Sysco 2008 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2008 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

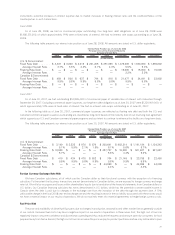

Effective July 3, 2005, we adopted the fair value recognition provisions of SFAS 123(R) using the modified-prospective transition

method. Under this transition method, compensation cost recognized in fiscal 2006 and later years includes: a) compensation cost for all

share-based payments granted through July 2, 2005, but for which the requisite service period had not been completed as of July 2, 2005,

based on the grant date fair value estimated in accordance with the original provisions of SFAS 123, and b) compensation cost for all share-

based payments granted subsequent to July 2, 2005, based on the grant date fair value estimated in accordance with the provisions of

SFAS 123(R). Results for periods prior to fiscal 2006 have not been restated.

As of June 28, 2008, there was $66,432,000 of total unrecognized compensation cost related to share-based compensation

arrangements. That cost is expected to be recognized over a weighted-average period of 2.88 years.

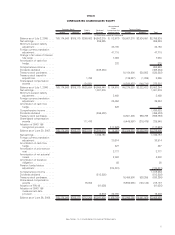

The fair value of each option award is estimated on the date of grant using a Black-Scholes option pricing model. Expected volatility is

based on historical volatility of SYSCO’s stock, implied volatilities from traded options on SYSCO’s stock and other factors. We utilize

historical data to estimate option exercise and employee termination behavior within the valuation model; separate groups of employees

that have similar historical exercise behavior are considered separately for valuation purposes. Expected dividend yield is estimated based on

the historical pattern of dividends and the average stock price for the year preceding the option grant.The risk-free rate for the expected term

of the option is based on the U.S. Treasury yield curve in effect at the time of grant.

The fair value of the stock issued under the Employee Stock Purchase Plan is calculated as the difference between the stock price and

the employee purchase price.The fair value of the stock issued under the Management Incentive Plans is based on the stock price less a 12%

discount for post-vesting restrictions. The discount for post-vesting restrictions is estimated based on restricted stock studies and by

calculating the cost of a hypothetical protective put option over the restriction period.

The compensation cost related to these share-based awards is recognized over the requisite service period.The requisite service period

is generally the period during which an employee is required to provide service in exchange for the award.

The compensation cost related to stock issuances resulting from awards under the Management Incentive Plan was accrued over the

fiscal year to which the incentive bonus relates. The compensation cost related to stock issuances resulting from employee purchases of

stock under the Employees’ Stock Purchase Plan is recognized during the quarter in which the employee payroll withholdings are made.

Certain of our option awards are generally subject to graded vesting over a service period. In those cases, we will recognize

compensation cost on a straight-line basis over the requisite service period for the entire award. In other cases, certain of our option awards

provide for graded vesting over a service period but include a performance-based provision allowing for the vesting to accelerate. In these

cases, if it is probable that the performance condition will be met, we recognize compensation cost on a straight-line basis over the shorter

performance period; otherwise, we recognize compensation cost over the probable longer service period.

In addition, certain of our options provide that if the optionee retires at certain age and years of service thresholds, the options continue

to vest as if the optionee continued to be an employee or director. In these cases, for awards granted prior to July 2, 2005, we will recognize

the compensation cost for such awards over the remaining service period and accelerate any remaining unrecognized compensation cost

when the employee retires. For awards granted subsequent to July 3, 2005, we will recognize compensation cost for such awards over the

period from the date of grant to the date the employee first becomes eligible to retire with his options continuing to vest after retirement.

Our option grants include options that qualify as incentive stock options for income tax purposes. In the period the compensation cost

related to incentive stock options is recorded, a corresponding tax benefit is not recorded as it is assumed that we will not receive a tax

deduction related to such incentive stock options. We may be eligible for tax deductions in subsequent periods to the extent that there is a

disqualifying disposition of the incentive stock option. In such cases, we would record a tax benefit related to the tax deduction in an amount

not to exceed the corresponding cumulative compensation cost recorded in the financial statements on the particular options multiplied by

the statutory tax rate.

New Accounting Standards

SFAS 159

In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Liabilities” (SFAS 159). SFAS 159

permits entities to choose to measure many financial instruments and certain other items at fair value that are not currently required to be

measured at fair value. SFAS 159 also establishes presentation and disclosure requirements designed to facilitate comparisons between

entities that choose different measurement attributes for similar types of assets and liabilities. SFAS 159 is effective as of the beginning of an

entity’s first fiscal year that begins after November 15, 2007. We have decided not to adopt SFAS 159 for our existing financial assets and

liabilities at the date of option. Thus, there will be no one-time impact from adoption of this standard to our consolidated financial

statements.

SFAS 141(R)

In December 2007, the FASB issued SFAS No. 141(R), “Business Combinations” (SFAS 141(R)), which establishes principles and

requirements for how an acquirer recognizes and measures in its financial statements the identifiable assets acquired, the liabilities assumed

and any noncontrolling interest in a business combination. This statement also establishes recognition and measurement principles for the

27