Cabela's 2005 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

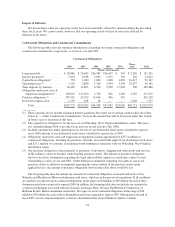

December 31, 2005. Our total remaining borrowing capacity under the credit facility as of December 31, 2005,

after subtracting outstanding letters of credit of $36.7 million, and standby letters of credit of $6.4 million, was

$281.9 million. The credit agreement requires that we comply with several financial and other covenants,

including requirements that we maintain the following financial ratios as set forth in the credit agreement:

• A fixed charge coverage ratio of no less than 1.50 to 1.00 as of the last day of any fiscal quarter. The

fixed charge coverage ratio is defined as (a) EBITR minus the sum of any cash dividends, tax expenses

paid in cash, in each case for the twelve month period ending on the last day of the fiscal quarter, and to

the extent not included, or previously included, in the calculation of EBITR, any cash payments with

respect to contingent obligations, to (b) the sum of interest expense, all required principal payments with

respect to coverage indebtedness and operating lease obligations, in each case for the twelve month

period ending on the last day of the fiscal quarter. Our credit agreement defines EBITR as net income

before deductions for income taxes, interest expense and operating lease obligations.

• A cash flow leverage ratio of no more than 3.00 to 1.00 as of the last day of any fiscal quarter for the

twelve month period ending on that day. The cash flow leverage ratio is defined as adjusted coverage

indebtedness (average indebtedness of the Company on a consolidated basis for the preceding four fiscal

quarters determined in accordance with GAAP excluding: (a) liabilities of WFB, (b) long term deferred

compensation, (c) long term deferred taxes, (d) any current liabilities (other than coverage

indebtedness), and (e) deferred grant income) to EBITDA. Our credit agreement defines EBITDA as net

income before deductions for income taxes, interest expense, depreciation and amortization, all as

determined on a consolidated basis in accordance with GAAP.

• A minimum tangible net worth of no less than $350,000 plus 50% of positive consolidated net income

on a cumulative basis for each fiscal year beginning with the fiscal year ended 2005 as of the last day of

any fiscal quarter. Tangible net worth is equity less intangible assets.

In addition, the credit agreement contains cross default provisions to other outstanding debt. In the event we

fail to comply with these covenants, a default is triggered. In the event of default, all outstanding letters of credit

and all principal and outstanding interest would immediately become due and payable.

In addition, our new credit agreement includes a limitation that we may not pay dividends to our

stockholders in excess of 50% of our prior year’s consolidated EBITDA and a provision that permits acceleration

by the lenders in the event there is a “change in control.” Our credit agreement defines “EBITDA” to mean our

net income before deductions for income taxes, interest expense, depreciation and amortization. Based upon this

EBITDA calculation for fiscal 2005, dividends would not be permissible in fiscal 2006 in excess of $80.3

million. Our credit agreement defines a “change in control” to mean any of the following circumstances: (a) we

cease to own, directly or indirectly, 100% of the shares of each class of the voting stock or other equity interest

of each other borrower that has or has had total assets in excess of $10.0 million; (b) the acquisition or

ownership, directly or indirectly, beneficially or of record, by any person or group (within the meaning of the

Securities Exchange Act of 1934 and the rules of the Securities and Exchange Commission thereunder as in

effect on July 15, 2005), of equity interests representing more than 25% of the aggregate ordinary voting power

represented by our issued and outstanding equity interests (other than equity interests held by Richard N. Cabela

or James W. Cabela or a group controlled by Richard N. Cabela or James W. Cabela); or (c) occupation of a

majority of the seats (other than vacant seats) on our board of directors by persons who were neither

(i) nominated by our board of directors nor (ii) appointed by directors so nominated. Our credit agreement

provides that all loans or deposits from us or any of our subsidiaries to our bank cannot exceed $75.0 million in

the aggregate at any time when loans are outstanding under the revolving credit facility.

We are party to inventory financing agreements that allow certain vendors providing boat merchandise to

give us extended payment terms. The vendors are responsible for all interest payments for the financing period

and the financing company holds a security interest in the specific boat inventory we hold. Our revolving credit

facility limits this security interest to $25.0 million. We record this boat merchandise in inventory with an

offsetting liability in accounts payable. The loans and payments are reflected in the financing section of our cash

52