Cabela's 2005 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

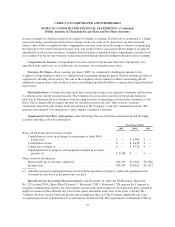

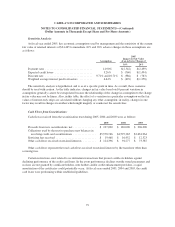

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(Dollar Amounts in Thousands Except Share and Per Share Amounts)

Credit card loans held for sale and credit card loans receivable consisted of the following at fiscal years

ended 2005 and 2004:

2005 2004

Composition of credit card loans held for sale and credit card loans receivable:

Loans serviced ................................................... $1,340,820 $ 1,083,120

Loans securitized and sold to outside investors .......................... (1,247,000) (1,010,000)

Securitized loans with certificates owned by WFB which are classified as

retained interests ................................................ (2,403) (2,562)

91,417 70,558

Less adjustments to market value and allowance for loan losses ............. (1,759) (1,330)

Total ............................................................... $ 89,658 $ 69,228

Delinquent loans in the managed credit card loan portfolio at fiscal year end:

30-89 days ....................................................... $ 6,856 $ 5,591

90 days or more and still accruing .................................... $ 2,176 $ 2,098

Total net charge-offs on the managed credit card loans portfolio for fiscal year

ended ............................................................. $ 23,602 $ 19,658

Annual average credit card loans:

Managed credit card loans .......................................... $1,095,580 $ 888,730

Securitized credit card loans including seller’s interest .................... $1,074,765 $ 877,280

Total net charge-offs as a percentage of annual average managed loans ........... 2.15% 2.21%

Key economic assumptions used by management throughout 2005 and 2004 to estimate the fair value of the

interest only strips resulting from the securitization of credit card loans were as follows:

Key Assumptions:

Ranges

2005 2004

Payment rates:

Month 1 ....................................... 47.18% to 48.22% 47.15% to 48.60%

Following months ................................ 14.80% to 15.46% 14.83% to 15.33%

Weighted average life in years ...................... 0.542 0.542

Expected credit losses:

Month 1 ....................................... 1.70% to 2.30% 2.17% to 2.31%

Following months ................................ 3.11% to 3.75% 3.58% to 3.75%

Servicing fee ........................................ 1.25% to 2.00% 1.25%

Discount rate ........................................ 9.71% to 12.22% 9.70% to 10.03%

Weighted average interest rate paid to investors ............ 3.68% to 4.44% 2.83% to 3.39%

78