Cabela's 2005 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

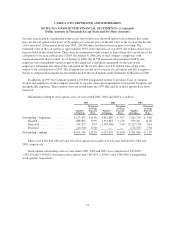

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(Dollar Amounts in Thousands Except Share and Per Share Amounts)

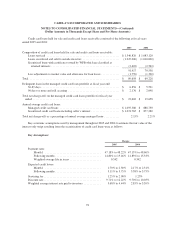

no principal amounts outstanding on the line of credit, and $43,141 outstanding on letters of credit and standby

letters of credit, at December 31, 2005. The average principal amount outstanding during fiscal 2005 was

$77,204. The weighted average interest rate on the line of credit was 4.56% during fiscal 2005. The agreement

requires that the Company comply with several financial and other covenants, including requirements that it

maintain the following financial ratios as set forth in the credit agreement:

• A fixed charge coverage ratio of no less than 1.50 to 1.00 as of the last day of any fiscal quarter. The

fixed charge coverage ratio is defined as (a) EBITR minus the sum of any cash dividends, tax expenses

paid in cash, in each case for the twelve month period ending on the last day of the fiscal quarter, and to

the extent not included, or previously included, in the calculation of EBITR, any cash payments with

respect to contingent obligations to (b) the sum of interest expense, all required principal payments with

respect to coverage indebtedness and operating lease obligations, in each case for the twelve month

period ending on the last day of the fiscal quarter. The credit agreement defines EBITR as net income

before deductions for income taxes, interest expense and operating lease obligations.

• A cash flow leverage ratio of no more than 3.00 to 1.00 as of the last day of any fiscal quarter for the

twelve month period ending on that day. The cash flow leverage ratio is defined as adjusted coverage

indebtedness (average indebtedness of the Company on a consolidated basis for the preceding four fiscal

quarters determined in accordance with GAAP excluding: (a) liabilities of WFB, (b) long term deferred

compensation, (c) long term deferred taxes, (d) any current liabilities (other than coverage

indebtedness), and (e) deferred grant income) to EBITDA. The credit agreement defines EBITDA as net

income before deductions for income taxes, interest expense, depreciation and amortization, all as

determined on a consolidated basis in accordance with GAAP.

• A minimum tangible net worth of no less than $350,000 plus 50% of positive consolidated net income

on a cumulative basis for each fiscal year beginning with the fiscal year ended 2005 as of the last day of

any fiscal quarter. Tangible net worth is equity less intangible assets.

In addition, the credit agreement contains cross default provisions to other outstanding debt. In the event the

Company fails to comply with these covenants, a default is triggered. In the event of default, all outstanding

letters of credit and all principal and outstanding interest would immediately become due and payable.

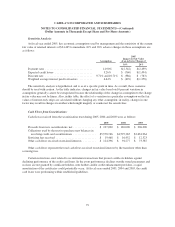

The Company is party to inventory financing agreements that allow certain vendors providing boat

merchandise to give the Company extended payment terms. The vendors are responsible for all interest payments

for the financing period and the financing company holds a security interest in the specific boat inventory held by

the Company. The Company’s revolving credit facility limits this security interest to $25,000. The Company

records this boat merchandise in inventory with an offsetting liability in accounts payable. The loans and payments

are reflected in the financing lines of credit in the Company’s cash flow statement. The extended payment terms to

the vendor do not exceed one year. The outstanding liability was $1,443 at the end of fiscal 2005.

The Company was in compliance with all covenants as of the end of the periods presented.

On October 7, 2004, WFB entered into an unsecured Federal Funds Sales Agreement with a financial

institution. All federal funds transactions are on a daily origination and return basis. Daily interest charges are

determined based on mutual agreement by the parties. The maximum amount of funds which can be borrowed is

$25,000. There were no amounts outstanding as of December 31, 2005.

On October 8, 2004, WFB entered into an unsecured Federal Funds Line of Credit agreement with a financial

institution. The maximum amount of funds which can be borrowed is $40,000. The interest rate for the line of credit

is based on the current federal funds rate. There were no amounts outstanding as of December 31, 2005.

83