Sysco 2008 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2008 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

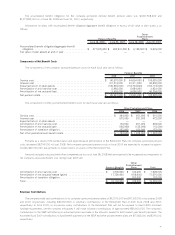

Insurance Program

SYSCO maintains a self-insurance program covering portions of workers’ compensation, general and vehicle liability costs. The

amounts in excess of the self-insured levels are fully insured by third party insurers. The company also maintains a fully self-insured group

medical program. Liabilities associated with these risks are estimated in part by considering historical claims experience, medical cost

trends, demographic factors, severity factors and other actuarial assumptions.

Share-Based Compensation

SYSCO recognizes expense for its share-based compensation based on the fair value of the awards that are granted. The fair value of

the stock options is estimated at the date of grant using the Black-Scholes option pricing model. Option pricing methods require the input of

highly subjective assumptions, including the expected stock price volatility. Measured compensation cost is recognized ratably over the

vesting period of the related share-based compensation award. Cash flows resulting from tax deductions in excess of the compensation cost

recognized for those options (excess tax benefits) are classified as financing cash flows on the consolidated cash flows statements.

Acquisitions

Acquisitions of businesses are accounted for using the purchase method of accounting, and the financial statements include the results

of the acquired operations from the respective dates they joined SYSCO.

The purchase price of the acquired entities is allocated to the net assets acquired and liabilities assumed based on the estimated fair

value at the dates of acquisition, with any excess of cost over the fair value of net assets acquired, including intangibles, recognized as

goodwill. The balances included in the consolidated balance sheets related to recent acquisitions are based upon preliminary information

and are subject to change when final asset and liability valuations are obtained. Material changes to the preliminary allocations are not

anticipated by management.

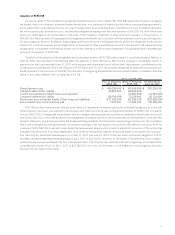

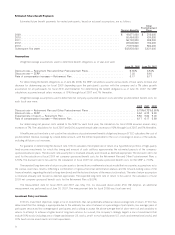

2. CHANGES IN ACCOUNTING

FIN 48

Effective July 1, 2007, SYSCO adopted FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes — an Interpretation of

FASB Statement No. 109” (FIN 48), which clarifies the accounting for uncertainty in income taxes recognized in accordance with

SFAS No. 109, “Accounting for Income Taxes” (SFAS 109). FIN 48 clarifies the application of SFAS 109 by defining criteria that an individual

tax position must meet for any part of the benefit of that position to be recognized in the financial statements. Additionally, FIN 48 provides

guidance on the measurement, derecognition, classification and disclosure of tax positions, along with accounting for the related interest

and penalties. The impact of adopting this standard is discussed in Note 16, Income Taxes.

Pension Measurement Date Change and SFAS 158 Adoption

Beginning in fiscal 2006, SYSCO changed the measurement date for the company-sponsored pension and other postretirement benefit

plans from fiscal year-end to May 31st, which represented a change in accounting. Management believes this accounting change was

preferable, as the one-month acceleration of the measurement date allowed additional time for management to evaluate and report the

actuarial pension measurements in the year-end financial statements and disclosures within the accelerated filing deadlines of the Securities

and Exchange Commission.The cumulative effect of this change in accounting resulted in an increase to earnings in the first quarter of fiscal

2006 of $9,285,000, net of tax.The impact to pro forma net earnings and earnings per share adjusted for the effect of retroactive application

of the change in measurement date on net company-sponsored pension costs for fiscal 2005 was not material.

In September 2006, the FASB issued SFAS No. 158, “Employers’ Accounting for Defined Benefit Pension and Other Postretirement

Plans — an amendment of FASB Statements No. 87, 88, 106, and 132(R)” (SFAS 158). SFAS 158 has two major provisions. The recognition

and disclosure provision requires an employer to recognize a plan’s funded status in its statement of financial position and recognize the

changes in a defined benefit postretirement plan’s funded status in comprehensive income in the year in which the changes occur. The

measurement date provision requires an employer to measure a plan’s assets and obligations as of the end of the employer’s fiscal year.

SYSCO adopted SFAS 158’s recognition and disclosure requirements as of June 30, 2007. In addition, SYSCO elected to early adopt the

measurement date provision in order to adopt both provisions of this accounting standard at the same time. See discussion of the impact of

adoption in Note 12, Employee Benefit Plans.

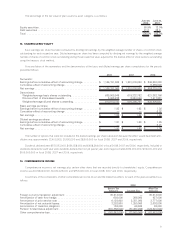

EITF 04-13 Adoption

In September 2005, the Emerging Issues Task Force reached a consensus on EITF 04-13 which requires that two or more inventory

transactions with the same counterparty (as defined) should be viewed as a single nonmonetary transaction if the transactions were entered

into in contemplation of one another. Exchanges of inventory between entities in the same line of business should be accounted for at fair

value or recorded at carrying amounts, depending on the classification of such inventory.This guidance was effective for the fourth quarter of

fiscal 2006 for SYSCO. SYSCO has certain transactions where finished goods are purchased from a customer or sourced by that customer

for warehousing and distribution and resold to the same customer. These transactions are evidenced by title transfer and are separately

41