Starbucks 2009 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2009 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

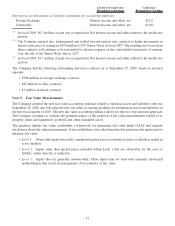

|

|

options for a lesser amount of new options to be granted with lower exercise prices. Stock options eligible for

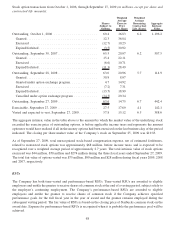

exchange were those with an exercise price per share greater than $19.00 that were granted prior to December 1,

2007 under the Company’s Amended and Restated 2005 Long-Term Equity Incentive Plan (the “2005 Plan”), the

Amended and Restated Key Employee Stock Option Plan-1994 or the 1991 Company-Wide Stock Option Plan. On

May 1, 2009 Starbucks commenced the option exchange program, which expired on May 29, 2009. A total of

14.3 million eligible stock options were tendered by employees, representing 65% of the total stock options eligible

for exchange. On June 1, 2009, the Company granted an aggregate of 4.7 million new stock options in exchange for

the eligible stock options surrendered. The exercise price of the new stock options was $14.92, which was the

closing price of Starbucks common stock on June 1, 2009. The new stock options were granted under the 2005 Plan.

No incremental stock option expense was recognized for the exchange because the fair value of the new options,

using standard employee stock option valuation techniques, was approximately equal to the fair value of the

surrendered options they replaced.

The fair value of stock option awards and ESPP shares was estimated at the grant date with the following weighted

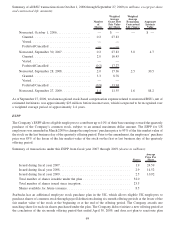

average assumptions for the fiscal years ended September 27, 2009, September 28, 2008 and September 30, 2007

(excludes options granted in the 2009 stock option exchange program described above):

Fiscal Year Ended 2009 2008 2007 2009 2008 2007

Employee Stock Options

Granted During the Period ESPP

Expected term (in years) .... 4.9 4.7 4.7 0.25 - 0.5 0.25 - 0.5 0.25 - 0.5

Expected stock price

volatility .............. 44.5% 29.3% 28.9% 37% - 64% 26% - 44% 28% - 31%

Risk-free interest rate ...... 2.2% 3.4% 4.6% 0.2% - 1.7% 1.3% - 4.5% 4.7% - 5.1%

Expected dividend yield..... 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Weighted average grant

price ................. $8.97 $22.11 $36.04 $ 10.92 $ 14.52 $ 24.59

Estimated fair value per

option granted .......... $3.61 $ 6.85 $11.72 $ 2.67 $ 4.00 $ 6.03

The expected term of the options represents the estimated period of time until exercise and is based on historical

experience of similar awards, giving consideration to the contractual terms, vesting schedules and expectations of

future employee behavior. Expected stock price volatility is based on a combination of historical volatility of the

Company’s stock and the one-year implied volatility of its traded options, for the related vesting periods. The risk-

free interest rate is based on the implied yield available on US Treasury zero-coupon issues with an equivalent

remaining term. As the Company does not pay dividends, the dividend yield is 0%. The amounts shown above for

the estimated fair value per option granted are before the estimated effect of forfeitures, which reduce the amount of

expense recorded on the consolidated statement of earnings.

The BSM option valuation model was developed for use in estimating the fair value of traded options, which have

no vesting restrictions and are fully transferable. The Company’s employee stock options have characteristics

significantly different from those of traded options, and changes in the subjective input assumptions can materially

affect the fair value estimate. Because Starbucks stock options do not trade on a secondary exchange, employees do

not derive a benefit from holding stock options unless there is an increase, above the grant price, in the market price

of the Company’s stock. Such an increase in stock price would benefit all shareholders commensurately.

67