Cabela's 2005 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

We sell our credit card loans in the ordinary course of business through a commercial paper conduit

program and we have from time to time entered into longer term fixed and floating rate securitization

transactions. In a conduit securitization, our credit card loans are converted into securities and sold to commercial

paper issuers, which pool the securities with those of other issuers. The amount securitized in a conduit structure

is allowed to fluctuate within the terms of the facility, which may provide greater flexibility for liquidity needs.

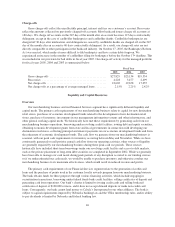

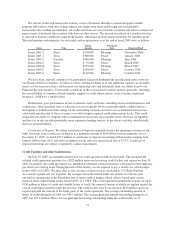

The total amounts and maturities for our credit card securitizations as of the end of fiscal 2005 were as follows:

Series Type

Initial

Amount

Certificate

Rate Expected Final

Series 2001-2 Term $250,000 Floating November 2006

Series 2003-1 Term $300,000 Fixed January 2008

Series 2003-2 Variable $300,000 Floating June 2006

Series 2004-I Term $ 75,000 Fixed March 2009

Series 2004-II Term $175,000 Floating March 2009

Series 2005-I Term $140,000 Fixed October 2010

Series 2005-I Term $110,000 Floating October 2010

We have been, and will continue to be, particularly reliant on funding from securitization transactions for

our Financial Services business. A failure to renew existing facilities or to add additional capacity on favorable

terms as it becomes necessary could increase our financing costs and potentially limit our ability to grow our

Financial Services business. Unfavorable conditions in the asset-backed securities markets generally, including

the unavailability of commercial bank liquidity support or credit enhancements, such as financial guaranty

insurance, could have a similar effect.

Furthermore, poor performance of our securitized credit card loans, including increased delinquencies and

credit losses, lower payment rates or a decrease in excess spreads below certain thresholds, could result in a

downgrade or withdrawal of the ratings on the outstanding securities issued in our securitization transactions,

cause early amortization of these securities or result in higher required credit enhancement levels. This could

jeopardize our ability to complete other securitization transactions on acceptable terms, decrease our liquidity

and force us to rely on other potentially more expensive funding sources, to the extent available, which would

decrease our profitability.

Certificates of Deposit. We utilize certificates of deposit to partially finance the operating activities of our

bank. Our bank issues certificates of deposit in a minimum amount of $100,000 in various maturities. As of

December 31, 2005, we had $109.5 million of certificates of deposit outstanding with maturities ranging from

January 2006 to June 2015 and with a weighted average effective annual fixed rate of 4.13%. Certificate of

deposit borrowings are subject to regulatory capital requirements.

Credit Facilities and other Indebtedness

On July 15, 2005, we amended and restated our credit agreement with several banks. The amended and

restated credit agreement provides for a $325 million unsecured revolving credit facility and expires on June 30,

2010. In addition, the credit agreement was amended to eliminate certain limitations with regard to the temporary

pay down of revolving loans. During the term of the facility, we are required to pay a facility fee, which ranges

from 0.100% to 0.250%. We may elect to take advances at interest rates calculated at U.S. Bank National

Association’s prime rate (or, if greater, the average rate on the federal funds rate in effect for the day plus

one-half of one percent) or the Eurodollar rate of interest plus a margin, which adjusts, based upon certain

financial ratios achieved and ranges from 0.650% to 1.350%. The credit agreement permits the issuance of up to

$150 million in letters of credit and standby letters of credit, the nominal amount of which are applied against the

overall credit limit available under the revolver. The credit facility may be increased to $450 million upon our

request and with the consent of the banks party to the credit agreement. The average outstanding amount of

letters of credit during fiscal 2005 was $44.7 million. The average principal amount outstanding during fiscal

2005 was $77.2 million. There were no principal borrowings outstanding under the credit facility as of

51