Cabela's 2005 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

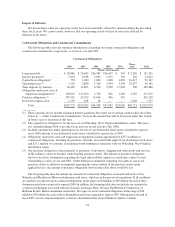

Quarterly Results of Operations and Seasonal Influences

Due to holiday buying patterns and hunting and fishing season openings across the country, merchandise

revenue is typically higher in the third and fourth quarters than in the first and second quarters. We anticipate our

revenue will continue to be seasonal in nature.

The following table sets forth unaudited financial and operating data in each quarter during fiscal years 2005

and 2004. This quarterly information has been prepared on a basis consistent with our audited financial

statements and includes all normal recurring adjustments that we consider necessary for a fair presentation of the

information shown. This information should be read in conjunction with our selected financial data and audited

consolidated financial statements and the notes thereto appearing elsewhere in this report. Our quarterly

operating results may fluctuate significantly as a result of these and a variety of other factors, and operating

results for any quarter are not necessarily indicative of results for a full fiscal year. See “Risk Factors” and

“—Influences on Period Comparability.”

Unaudited

2005 2004

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

First

Quarter

Second

Quarter (1)

Third

Quarter

Fourth

Quarter

(Dollars in thousands except EPS)

Net revenue ..................... $350,589 $343,872 $429,753 $675,447 $313,917 $279,139 $383,810 $579,108

Gross profit ...................... 137,228 135,160 174,759 288,192 125,242 106,853 156,421 241,793

Operating income ................. 11,023 8,822 26,260 68,858 12,703 3,232 25,495 55,785

Net income ...................... 7,767 6,016 16,275 42,511 8,046 1,987 16,503 38,460

Earnings per share—basic (2) ....... $ 0.12 $ 0.09 $ 0.25 $ 0.66 $ 0.14 $ 0.03 $ 0.26 $ 0.60

Earnings per share—diluted (2) ...... $ 0.12 $ 0.09 $ 0.25 $ 0.64 $ 0.14 $ 0.03 $ 0.25 $ 0.58

As a percentage of full year results:

Revenue ........................ 19.5% 19.1% 23.9% 37.5% 20.2% 17.9% 24.7% 37.2%

Gross profit ...................... 18.7% 18.3% 23.8% 39.2% 19.9% 17.0% 24.8% 38.3%

Operating income ................. 9.6% 7.7% 22.8% 59.9% 13.1% 3.3% 26.2% 57.4%

Net income ...................... 10.7% 8.3% 22.4% 58.6% 12.4% 3.1% 25.4% 59.1%

(1) We recognized an offset to revenue in the second fiscal quarter of fiscal 2004 of $3.1 million as a result of the completion of a

securitization transaction in our Financial Services segment in that quarter.

(2) Basic and diluted earnings per share are computed independently for each of the quarters presented. Due to our initial public offering in

2004, the sum of the fiscal 2004 quarterly earnings per share may not total the amounts for fiscal 2004.

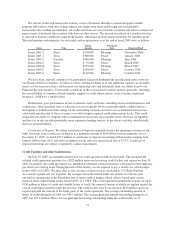

Bank Asset Quality

We securitize a majority of our credit card loans. On a quarterly basis, we transfer eligible credit card loans

into a securitization trust. We are required to own at least a minimum twenty day average of 5% of the interests

in the securitization trust. Therefore, these retained loans have the same characteristics as those loans sold to

outside investors. Certain accounts are ineligible for securitization because they are delinquent at the time of

sales to the trust, originated from sources other than Cabela’s Club credit cards and various other requirements.

The total amount of ineligible loans and receivables were $14.1 million and $6.1 million at fiscal year end 2005

and fiscal year end 2004, respectively. Of the $14.1 million outstanding at fiscal year end 2005, $12.6 million

originated from sources other than Cabela’s Club credit cards. The following table shows credit card loans

available for sale along with those securitized as of fiscal year end 2005, 2004 and 2003:

2005 2004 2003

Loans

Outstanding

>90 Days

Delinquent

Loans

Outstanding

>90 Days

Delinquent

Loans

Outstanding

>90 Days

Delinquent

Loans held for sale (median FICO score of 775 in 2005

and 776 in 2004) .............................. $ 8,606 — $ 4,202 — $ 4,223 —

Loans securitized and transferor’s interest (median FICO

score of 778 in 2005; and 774 in 2004) ............. 1,318,140 $1,752 1,072,910 $1,808 867,982 $1,433

Total .......................................... $1,326,746 $1,752 $1,077,112 $1,808 $872,205 $1,433

44