Sysco 2008 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2008 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

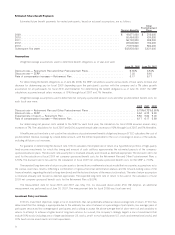

|

|

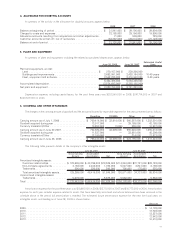

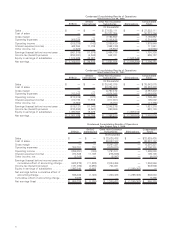

Before-Tax

Amount Income Tax

After-Tax

Amount

2007

Minimum pension liability adjustment . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 5,633,000 $ 2,164,000 $ 3,469,000

Foreign currency translation adjustment . . . . . . . . . . . . . . . . . . . . . . . . . 25,052,000 — 25,052,000

Amortization of cash flow hedge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 694,000 266,000 428,000

Other comprehensive income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 31,379,000 $ 2,430,000 $ 28,949,000

Before-Tax

Amount Income Tax

After-Tax

Amount

2006

Minimum pension liability adjustment . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 70,097,000 $ 26,917,000 $ 43,180,000

Foreign currency translation adjustment . . . . . . . . . . . . . . . . . . . . . . . . . . 47,718,000 — 47,718,000

Change in fair value of interest rate swap . . . . . . . . . . . . . . . . . . . . . . . . 11,388,000 4,324,000 7,064,000

Amortization of cash flow hedge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 540,000 207,000 333,000

Other comprehensive income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 129,743,000 $ 31,448,000 $ 98,295,000

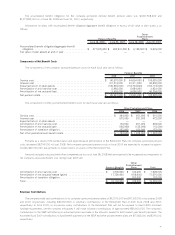

The following table provides a summary of the changes in accumulated other comprehensive income (loss) for the years presented:

Pension and Other

Postretirement

Benefit Plans

Foreign Currency

Translation Interest Rate Swap Total

Balance as of July 2, 2005 . . . . . . . . . . . . . . . . . . $ (54,286,000) $ 60,730,000 $ (20,121,000) $ (13,677,000)

Minimum pension liability adjustment . . . . . . . . . . 43,180,000 — — 43,180,000

Foreign currency translation adjustment . . . . . . . . — 47,718,000 — 47,718,000

Change in fair value of interest rate swap . . . . . . . — — 7,064,000 7,064,000

Amortization of cash flow hedge . . . . . . . . . . . . . — — 333,000 333,000

Balance as of July 1, 2006 . . . . . . . . . . . . . . . . . . (11,106,000) 108,448,000 (12,724,000) 84,618,000

Minimum pension liability adjustment . . . . . . . . . . 3,469,000 — — 3,469,000

Foreign currency translation adjustment . . . . . . . . — 25,052,000 — 25,052,000

Amortization of cash flow hedge . . . . . . . . . . . . . — — 428,000 428,000

Adoption of SFAS 158 recognition provision . . . . . (117,628,000) — — (117,628,000)

Balance as of June 30, 2007 . . . . . . . . . . . . . . . . (125,265,000) 133,500,000 (12,296,000) (4,061,000)

Adoption of SFAS 158 measurement date

provision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22,780,000 — — 22,780,000

Foreign currency translation adjustment . . . . . . . . — 30,514,000 — 30,514,000

Amortization of cash flow hedge . . . . . . . . . . . . . — — 427,000 427,000

Amortization of prior service cost . . . . . . . . . . . . . 3,777,000 — — 3,777,000

Amortization of net actuarial losses . . . . . . . . . . . 2,003,000 — — 2,003,000

Amortization of transition obligation . . . . . . . . . . . 93,000 — — 93,000

Pension funded status adjustment . . . . . . . . . . . . (124,301,000) — — (124,301,000)

Balance as of June 28, 2008 . . . . . . . . . . . . . . . . $ (220,913,000) $ 164,014,000 $ (11,869,000) $ (68,768,000)

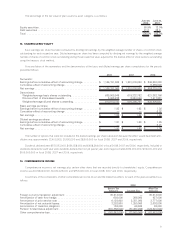

15. SHARE-BASED COMPENSATION

Prior to July 3, 2005, SYSCO accounted for its stock option plans and its Employees’ Stock Purchase Plan using the intrinsic value

method of accounting provided under APB Opinion No. 25, “Accounting for Stock Issued to Employees,” (APB 25) and related

interpretations, as permitted by FASB Statement No. 123, “Accounting for Stock-Based Compensation,” (SFAS 123) under which no

compensation expense was recognized for stock option grants and issuances of stock pursuant to the Employees’ Stock Purchase Plan.

However, share-based compensation expense was recognized in periods prior to fiscal 2006 (and continues to be recognized) for stock

issuances pursuant to the Management Incentive Plan and stock grants to non-employee directors. Share-based compensation was a pro

forma disclosure in the financial statement footnotes and continues to be provided for periods prior to fiscal 2006.

Effective July 3, 2005, SYSCO adopted the fair value recognition provisions of FASB Statement No. 123(R), “Share-Based Payment,”

(SFAS 123(R)) using the modified-prospective transition method. Under this transition method, compensation cost recognized in fiscal

2006 and later years includes: a) compensation cost for all share-based payments granted through July 2, 2005, but for which the requisite

service period had not been completed as of the beginning of the fiscal year, based on the grant date fair value estimated in accordance with

the original provisions of SFAS 123, and b) compensation cost for all share-based payments granted during the fiscal year, based on the grant

date fair value estimated in accordance with the provisions of SFAS 123(R). Results for prior periods were not restated.

The adoption of SFAS 123(R) results in lower diluted shares outstanding than would have been calculated had compensation cost not

been recorded for stock options and stock issuances under the Employees’ Stock Purchase Plan. This is due to a modification required by

SFAS 123(R) of the treasury stock method calculation utilized to compute the dilutive effect of stock options.

52