Cabela's 2005 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2005 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

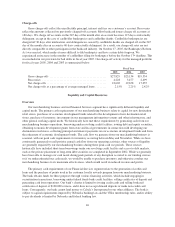

As reflected in the preceding table, the credit quality of our reported credit card loans does not have a

significant effect on the overall quality of our entire managed portfolio. As a result, we generally only monitor

the asset quality of the managed portfolio.

The quality of our managed credit card loan portfolio at any time reflects, among other factors, the

creditworthiness of the individual cardholders, general economic conditions, the success of our account

management and collection activities, and the life cycle stage of the portfolio. Our financial results are sensitive

to changes in delinquencies and net charge-offs of this portfolio. During periods of economic weakness,

delinquencies and net charge-offs are more likely to increase. We have sought to manage this sensitivity by

selecting a customer base that has historically shown itself to be very creditworthy based on charge-off levels,

credit bureau scores such as Fair Isaac & Company (“FICO”) scores and behavior scores.

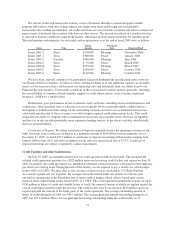

Our average managed credit card loans outstanding increased by $207 million, or 23.3%, to $1,096 million

in fiscal 2005 from $889 million in fiscal 2004. We believe that as credit card accounts mature they are less

likely to charge-off and less likely to be closed. The following table shows our managed loans outstanding at

fiscal year end 2005 and 2004 by months since the account opened.

2005 2004

Loans

Outstanding

Percentage of

Total

Loans

Outstanding

Percentage of

Total

(Dollars in thousands)

Months Since Account Opened

6 months or Less ................................ $ 87,394 6.5% $ 53,803 5.0%

7 – 12 months .................................. 83,531 6.2 70,600 6.5

13 – 24 months .................................. 170,864 12.7 155,500 14.4

25 – 36 months .................................. 170,886 12.8 169,804 15.7

37 – 48 months .................................. 178,980 13.3 183,254 16.9

49 – 60 months .................................. 190,011 14.2 233,624 21.5

61 – 72 months .................................. 240,743 18.0 82,640 7.6

73 – 84 months .................................. 83,701 6.3 28,514 2.6

85 + months .................................... 134,710 10.0 105,381 9.8

Total ...................................... $1,340,820 100.0% $1,083,120 100.0%

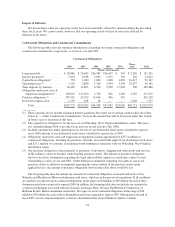

Delinquencies

We consider the entire balance of an account, including any accrued interest and fees, delinquent if the

minimum payment is not received by the payment due date. Our aging methodology is based on the number of

completed billing cycles during which a customer has failed to make a required payment. Delinquencies not only

have the potential to reduce earnings by increasing the unrealized loss recognized to reduce the loans to market

value and reducing securitization income, but they also result in additional operating costs dedicated to resolving

the delinquencies. The following chart shows the percentage of our managed loans that have been delinquent as

of the end of fiscal years 2005, 2004 and 2003.

Fiscal Year

2005 2004 2003

Number of days delinquent

Greater than 30 days ................................. 0.67% 0.71% 0.80%

Greater than 60 days ................................. 0.38% 0.41% 0.43%

Greater than 90 days ................................. 0.16% 0.19% 0.18%

45