Cabela's 2005 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(Dollar Amounts in Thousands Except Share and Per Share Amounts)

should follow the disclosure requirements of Statement 5 for both loss and gain contingencies related to uncertain

tax positions. The transition adjustment resulting from the application of this interpretation would be recorded as

a cumulative-effect change in the income statement as of the end of the period of adoption. The FASB met in

January of 2006 and continues to deliberate over the issues in this interpretation, it has also determined that the

final interpretation would not be effective until the first fiscal year ending after December 15, 2006.

In August 2005, the FASB issued proposed statements of financial accounting standards: “Accounting for

Transfers of Financial Assets, an amendment of FASB Statement No. 140” and “Accounting for Servicing of

Financial Assets, an amendment of FASB Statement No. 140.” The Company is currently reviewing the

amendments to FASB Statement No. 140 and has not yet determined the impact on its financial statements.

In February 2006, the FASB issued Statement No. 155, “Accounting for Certain Hybrid Financial

Instruments—an amendment to FASB Statements No. 133 and 140” (“Statement 155”). Statement 155 eliminates

the exemption from applying Statement 133 to interests in securitized financial assets so that similar instruments

are accounted for similarly regardless of the form of the instruments. It also allows the Company to elect fair

value measurement at acquisition, at issuance, or when a previously recognized financial instrument is subject to

a remeasurement (new basis) event, on an instrument-by-instrument basis, in cases in which a derivative would

otherwise have to be bifurcated. This statement is effective for all financial instruments acquired or issued after

the beginning of an entity’s first fiscal year that begins after September 15, 2006. Provisions of Statement 155

may be applied to instruments that the Company holds at the date of adoption on an instrument-by-instrument

basis. The Company is currently reviewing Statement 155 and has not yet determined the impact on its financial

statements.

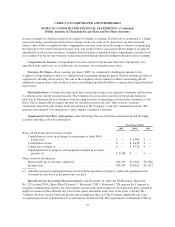

2. SALE OF CREDIT CARD LOANS

WFB has established a trust for the purpose of routinely selling and securitizing credit card loans. WFB

maintains responsibility for servicing the securitized loans and receives 1.25% (annualized) for Series 2001-2,

2003-1 and 2003-2 and 2.0% (annualized) for Series 2004-I, 2004-II and 2005-I of the average outstanding loans

in the trust. Additionally, WFB earns 0.75% on Series 2001-2, 2003-1 and 2003-2, but only to the extent that the

trust generates sufficient interchange income to make that portion of the payment. Servicing fees are paid

monthly. The trust issues commercial paper, long term bonds or long term notes. Variable bonds and notes are

priced on a floating rate basis with a spread over a benchmark rate. The fixed rate notes are priced on a five-year

swap rate plus a spread. WFB retains rights to future cash flows arising after investors have received the return

for which they are entitled and after certain administrative costs of operating the trust. These retained interests

are known as interest-only strips and are subordinate to investor’s interests. The value of the interest-only strips

is subject to credit, payment rate and interest rate risks on the loans sold. The investors have no recourse to

WFB’s assets for failure of debtors to pay. However, as contractually required, WFB establishes certain cash

accounts, known as cash reserve accounts, to be used as collateral for the benefit of investors.

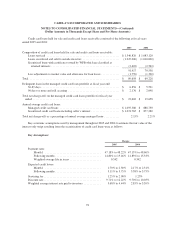

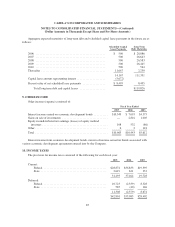

Retained Interests:

Retained interests in securitized loans consisted of the following at fiscal years ended 2005 and 2004:

2005 2004

Cash reserve account ....................................... $16,495 $16,158

Interest-only strip ......................................... 15,567 10,003

Class B certificates ........................................ 2,403 2,562

$34,465 $28,723

77