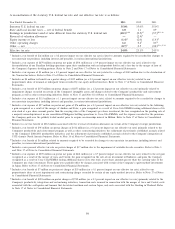

We have significant operations outside the United States. Unit case volume outside the United States represented 81 percent of

the Company’s worldwide unit case volume in 2013. We earn a substantial amount of our consolidated operating income and

income before income taxes in foreign subsidiaries that either sell concentrate to our local bottling partners or, in certain

instances, sell finished products directly to our customers to fulfill the demand for Company beverage products outside the United

States. A significant portion of these foreign earnings is considered to be indefinitely reinvested in foreign jurisdictions. The

Company’s cash, cash equivalents, short-term investments and marketable securities held by our foreign subsidiaries totaled

$18.3 billion as of December 31, 2013. With the exception of an insignificant amount, for which U.S. federal and state income

taxes have already been provided, we do not intend, nor do we foresee a need, to repatriate these funds. Additionally, the absence

of a government-approved mechanism to convert local currency into U.S. dollars in Argentina and Venezuela restricts the

Company’s ability to pay dividends from these locations. As of December 31, 2013, the Company’s subsidiaries in Argentina and

Venezuela held $353 million and $324 million, respectively, of cash, cash equivalents, short-term investments and marketable

securities.

Net operating revenues in the United States were $19.8 billion in 2013, or 42 percent of the Company’s consolidated net operating

revenues. We expect existing domestic cash, cash equivalents, short-term investments, marketable securities, cash flows from

operations and the issuance of debt to continue to be sufficient to fund our domestic operating activities and cash commitments

for investing and financing activities. In addition, we expect existing foreign cash, cash equivalents, short-term investments,

marketable securities and cash flows from operations to continue to be sufficient to fund our foreign operating activities and cash

commitments for investing activities.

In the future, should we require more capital to fund significant discretionary activities in the United States than is generated by

our domestic operations or is available through the issuance of debt, we could elect to repatriate future periods’ earnings from

foreign jurisdictions. This alternative could result in a higher effective tax rate. While the likelihood is remote, the Company could

also elect to repatriate earnings from foreign jurisdictions that have previously been considered to be indefinitely reinvested. Upon

distribution of those earnings in the form of dividends or otherwise, the Company would be subject to additional U.S. income

taxes (net of an adjustment for foreign tax credits) and withholding taxes payable to various foreign jurisdictions, where applicable.

This alternative could also result in a higher effective tax rate in the period in which such a determination is made to repatriate

prior period foreign earnings. Refer to Note 14 of Notes to Consolidated Financial Statements for further information related to

our income taxes and undistributed earnings of the Company’s foreign subsidiaries.

Based on all the aforementioned factors, the Company believes its current liquidity position is strong, and we will continue to

meet all of our financial commitments for the foreseeable future. These commitments include, but are not limited to, regular

quarterly dividends, debt maturities, capital expenditures, share repurchases and obligations included under the heading

‘‘Off-Balance Sheet Arrangements and Aggregate Contractual Obligations’’ below.

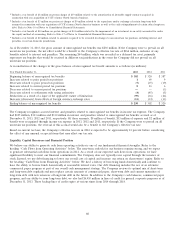

Cash Flows from Operating Activities

Net cash provided by operating activities for the years ended December 31, 2013, 2012 and 2011 was $10,542 million,

$10,645 million and $9,474 million, respectively.

Cash flows from operating activities decreased $103 million, or 1 percent, in 2013 compared to 2012. This decrease primarily

reflects the impact of foreign currency fluctuations, an increase in tax payments and the effect of the deconsolidation of our

Philippine and Brazilian bottling operations during 2013, partially offset by lower pension funding in 2013 compared to 2012.

Refer to Note 2 of the Notes to Consolidated Financial Statements for additional information on the deconsolidation of these

bottling operations. Refer to the heading ‘‘Operations Review — Net Operating Revenues’’ above for additional information on

the impact of foreign currency fluctuations. Refer to Note 13 and Note 14 of Notes to Consolidated Financial Statements for

additional information on the pension funding and tax payments.

Cash flows from operating activities increased $1,171 million, or 12 percent, in 2012 compared to 2011. This increase reflects

higher receipts from customers, lower tax payments and the favorable impact of the Company discontinuing its temporary

extension of credit terms in Japan. The favorable impact of the previous items was partially offset by the unfavorable impact of

foreign currency fluctuations and an increase in contributions to our pension plans.

The Company discontinued the temporary extension of its credit terms in Japan during the first quarter of 2012. We originally

extended our credit terms in Japan during the second quarter of 2011 as a result of the natural disasters that devastated portions

of the country on March 11, 2011. This change resulted in an increase in cash from operations during the year ended

December 31, 2012.

61