Cabela's 2005 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

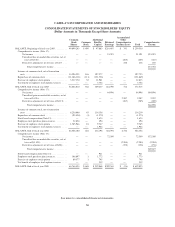

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(Dollar Amounts in Thousands Except Share and Per Share Amounts)

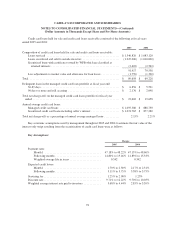

WFB is required to maintain a cash reserve account as part of certain securitization programs. In addition,

WFB owns Class B certificates from one of its securitizations. The fair value of the cash reserve account is

estimated by discounting future cash flows using a rate that reflects the risks commensurate with similar types of

instruments. For the Class B certificates, the fair value approximates the book value of the underlying loans.

Interest-only strips are measured like investments in debt securities classified as trading under SFAS No. 115,

Accounting for Certain Investments in Debt and Equity Securities.

Inventories—Inventories are stated at the lower of cost or market. Cost is determined using the last-in,

first-out method (dollar value, link-chain) for all inventories except for those inventories owned by Van Dyke

Supply Company, Inc., and Wild Wings, LLC, subsidiaries of the Company, which use the first-in, first-out

method. If all inventories had been valued using the first-in, first-out method, which approximates replacement

cost, the stated value would not have been greater as of the fiscal years ended 2005 and 2004, respectively. All

inventories are in one inventory class and are classified as finished goods. A provision for shrink is estimated,

based on historical cycle count adjustments and periodic physical inventories. The balance in the shrink reserve

was $2,350 and $4,511 as of December 31, 2005 and January 1, 2005, respectively. The change in the

Company’s shrink reserve is a function of the timing of physical inventory counts. The allowance for damaged

goods from returns is based upon historical experience. Inventory is adjusted for obsolete or slow moving

inventory based on inventory aging reports and, in some cases, by specific identification of slow moving or

obsolete inventory. The balance in the obsolete and damaged goods reserve was $7,904 and $7,129 as of

December 31, 2005 and January 1, 2005, respectively.

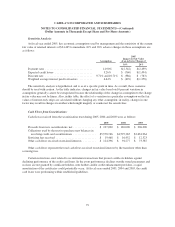

Accounting for Vendor Allowances—Vendor allowances include allowances, rebates and cooperative

advertising funds received from vendors. These funds are determined for each fiscal year and the majority is

based on various quantitative contract terms. Amounts expected to be received from vendors relating to purchase

of merchandise inventories are recognized as a reduction of costs of goods sold as the merchandise is sold.

Amounts that represent a reimbursement of costs incurred, such as advertising, are recorded as a reduction to the

related expense in the period that the related expense is incurred. Fair value of expenses reimbursed is

determined using actual costs incurred, such as print and production costs for media or catalog advertising.

Reimbursements received from vendors that exceed related expenses are classified as a reduction of merchandise

costs of goods sold when the merchandise is sold.

The Company records an estimate of earned allowances based on the latest projected purchase volumes.

Historical program results, current purchase volumes, and inventory projections are reviewed when establishing

the estimate for earned allowances, and a reserve based on historical adjustments is recorded as a reduction to the

total estimated allowance.

Deferred Catalog Costs and Advertising—The Company expenses the production cost of advertising as the

advertising takes place, except for catalog advertising costs, which are capitalized and amortized over the

expected period of future benefits.

Advertising consists primarily of catalogs for the Company’s products. The capitalized costs of the

advertising are amortized over a three to twelve month period following the mailing of the catalogs.

At fiscal year ends 2005 and 2004, $36,987 and $26,592, respectively, of catalog costs were included in

prepaid expenses in the accompanying consolidated balance sheets. Advertising expense was $170,024, $157,623

and $146,062 for the fiscal years ended 2005, 2004 and 2003, respectively. Advertising vendor allowances

recorded as a reduction to advertising expense included in the amounts above were approximately $4,783, $3,290

and $4,044 for the fiscal years ended 2005, 2004 and 2003, respectively.

70