Starbucks 2009 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2009 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

|

|

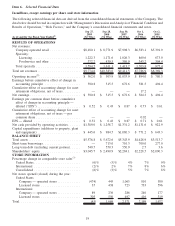

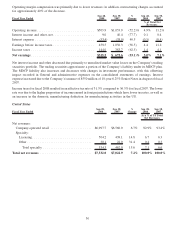

stores in the US and approximately 200 net new stores in International markets. Both the US and International net

new additions are expected to be primarily licensed stores.

Given these revenue expectations, combined with the Company’s reduced cost structure, in-store operating

efficiencies, and lower restructuring charges, Starbucks currently expects significant improvement in its consol-

idated operating margin in fiscal 2010. Operating cash flow for fiscal 2010 is currently expected to reach

approximately $1.4 billion and capital expenditures are expected to range from $500 million to $550 million.

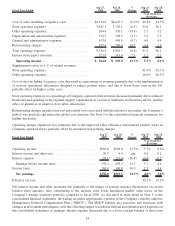

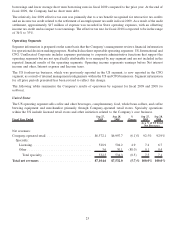

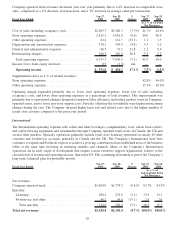

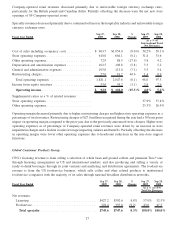

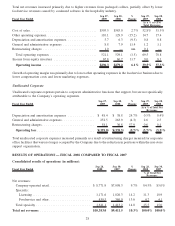

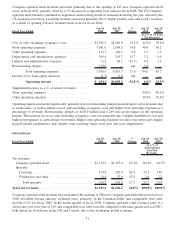

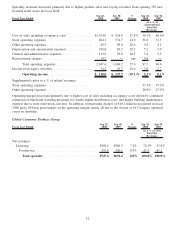

Operating Segment Overview

Starbucks has three reportable operating segments: US, International and CPG. The US foodservice business, which

was previously reported in the US segment, is now reported in the CPG segment, as a result of internal management

realignments within the US and CPG businesses. Segment information for all prior periods presented has been

revised to reflect this change.

The US and International segments bothinclude Company-operated retail stores and licensed retail stores. Licensed

stores frequently have a higher operating margin than Company-operated stores. Under the licensed model,

Starbucks receives a reduced share of the total store revenues, but this is more than offset by the reduction in its

share of costs as these are primarily borne by the licensee. The International segment has a higher relative share of

licensed stores versus Company-operated compared to the US segment; however, the US segment has been

operating significantly longer than the International segment and has developed deeper awareness of, and

attachment to, the Starbucks brand and stores among its customer base. As a result, the more mature US segment

has significantly more stores, and higher total revenues than the International segment. Average sales per store are

also higher in the US due to various factors including length of time in market and local income levels. Further,

certain market costs, particularly occupancy costs, are lower in the US segment compared to the average for the

International segment, which comprises a more diverse group of operations. As a result of the relative strength of the

brand in the US segment, the number of stores, the higher unit volumes, and the lower market costs, the US segment,

despite its higher relative percentage of Company-operated stores, has a higher operating margin, excluding

restructuring costs, than the less-developed International segment.

The Company’s International store base continues to expand and Starbucks has been focusing on achieving

sustainable growth from established international markets while at the same time investing in emerging markets,

such as China, Brazil and Russia. The Company’s newer international markets require a more extensive support

organization, relative to the current levels of revenue and operating income.

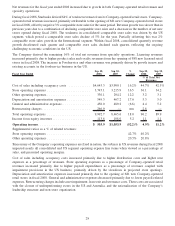

The CPG segment includes packaged coffee and tea, and other branded products operations worldwide, and the US

foodservice business. For the packaged coffee and tea and branded products, Starbucks operates primarily through

licensing arrangements and joint ventures with large consumer products business partners, most significantly with

Kraft for distribution of packaged coffees and teas, and The North American Coffee Partnership with the Pepsi-Cola

Company for manufacturing and distribution of ready-to-drink beverages. This operating model allows the CPG

segment to leverage the business partners’ existing infrastructures and to extend the Starbucks brand in an efficient

way. Most of the customer revenues from the packaged coffee and ready-to-drink products are recognized as

revenues by the licensed or joint venture business partner, not by the CPG segment. Royalties and payments from

our licensing agreements are recorded under licensing revenue, and the proportionate share of the results of the

Company’s joint ventures are included, on a net basis, in Income from equity investees on the consolidated

statements of earnings. The US foodservice business sells coffee and other related products to institutional

foodservice companies with the majority of its sales through national broadline distribution networks. The CPG

segment reflects relatively lower revenues, a modest cost structure, and a resulting higher operating margin,

compared to the Company’s other two reporting segments, which consist primarily of retail stores.

Expenses pertaining to corporate administrative functions that support the operating segments but are not

specifically attributable to or managed by any segment are not included in the reported financial results of the

operating segments. These unallocated corporate expenses include certain general and administrative expenses,

related depreciation and amortization expenses, corporate restructuring charges and amounts included in Net

interest income and other and Interest expense on the consolidated statements of earnings.

22