Sysco 2008 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2008 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

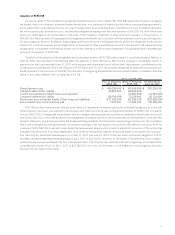

Goodwill is assigned to the reporting units that are expected to benefit from the synergies of the combination. The recoverability of

goodwill and indefinite-lived intangibles is assessed annually, or more frequently as needed when events or changes have occurred that

would suggest an impairment of carrying value, by determining whether the fair values of the applicable reporting units exceed their carrying

values. The reporting units used to assess goodwill impairment are the company’s six operating segments as described in Note 19, Business

Segment Information. The components within each of the six operating segments have similar economic characteristics and therefore are

aggregated into six reporting units. The evaluation of fair value requires the use of projections, estimates and assumptions as to the future

performance of the operations in performing a discounted cash flow analysis, as well as assumptions regarding sales and earnings multiples

that would be applied in comparable acquisitions.

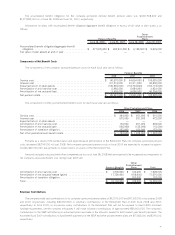

Derivative Financial Instruments

SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities” (SFAS 133), requires the recognition of all derivatives as

assets or liabilities within the consolidated balance sheets at fair value. Gains or losses on derivative financial instruments designated as fair

value hedges have been recognized immediately in the consolidated results of operations, along with the offsetting gain or loss related to the

underlying hedged item.

Gains or losses on derivative financial instruments designated as cash flow hedges have been recorded as a separate component of

shareholders’ equity at their settlement, whereby gains or losses are reclassified to the Consolidated Results of Operations in conjunction

with the recognition of the underlying hedged item.

In the normal course of business, SYSCO enters into forward purchase agreements for the procurement of fuel, electricity and product

commodities related to SYSCO’s business. These agreements meet the definition of a derivative. However, the company elected to use the

normal purchase and sale exemption available under SFAS 133 (as amended and interpreted); therefore, these agreements are not recorded

at fair value.

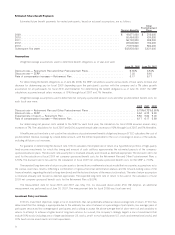

Treasury Stock

The company records treasury stock purchases at cost. Shares removed from treasury are valued at cost using the average cost

method.

Foreign Currency Translation

The assets and liabilities of all foreign subsidiaries are translated at current exchange rates. Related translation adjustments are

recorded as a component of accumulated other comprehensive income (loss).

Revenue Recognition

The company recognizes revenue from the sale of a product when it is considered to be realized or realizable and earned.The company

determines these requirements to be met at the point at which the product is delivered to the customer. The company grants certain

customers sales incentives such as rebates or discounts and treats these as a reduction of sales at the time the sale is recognized. Sales tax

collected from customers is not included in revenue but rather recorded as a liability due to the respective taxing authorities. Purchases and

sales of inventory with the same counterparty that are entered into in contemplation of one another are considered to be a single

nonmonetary transaction. Beginning in the fourth quarter of fiscal 2006, the company recorded the net effect of such transactions in the

consolidated results of operations within sales as a result of a new accounting standard, EITF Issue No. 04-13, “Accounting for Purchases

and Sales of Inventory With the Same Counterparty,” (EITF 04-13). See further discussion in Note 2, Changes in Accounting.

Vendor Consideration

SYSCO recognizes consideration received from vendors when the services performed in connection with the monies received are

completed and when the related product has been sold by SYSCO as a reduction to cost of sales. There are several types of cash

consideration received from vendors. In many instances, the vendor consideration is in the form of a specified amount per case or per pound.

In these instances, SYSCO will recognize the vendor consideration as a reduction of cost of sales when the product is sold. In the situations

where the vendor consideration is not related directly to specific product purchases, SYSCO will recognize these as a reduction of cost of

sales when the earnings process is complete, the related service is performed and the amounts realized. In certain of these latter instances,

the vendor consideration represents a reimbursement of a specific incremental identifiable cost incurred by SYSCO. In these cases, SYSCO

classifies the consideration as a reduction of those costs, with any excess funds classified as a reduction of cost of sales and recognizes these

in the period in which the costs are incurred and related services performed.

Shipping and Handling Costs

Shipping and handling costs include costs associated with the selection of products and delivery to customers. Included in operating

expenses are shipping and handling costs of approximately $2,155,794,000 in fiscal 2008, $1,977,516,000 in fiscal 2007, and

$1,857,093,000 in fiscal 2006.

40