Yahoo 2005 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2005 Yahoo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

94

Note 14 LITIGATION SETTLEMENT

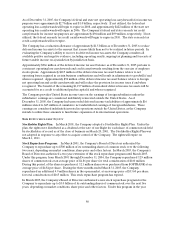

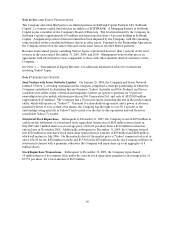

In April 2002, the Company’s wholly owned subsidiary, Overture, filed a lawsuit against Google Inc.

(“Google”) in the United States District Court for the Northern District of California with respect to a

patent which protected various features and innovations relating to bid-for-performance products and

Overture’s pay-for-performance (sponsored) search technologies. In addition, the Company had a second

dispute with Google concerning the shares issuable to the Company pursuant to a warrant held by the

Company to purchase Google shares that were received in connection with a June 2000 services

agreement.

In August 2004, Google issued 2.7 million shares of Class A common stock in settlement of the two

disputes. The Company agreed to dismiss the 361 patent lawsuits and granted to Google a fully-paid

license to the 361 patent as well as several related patent applications held by Overture. The Company

allocated the 2.7 million shares between the two disputes, based on the relative fair values of the two

disputes, including consideration of a valuation performed by a third party. A portion of the shares

allocated to the patent dispute has been recorded as an adjustment to goodwill for the period that the

patents were in effect prior to Overture’s acquisition by the Company. The portion of the shares received

for the settlement of the patent dispute which has been allocated to future periods has been recorded in

deferred revenue on the consolidated balance sheets and will be recognized as fees revenues over the

remaining life of the patent, approximately 12 years. The shares allocated to the warrant dispute

settlement did not have an income statement effect as the fair value of the warrant was recorded at the

time the services were performed based on the fair value of the services rendered.

During the year ended December 31, 2004, the Company disposed of approximately 4.0 million shares of

Google and realized gains of $413 million, net of selling costs, which were included in other income, net on

the consolidated statements of operations. During the year ended December 31, 2005 the Company sold

the remaining Google shares and realized gains of $961 million, which were recorded in other income, net.

Note 15 SEGMENTS

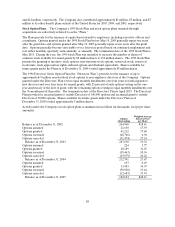

The Company manages its business geographically. The primary areas of measurement and

decision-making are the United States and International. Management relies on an internal management

reporting process that provides revenue and segment operating income before depreciation and

amortization for making financial decisions and allocating resources. Segment operating income before

depreciation and amortization includes income from operations before depreciation, amortization of

intangible assets and amortization of stock compensation expense. Management believes that segment

operating income before depreciation and amortization is an appropriate measure for evaluating the

operational performance of the Company’s segments. However, this measure should be considered in

addition to, not as a substitute for, or superior to, income from operations or other measures of financial

performance prepared in accordance with generally accepted accounting principles.