Sysco 2008 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2008 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

|

|

FIN 48

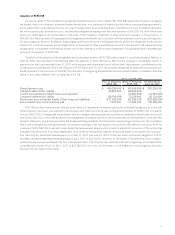

Prior to fiscal 2008, in evaluating the exposures connected with the various tax filing positions, the company established an accrual

when, despite management’s belief that the company’s tax return positions are supportable, management believed that certain positions

may be successfully challenged and a loss was probable. When facts and circumstances changed, these accruals were adjusted.

As discussed in Note 2, Changes in Accounting, the company adopted FIN 48 effective July 1, 2007. FIN 48 provides that a tax benefit

from an uncertain tax position may be recognized when it is more likely than not that the position will be sustained upon examination,

including resolutions of any related appeals or litigation processes, based on the technical merits of the position. The amount recognized is

measured as the largest amount of tax benefit that has a greater than 50% likelihood of being realized upon settlement. As a result of this

adoption, the company recognized, as a cumulative effect of change in accounting principle, a $91,635,000 decrease in its beginning

retained earnings on its July 1, 2007 balance sheet. A reconciliation of the beginning and ending amount of gross unrecognized tax benefits,

excluding interest and penalties, is as follows:

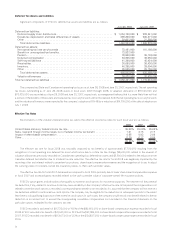

2008

Unrecognized tax benefits at beginning of year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 82,639,000

Additions for tax positions related to prior years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —

Reductions for tax positions related to prior years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (138,000)

Additions for tax positions related to the current year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,912,000

Reductions for tax positions related to the current year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —

Reductions due to settlements with taxing authorities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (223,000)

Reductions due to lapse of applicable statute of limitations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (2,261,000)

Unrecognized tax benefits at end of year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 87,929,000

As of June 28, 2008, the gross amount of accrued interest liabilities was $138,207,000 related to unrecognized tax benefits and

recorded interest expense of $12,287,000 in fiscal 2008. The company does not have any accrued liabilities for penalties related to

unrecognized tax benefits and did not record any expense related to penalties in fiscal 2008. To the extent interest and penalties may be

assessed by taxing authorities on any underpayment of income tax, estimated amounts required under FIN 48 have been accrued and are

classified as a component of income taxes in the consolidated results of operations. This was the company’s accounting policy prior to the

adoption of FIN 48, and SYSCO elected to continue this accounting policy post-adoption.

If SYSCO were to recognize all unrecognized tax benefits recorded as of June 28, 2008, approximately $57,503,000 of the

$87,929,000 reserve would reduce the effective tax rate. It is reasonably possible that the amount of the unrecognized tax benefits

with respect to certain of the company’s unrecognized tax positions will increase or decrease in the next twelve months either because

SYSCO agrees with positions that are sustained on audit or because the company agrees to their disallowance. Items that may cause

changes to unrecognized tax benefits primarily include the consideration of various filing requirements in various states and the allocation of

income and expense between tax jurisdictions. At this time, an estimate of the range of the reasonably possible change cannot be made.

SYSCO is currently in the appeals process as it relates to certain adjustments from the Internal Revenue Service (IRS) in relation to its

audit of the company’s 2003 and 2004 federal income tax returns. See further discussion in Note 18, Commitments and Contingencies,

under the caption “BSCC Cooperative Structure.” The IRS is also auditing SYSCO’s 2005 and 2006 federal income tax returns. As of June 28,

2008, SYSCO’s tax returns in the majority of the state and local jurisdictions and Canada are no longer subject to audit for the years before

2004. However, some jurisdictions have audits open prior to 2004, with the earliest dating back to 1996. Although the outcome of tax

audits is generally uncertain, the company believes that adequate amounts of tax, including interest and penalties, have been accrued for any

adjustments that may result from those years.

Other

The company intends to permanently reinvest the undistributed earnings of its Canadian subsidiaries in those businesses outside of the

United States and, therefore, has not provided for U.S. deferred income taxes on such undistributed foreign earnings. The determination of

the amount of the unrecognized deferred tax liability related to the undistributed earnings is not practicable.

The determination of the company’s provision for income taxes requires significant judgment, the use of estimates and the

interpretation and application of complex tax laws. The company’s provision for income taxes reflects a combination of income earned

and taxed in the various U.S. federal and state, as well as Canadian federal and provincial, jurisdictions. Jurisdictional tax law changes,

increases or decreases in permanent differences between book and tax items, accruals or adjustments of accruals for tax contingencies or

valuation allowances, and the company’s change in the mix of earnings from these taxing jurisdictions all affect the overall effective tax rate.

17. ACQUISITIONS

During fiscal 2008, in the aggregate, the company paid cash of $55,259,000 for operations acquired during fiscal 2008 and for

contingent consideration related to operations acquired in previous fiscal years. The acquisitions were immaterial, individually and in the

aggregate, to the consolidated financial statements. In addition, escrowed funds in the amount of $7,000,000 related to certain acquisitions

were released to sellers of previously acquired businesses during fiscal 2008.

57