Cabela's 2005 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

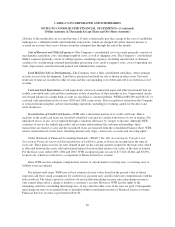

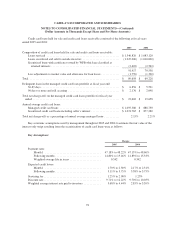

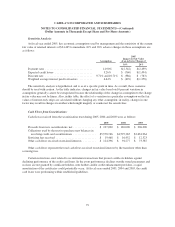

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(Dollar Amounts in Thousands Except Share and Per Share Amounts)

24th day of the month after an account becomes 115 days contractually past due, except in the case of cardholder

bankruptcies, cardholder deaths and fraudulent transactions, which are charged off earlier. Interest income is

accrued on accounts that carry a balance from the statement date through the end of the month.

Cost of Revenue and SG&A Expenses—The Company’s consolidated cost of revenue primarily consists of

merchandise acquisition costs, including freight-in costs, as well as shipping costs. The Company’s consolidated

SG&A expenses primarily consist of selling expense, marketing expenses, including amortization of deferred

catalog costs, warehousing, returned merchandise processing costs, retail occupancy costs, costs of operating our

bank, depreciation, amortization and general and administrative expenses.

Land Held for Sale or Development—The Company owns a fully consolidated subsidiary, whose primary

activity is real estate development. Land that is purchased and held for sale is shown in other assets. Proceeds

from sale of land are recorded in other revenue and the corresponding cost of the land sold is recorded in cost of

revenue.

Cash and Cash Equivalents—Cash equivalents consist of commercial paper and other investments that are

readily convertible into cash and have maturities at date of purchase of three months or less. Unpresented checks

net of bank balance in a single bank account are classified as current liabilities. WFB had $80,569 and $58,147 of

cash and cash equivalents in fiscal years 2005 and 2004, respectively. Due to regulatory restrictions the Company

is restricted from using this cash for non-banking operations, including for working capital for the direct and

retail businesses.

Securitization of Credit Card Loans—WFB sells a substantial portion of its credit card loans. Thus a

majority of the credit card loans are classified as held for sale and are carried at the lower of cost or market. Net

unrealized losses, if any, are recognized through a valuation allowance by charges to income. Although WFB

continues to service the underlying credit card accounts and maintains the customer relationships, these

transactions are treated as sales and the securitized loans are removed from the consolidated balance sheet. WFB

retains certain interests in the loans, including interest-only strips, cash reserve accounts and servicing rights.

Under Statement of Financial Accounting Standards (“SFAS”) No. 140, Accounting for Transfers and

Servicing of Financial Assets and Extinguishments of Liabilities, gains or losses are recognized at the time of

each sale. These gains or losses on sales depend in part on the carrying amount assigned to the loans sold, which

is allocated between the assets sold and retained interest based on their relative fair values at the date of transfer.

For the fiscal years ended 2005, 2004 and 2003, WFB recognized gains on sale of $17,020, $8,864 and $5,894,

respectively, which are reflected as a component of Financial Services revenue.

Since WFB receives adequate compensation relative to current market servicing rates, a servicing asset or

liability is not recognized.

For interest-only strips, WFB uses its best estimates for fair values based on the present value of future

expected cash flows using assumptions for credit losses, payment rates and discount rates commensurate with the

risks involved. The future expected cash flows do not include interchange income since interchange income is

only earned when and if a charge is made to a customer’s account. However, WFB has the rights to the

remaining cash flows (including interchange fees, if any) after the other costs of the trust are paid. Consequently,

interchange income on securitized loans is included within securitization income of Financial Services revenue.

Financial Services revenue is presented in Note 20.

69