Cabela's 2005 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(Dollar Amounts in Thousands Except Share and Per Share Amounts)

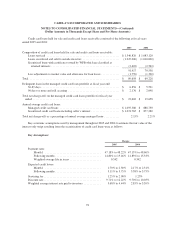

11. DERIVATIVES

The Company is exposed to market risks including changes in currency exchange rates and interest rates.

The Company may enter into various derivative transactions pursuant to established Company policies to manage

volatility associated with these exposures.

Foreign Currency Management—The Company may enter into forward exchange or option contracts for

transactions denominated in a currency other than the applicable functional currency in order to reduce exposures

related to changes in foreign currency exchange rates. This primarily relates to hedging against anticipated

inventory purchases.

Hedges of anticipated inventory purchases are designated as cash flow hedges. The gains and losses

associated with these hedges are deferred in accumulated other comprehensive income/(loss) until the anticipated

transaction is consummated and are recognized in the income statement in the same period during which the

hedged transactions affect earnings. Gains and losses on foreign currency derivatives for which the Company has

not elected hedge accounting are recorded immediately in earnings.

For the fiscal years ended 2005 and 2004, there was ineffectiveness associated with the Company’s foreign

currency derivatives designated as cash flow hedges. The Company discontinued four foreign currency contracts

in the twelve months ended December 31, 2005, for which a loss of $58 was recorded in earnings.

Generally, the Company hedges a portion of its anticipated inventory purchases for periods up to twelve

months. As of December 31, 2005, the Company has hedged certain portions of its anticipated inventory

purchases through May 2006.

The fair value of foreign currency derivative assets or liabilities is recognized within other current assets or

other current liabilities. As of December 31, 2005 and January 1, 2005, the fair value of foreign currency

derivative assets were $0 and $235, respectively, and the fair value of foreign currency derivative liabilities was

$11 and $0, respectively.

As of December 31, 2005 and January 1, 2005, the net deferred loss recognized in accumulated other

comprehensive income/(loss) was $(158) and $(205), net of tax, respectively. The Company anticipates a loss of

$7, net of tax, will be transferred out of accumulated other comprehensive income and recognized within

earnings over the next twelve months. Gains or (losses) of $(102), $296 and $430, net of tax, were transferred

from accumulated other comprehensive income into income from operations in fiscal years 2005, 2004 and 2003,

respectively.

Interest Rate Management—On February 4, 2003, in connection with the Series 2003-1 term securitization,

the securitization trust entered into a $300,000 notional swap agreement in order to manage interest rate

exposure. The exposure is related to changes in cash flows from funding credit card loans, which include a high

percentage of accounts with floating rate obligations that do not incur monthly finance charges. The swap

converts the interest rate on the investor bonds from a floating rate basis with a spread over a benchmark note to

a fixed rate of 3.699%. Since the trust is not consolidated, the fair value of the swap is not reflected on the

financial statements. Additionally, the Company entered into a swap with similar terms with the counter-party

whereby the notional amount is zero unless the notional amount of the trust’s swap falls below $300,000. The

Company has not elected to designate this derivative as a hedge and, therefore, the derivative is marked to market

through the statement of income. As of December 31, 2005, market value was determined to be zero. WFB pays

Cabela’s a fee for the credit enhancement provided by this swap, which was $608, $610 and $552 in fiscal 2005,

2004 and 2003, respectively.

87