Sysco 2008 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2008 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

fiscal 2008, and operations to service our five broadline operating companies in Florida began in April 2008. In fiscal 2009, we intend to

service additional broadline companies from our existing RDCs.

We will continue to use our strategic business initiatives to leverage our market leadership position to continuously improve how we

buy, handle and market products for our customers. Our primary focus is on growing and optimizing the core foodservice distribution

business in North America, however we will also continue to explore and identify opportunities to grow our global capabilities and stay

abreast of international acquisition opportunities.

As a part of our on going strategic analysis, we regularly evaluate business opportunities, including potential acquisitions and sales of

assets and businesses.

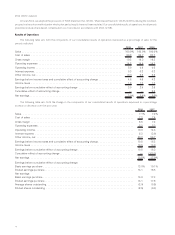

Accounting Changes

FIN 48 Adoption

As of July 1, 2007, we adopted FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes — an Interpretation of FASB

Statement No. 109” (FIN 48), which clarifies the accounting for uncertainty in income taxes recognized in accordance with SFAS No. 109,

“Accounting for Income Taxes” (SFAS 109). FIN 48 clarifies the application of SFAS 109 by defining criteria that an individual tax position

must meet for any part of the benefit of that position to be recognized in the financial statements. Additionally, FIN 48 provides guidance on

the measurement, derecognition, classification and disclosure of tax positions, along with accounting for the related interest and penalties.

As a result of this adoption, we recognized, as a cumulative effect of change in accounting principle, a $91,635,000 decrease in our

beginning retained earnings on our July 1, 2007 balance sheet.

Pension Measurement Date Change and SFAS 158 Adoption

As of June 30, 2007, we adopted the recognition and disclosure provisions of SFAS No. 158, “Employers’Accounting for Defined Benefit

Pension and Other Postretirement Plans — an amendment of FASB Statements No. 87, 88, 106, and 132(R)” (SFAS 158). The recognition

provision requires an employer to recognize a plan’s funded status in its statement of financial position and recognize the changes in a

postretirement benefit plan’s funded status in comprehensive income in the year in which the changes occur. The effect of adoption on our

consolidated balance sheet as of June 30, 2007 was a decrease in prepaid pension cost of $83,846,000, a decrease in other assets of

$43,854,000, an increase in accrued expenses of $10,967,000, a decrease in long-term deferred taxes of $73,328,000, an increase in other

long-term liabilities of $52,289,000, and a charge to accumulated other comprehensive loss of $117,628,000. The adoption of SFAS 158’s

recognition provision did not have an effect on our consolidated balance sheet as of July 1, 2006. The adoption has no effect on our

consolidated results of operations for any period presented, and it will not affect our consolidated results of operations in future periods.

SFAS 158 also has a measurement date provision, which is a requirement to measure plan assets and benefit obligations as of the date

of the employer’s fiscal year-end statement of financial position, effective for fiscal years ending after December 15, 2008. In the first quarter

of fiscal 2006, we changed the measurement date for company-sponsored pension and other postretirement benefit plans from fiscal year-

end to May 31st to assist us in meeting accelerated SEC filing dates. As a result of this change, we recorded a cumulative effect of a change in

accounting, which increased net earnings for fiscal 2006 by $9,285,000, net of tax. With the issuance of SFAS 158, we have elected to early

adopt the measurement date provision in order to adopt both provisions of this accounting standard at the same time. As a result, beginning

with fiscal 2008, the measurement date again corresponded with our fiscal year-end.We performed measurements as of May 31, 2007 and

June 30, 2007 of our plan assets and benefit obligations. We recorded a charge to beginning retained earnings on July 1, 2007 of

$3,572,000, net of tax, for the impact of the cumulative difference in our pension expense between the two measurement dates. We also

recorded a benefit to beginning accumulated other comprehensive income (loss) on July 1, 2007 of $22,780,000, net of tax, for the impact

of the difference in our balance sheet recognition provision between the two measurement dates.

EITF 04-13 Adoption

In the beginning of the fourth quarter of fiscal 2006, we adopted accounting pronouncement EITF 04-13 “Accounting for Purchases and

Sales of Inventory with the Same Counterparty,” (EITF 04-13). The accounting standard requires certain transactions, where inventory is

purchased by us from a customer and then resold at a later date to the same customer (as defined), to be presented in the income statement

on a net basis. This situation primarily arises for SYSCO when a customer has a proprietary item which they have either manufactured or

sourced, but they require our distribution and logistics capabilities to get the product to their locations. The application of this standard

requires sales and cost of sales to be reduced by the same amount for these transactions and thus net earnings are unaffected by the

application of this standard.We adopted this accounting pronouncement beginning in the fourth quarter of fiscal 2006 and have applied it to

similar transactions prospectively. Prior period sales and cost of sales have not been restated.Therefore, the calculation of sales growth and

the comparison of gross margins, operating expenses and earnings as a percentage of sales between the non-comparable periods is

affected. The impact of adopting this standard resulted in sales being reduced by $99,803,000 for the fourth quarter of fiscal 2006, and

$253,724,000 for the first 39 weeks of fiscal 2007, without a reduction in sales for the comparable prior year periods. Beginning with the

fourth quarter of fiscal 2007, sales are reported on a comparable accounting basis with the comparable prior year period.

13