Cabela's 2005 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

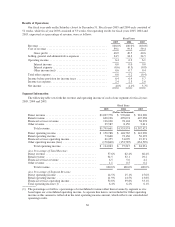

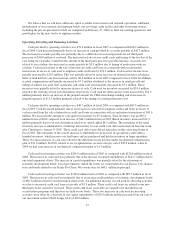

For credit card loans securitized and sold, the loans are removed from our balance sheet and the net earnings

on these securitized assets after paying outside investors are reflected as a component of our securitization

income on a GAAP basis. The following table summarizes the results of our Financial Services segment for

fiscal years 2005, 2004 and 2003 on a GAAP basis with interest and fee income, interest expense and provision

for loan losses for the credit card loans receivable we own reported in net interest income. Non-interest income

on a GAAP basis includes servicing income, gains on sales of loans and income recognized on our retained

interests for the entire securitized portfolio, as well as, interchange income on the entire managed portfolio.

Financial Services Revenue as reported in the Financial Statements:

Fiscal Years

2005 2004 2003

(Dollars in thousands)

Interest and fee income ............................................ $ 17,196 $ 12,735 $ 7,858

Interest expense .................................................. (3,241) (3,063) (3,226)

Net interest income ............................................... 13,955 9,672 4,632

Non-interest income:

Securitization income (1) ...................................... 133,032 96,466 74,472

Other non-interest income ..................................... 31,836 24,905 19,050

Total non-interest income .................................. 164,868 121,371 93,522

Less: Customer rewards costs ....................................... (62,723) (52,939) (39,876)

Financial Services revenue ......................................... $116,100 $ 78,104 $ 58,278

(1) For the fiscal years ended 2005, 2004 and 2003, we recognized gains on sale of credit card loans of $17.0

million, $8.9 million and $5.9 million, respectively, which are reflected as a component of securitization

income.

Our “managed” credit card loans represent credit card loans receivable we own plus securitized credit card

loans. Since the financial performance of the managed portfolio has a significant impact on the earnings we will

receive from servicing the portfolio, we believe the following table on a “managed” basis is important

information to analyze our revenue in the Financial Services segment. This non-GAAP presentation reflects the

financial performance of the credit card loans receivable we own plus those that have been sold for the fiscal

years ended 2005, 2004 and 2003 and includes the effect of recording the retained interest at fair value. Interest

income, interchange income (net of customer rewards) and fee income on both the owned and securitized

portfolio are recorded in their respective line items. Interest paid to outside investors on the securitized credit

card loans is included with other interest costs and included in interest expense. Credit losses on the entire

managed portfolio are included in provision for loan losses. Although our financial statements are not presented

in this manner, management reviews the performance of its managed portfolio in order to evaluate the

effectiveness of its origination and collection activities, which ultimately affects the income we will receive for

servicing the portfolio. The securitization of credit card loans primarily converts interest income, interchange

income, credit card fees, credit losses and other income and expense related to the securitized loans into

securitization income.

37