Coca Cola 2013 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2013 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

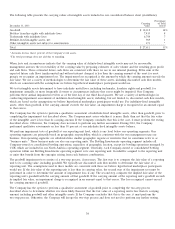

During 2013, the Company performed qualitative assessments on approximately 11 percent of our consolidated goodwill balance.

Intangible assets acquired in recent transactions are naturally more susceptible to impairment, primarily due to the fact that they

are recorded at fair value based on recent operating plans and macroeconomic conditions present at the time of acquisition.

Consequently, if operating results and/or macroeconomic conditions deteriorate shortly after an acquisition, it could result in the

impairment of the acquired assets. A deterioration of macroeconomic conditions may not only negatively impact the estimated

operating cash flows used in our cash flow models, but may also negatively impact other assumptions used in our analyses,

including, but not limited to, the estimated cost of capital and/or discount rates. Additionally, as discussed above, in accordance

with accounting principles generally accepted in the United States, we are required to ensure that assumptions used to determine

fair value in our analyses are consistent with the assumptions a hypothetical marketplace participant would use. As a result, the

cost of capital and/or discount rates used in our analyses may increase or decrease based on market conditions and trends,

regardless of whether our Company’s actual cost of capital has changed. Therefore, if the cost of capital and/or discount rates

change, our Company may recognize an impairment of an intangible asset in spite of realizing actual cash flows that are

approximately equal to, or greater than, our previously forecasted amounts.

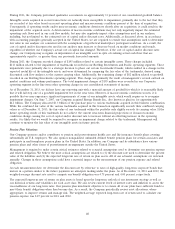

During 2013, the Company recorded charges of $195 million related to certain intangible assets. These charges included

$113 million related to the impairment of trademarks recorded in our Bottling Investments and Pacific operating segments. These

impairments were primarily due to a strategic decision to phase out certain local-market brands, which resulted in a change in the

expected useful life of the intangible assets, and were determined by comparing the fair value of the trademarks, derived using

discounted cash flow analyses, to the current carrying value. Additionally, the remaining charge of $82 million related to goodwill

recorded in our Bottling Investments operating segment. This charge was primarily the result of management’s revised outlook on

market conditions and volume performance. The total impairment charges of $195 million were recorded in our Corporate

operating segment in the line item other operating charges in our consolidated statements of income.

As of December 31, 2013, we did not have any reporting unit with a material amount of goodwill for which it is reasonably likely

that it will fail step one of a goodwill impairment test in the near term. However, if macroeconomic conditions worsen, it is

possible that we may experience significant impairments of some of our intangible assets, which would require us to recognize

impairment charges. On June 7, 2007, our Company acquired Energy Brands Inc., also known as glac´

eau, for approximately

$4.1 billion. The Company allocated $3.3 billion of the purchase price to various trademarks acquired in this business combination.

While the combined fair value of the various trademarks acquired in this transaction significantly exceeds their combined carrying

values as of December 31, 2013, the fair value of one trademark within the portfolio only slightly exceeds its carrying value. If the

future operating results of this trademark do not achieve the current near-term financial projections or if macroeconomic

conditions change causing the cost of capital and/or discount rate to increase without an offsetting increase in the operating

results, it is likely that we would be required to recognize an impairment charge related to this trademark. Management will

continue to monitor the fair value of our intangible assets in future periods.

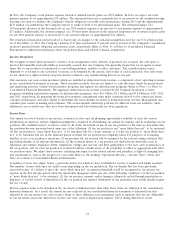

Pension Plan Valuations

Our Company sponsors and/or contributes to pension and postretirement health care and life insurance benefit plans covering

substantially all U.S. employees. We also sponsor nonqualified, unfunded defined benefit pension plans for certain associates and

participate in multi-employer pension plans in the United States. In addition, our Company and its subsidiaries have various

pension plans and other forms of postretirement arrangements outside the United States.

Management is required to make certain critical estimates related to actuarial assumptions used to determine our pension expense

and related obligation. We believe the most critical assumptions are related to (1) the discount rate used to determine the present

value of the liabilities and (2) the expected long-term rate of return on plan assets. All of our actuarial assumptions are reviewed

annually. Changes in these assumptions could have a material impact on the measurement of our pension expense and related

obligation.

At each measurement date, we determine the discount rate by reference to rates of high-quality, long-term corporate bonds that

mature in a pattern similar to the future payments we anticipate making under the plans. As of December 31, 2013 and 2012, the

weighted-average discount rate used to compute our benefit obligation was 4.75 percent and 4.00 percent, respectively.

The expected long-term rate of return on plan assets is based upon the long-term outlook of our investment strategy as well as

our historical returns and volatilities for each asset class. We also review current levels of interest rates and inflation to assess the

reasonableness of our long-term rates. Our pension plan investment objective is to ensure all of our plans have sufficient funds to

meet their benefit obligations when they become due. As a result, the Company periodically revises asset allocations, where

appropriate, to improve returns and manage risk. The weighted-average expected long-term rate of return used to calculate our

pension expense was 8.25 percent in 2013 and 2012.

40