Sysco 2010 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2010 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

provision which allows Sysco to retire the notes at any time prior to maturity at the greater of par plus accrued interest or an amount designed to

ensure that the note holders are not penalized by early redemption. Proceeds from the notes will be utilized over a period of time for general

corporate purposes, which may include acquisitions, refinancing of debt, working capital, share repurchases and capital expenditures.

In September 2009, we entered into an interest rate swap agreement that effectively converted $200.0 million of fixed rate debt maturing in

fiscal 2014 to floating rate debt. In October 2009, we entered into an interest rate swap agreement that effectively converted $250.0 million of fixed

rate debt maturing in fiscal 2013 to floating rate debt. Both transactions were entered into with the goal of reducing overall borrowing cost and

increasing floating interest rate exposure.These transactions were designated as fair value hedges since the swaps hedge against the changes in fair

value of fixed rate debt resulting from changes in interest rates.

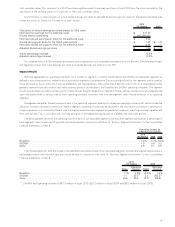

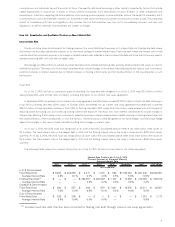

Total Debt

Total debt as of July 3, 2010 was $2.5 billion of which approximately 81% was at fixed rates with a weighted average of 5.9% and an average life

of 16 years, and the remainder was at floating rates with a weighted average of 2.3%. Certain loan agreements contain typical debt covenants to

protect note holders, including provisions to maintain the company’s long-term debt to total capital ratio below a specified level. Sysco was in

compliance with all debt covenants as of July 3, 2010.

Other

As part of normal business activities, we issue letters of credit through major banking institutions as required by certain vendor and insurance

agreements. As of July 3, 2010 and June 27, 2009, letters of credit outstanding were $28.4 million and $74.7 million, respectively.

Other Considerations

Multi-Employer Pension Plans

As discussed in Note 18, “Commitments and Contingencies”, to the Consolidated Financial Statements in Item 8, we contribute to several

multi-employer defined benefit pension plans based on obligations arising under collective bargaining agreements covering union-represented

employees.

Under current law regarding multi-employer defined benefit plans, a plan’s termination, our voluntary withdrawal or the mass withdrawal of all

contributing employers from any underfunded multi-employer defined benefit plan would require us to make payments to the plan for our

proportionate share of the multi-employer plan’s unfunded vested liabilities. Generally, Sysco does not have the greatest share of liability among the

participants in any of these plans. Based on the information available from plan administrators, which has valuation dates ranging from January 31,

2008 to June 30, 2009, we estimate our share of withdrawal liability on most of the multi-employer plans in which we participate could have been as

much as $183.0 million as of July 3, 2010 based on a voluntary withdrawal. The majority of the plans we participate in have a valuation date of

calendar year-end. As such, the majority of our estimated withdrawal liability results from plans for which the valuation date was December 31,

2008; therefore, our estimated liability reflects the asset losses incurred by the financial markets as of that date. In general, the financial markets

improved during calendar year 2009; therefore, we believe our current share of the withdrawal liability could differ from this estimate. In addition,ifa

multi-employer defined benefit plan fails to satisfy certain minimum funding requirements, the IRS may impose a non-deductible excise tax of 5% on

the amount of the accumulated funding deficiency for those employers contributing to the fund. As of July 3, 2010, we have approximately

$0.9 million in liabilities recorded in total related to certain multi-employer defined benefit plans for which our voluntary withdrawal had already

occurred.

Required contributions to multi-employer plans could increase in the future as these plans strive to improve their funding levels. In addition, the

Pension Protection Act, enacted in August 2006, requires underfunded pension plans to improve their funding ratios within prescribed intervals

based on the level of their underfunding. We believe that any unforeseen requirements to pay such increased contributions, withdrawal liability and

excise taxes would be funded through cash flow from operations, borrowing capacity or a combination of these items.

During fiscal 2008, we obtained information that a multi-employer pension plan we participated in failed to satisfy minimum funding

requirements for certain periods and concluded that it was probable that additional funding would be required as well as the payment of excise tax.

As a result, during fiscal 2008, we recorded a liability of approximately $16.5 million related to our share of the minimum funding requirements and

related excise tax for these periods. During the first quarter of fiscal 2009, we effectively withdrew from this multi-employer pension plan in an effort

to secure benefits for our employees that were participants in the plan and to manage our exposure to this under-funded plan. We agreed to pay

$15.0 million to the plan, which included the minimum funding requirements. In connection with this withdrawal agreement, we merged active

participants from this plan into Sysco’s company-sponsored Retirement Plan and assumed $26.7 million in liabilities. The payment to the plan was

made in the early part of the second quarter of fiscal 2009. If this plan were to undergo a mass withdrawal, as defined by the Pension Benefit

Guaranty Corporation, prior to September 2010, we could have additional liability. We do not currently believe a mass withdrawal from this plan prior

to September 2010 is probable.

We have experienced other instances triggering voluntary withdrawal from multi-employer pension plans. Total withdrawal liability provisions

recorded include $2.9 million in fiscal 2010, $9.6 million in fiscal 2009 and $22.3 million in fiscal 2008.

25