Sysco 2008 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2008 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

additional funding will be required as well as the payment of excise tax. As a result, we recorded a liability of approximately $16,500,000

related to our share of the minimum funding requirements and related excise tax for these periods. Currently, we believe that a majority of

this amount will be paid in fiscal 2009 and are continuing to explore our alternatives as it relates to this plan. As of June 28, 2008, we have

approximately $22,000,000 in liabilities recorded in total related to certain underfunded multi-employer defined benefit plans.

BSCC Cooperative Structure

Our affiliate, BSCC, is a cooperative taxed under subchapter T of the United States Internal Revenue Code.We believe that the deferred

tax liabilities resulting from the business operations and legal ownership of BSCC are appropriate under the tax laws. However, if the

application of the tax laws to the cooperative structure of BSCC were to be successfully challenged by any federal, state or local tax authority,

we could be required to accelerate the payment of all or a portion of our income tax liabilities associated with BSCC that we otherwise have

deferred until future periods. In that event, we would be liable for interest on such amounts. As of June 28, 2008, SYSCO has recorded

deferred income tax liabilities of $1,054,190,000, net of federal benefit, related to the BSCC supply chain distributions. If the IRS and any

other relevant taxing authorities determine that all amounts since the inception of BSCC were inappropriately deferred, and the

determination is upheld, we estimate that in addition to making a current payment for amounts previously deferred, as discussed above,

we may be required to pay interest on the cumulative deferred balances. These interest amounts could range from $290,000,000 to

$320,000,000, prior to federal and state income tax benefit, as of June 28, 2008. SYSCO calculated this amount based upon the amounts

deferred since the inception of BSCC applying the applicable jurisdictions’ interest rates in effect in each period.The IRS, in connection with

its audit of our 2003 and 2004 federal income tax returns, proposed adjustments related to the taxability of the cooperative structure. We

are vigorously protesting these adjustments. We have reviewed the merits of the issues raised by the IRS, and while management believes it

is probable we will prevail, we concluded the measurement model of FIN 48 required us to provide an accrual for a portion of the interest

exposure. If a taxing authority requires us to accelerate the payment of these deferred tax liabilities and to pay related interest, if any, we may

be required to raise additional capital through debt financing or we may have to forego share repurchases or defer planned capital

expenditures or a combination of these items.

Off-Balance Sheet Arrangements

We have no off-balance sheet arrangements.

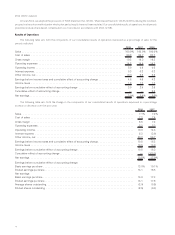

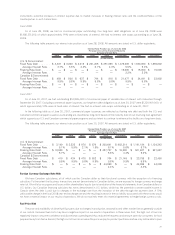

Contractual Obligations

The following table sets forth, as of June 28, 2008, certain information concerning our obligations and commitments to make

contractual future payments:

Total

Less Than

1 Year 1-3 Years 3-5 Years

More Than

5 Years

Payments Due by Period

(In thousands)

Recorded Contractual Obligations:

Long-term debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 1,943,711 $ 262 $ 447 $ 450,135 $ 1,492,867

Capital lease obligations . . . . . . . . . . . . . . . . . . . . . . . . . 36,620 4,634 6,380 3,687 21,919

Deferred compensation

(1)

. . . . . . . . . . . . . . . . . . . . . . . . 128,752 8,885 17,455 14,067 88,345

SERP and other postretirement plans

(2)

. . . . . . . . . . . . . . 243,464 17,401 39,899 45,406 140,758

Multi-employer pension plans

(3)

. . . . . . . . . . . . . . . . . . . 22,000 16,200 5,800 — —

Unrecognized tax benefits (including interest)

(4)

. . . . . . . . 208,037

Unrecorded Contractual Obligations:

Interest payments related to debt

(5)

. . . . . . . . . . . . . . . . 1,453,853 103,233 206,465 190,185 953,970

Long-term non-capitalized leases . . . . . . . . . . . . . . . . . . 290,843 64,000 97,916 54,356 74,571

Purchase obligations

(6)

. . . . . . . . . . . . . . . . . . . . . . . . . . 2,560,268 1,852,621 540,937 107,462 59,248

Total contractual cash obligations . . . . . . . . . . . . . . . . . . $ 6,887,548 $ 2,067,236 $ 915,299 $ 865,298 $ 2,831,678

(1)

The estimate of the timing of future payments under the Executive Deferred Compensation Plan involves the use of certain

assumptions, including retirement ages and payout periods.

(2)

Includes estimated contributions to the unfunded Supplemental Executive Retirement Plan (SERP) and other postretirement benefit

plans made in amounts needed to fund benefit payments for vested participants in these plans through fiscal 2017, based on actuarial

assumptions.

(3)

Excludes normal contributions required under our collective bargaining agreements.

(4)

Unrecognized tax benefits relate to uncertain tax positions recorded under FIN 48, which we adopted as of July 1, 2007. As of June 28,

2008, we had a liability of $69,830,000 for unrecognized tax benefits for all tax jurisdictions and $138,207,000 for related interest that

could result in cash payment. As we are not able to reasonably estimate the timing of non-current payments or the amount by which the

liability will increase or decrease over time, the related non-current balances have not been reflected in the “Payments Due by Period”

section of the table. For further discussion of the impact of adopting FIN 48, see Note 16, Income Taxes, in the Notes to Consolidated

Financial Statements in Item 8.

23