Sysco 2008 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2008 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

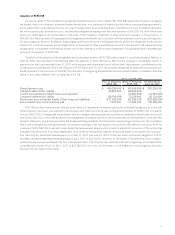

invoiced. Historically, the company has recorded such transactions in the consolidated results of operations within cost of sales for the

purchase amount and within sales for the sales amount. In fiscal 2008 and 2007, the company recorded the net effect of such transactions

in the consolidated results of operations within sales by reducing sales and cost of sales in the amount of $338,907,000 and $334,002,000,

respectively. In the fourth quarter of fiscal 2006, the company recorded the net effect of such transactions in the consolidated results of

operations within sales by reducing sales and cost of sales in the amount of $99,803,000. The amount included in the consolidated results

of operations within cost of sales for the 39 week period ended April 1, 2006 that were recorded on a gross basis prior to the adoption of

EITF 04-13 was $279,746,000.This amount was not restated when the new standard was adopted because only prospective treatment was

allowed.

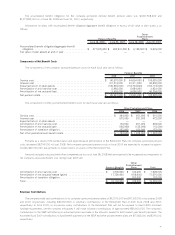

SFAS 123(R) Adoption

In December 2004, the FASB issued SFAS No. 123(R), “Share-Based Payment,” (SFAS 123(R)), which is a revision of SFAS No. 123,

“Accounting for Stock-Based Compensation” (SFAS 123). SFAS 123(R) supersedes APB Opinion No. 25, “Accounting for Stock Issued to

Employees” (APB Opinion 25), and amends SFAS No. 95, “Statement of Cash Flows.” In fiscal 2006, SYSCO adopted the provisions of

SFAS 123(R) utilizing the modified-prospective transition method under which prior period results have not been restated. See discussion of

the impact of adoption in Note 15, Share-Based Compensation.

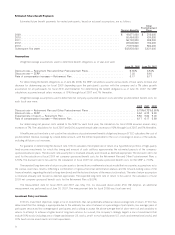

3. NEW ACCOUNTING STANDARDS

SFAS 159

In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Liabilities” (SFAS 159). SFAS 159

permits entities to choose to measure many financial instruments and certain other items at fair value that are not currently required to be

measured at fair value. SFAS 159 also establishes presentation and disclosure requirements designed to facilitate comparisons between

entities that choose different measurement attributes for similar types of assets and liabilities. SFAS 159 is effective as of the beginning of an

entity’s first fiscal year that begins after November 15, 2007.The company decided not to adopt SFAS 159 for its existing financial assets and

liabilities at the date of option.Thus, there will be no one-time impact from adoption of this standard to its consolidated financial statements.

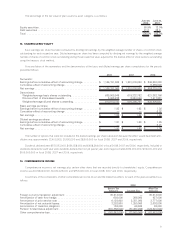

SFAS 141(R)

In December 2007, the FASB issued SFAS No. 141(R), “Business Combinations” (SFAS 141(R)), which establishes principles and

requirements for how an acquirer recognizes and measures in its financial statements the identifiable assets acquired, the liabilities assumed

and any noncontrolling interest in a business combination. This statement also establishes recognition and measurement principles for the

goodwill acquired in a business combination and disclosure requirements to enable financial statement users to evaluate the nature and

financial effects of the business combination. SYSCO will apply this statement primarily on a prospective basis for business combinations

beginning in fiscal 2010. Earlier application of the standard is prohibited.

FSP 157-2

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements” (SFAS 157), which establishes a common definition for

fair value under generally accepted accounting principles, establishes a framework for measuring fair value and expands disclosure

requirements about such fair value measurements. In February 2008, the FASB issued FASB Staff Position 157-2, “Effective Date of FASB

Statement No. 157” (FSP 157-2), which partially defers the effective date of SFAS No. 157 for one year for non-financial assets and liabilities

that are recognized or disclosed at fair value in the financial statements on a non-recurring basis. Consequently, SFAS 157 will be effective for

SYSCO in fiscal 2009 for financial assets and liabilities carried at fair value and non-financial assets and liabilities that are recognized or

disclosed at fair value on a recurring basis. As a result of the deferral, SFAS 157 will be effective in fiscal 2010 for non-recurring, non-financial

assets and liabilities that are recognized or disclosed at fair value. The adoption of SFAS 157 in fiscal 2009 for financial assets and liabilities

carried at fair value and non-financial assets and liabilities that are recognized or disclosed at fair value on a recurring basis will not have a

material impact on the company’s consolidated financial statements. The company is continuing to evaluate the impact of adopting the

provisions of SFAS 157 in fiscal 2010 for non-recurring, non-financial assets and liabilities that are recognized or disclosed at fair value.

SFAS 161

In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging Activities, an amendment of

FASB Statement No. 133” (SFAS 161). SFAS 161 requires enhanced disclosures about an entity’s derivative and hedging activities and thereby

improves the transparency of financial reporting. This Statement will be effective for SYSCO’s financial statements beginning with the third

quarter of fiscal 2009. The company is currently evaluating the impact the adoption of SFAS 161 may have on its financial statement

disclosures.

42