Sysco 2010 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2010 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

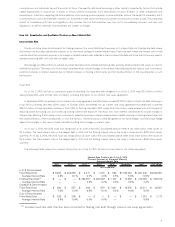

in the discount rates would increase pension cost by $61.7 million. The impact of a 100 basis point increase in the discount rates differs from the

impact of a 100 basis point decrease in discount rates because the liabilities are less sensitive to change at higher discount rates. Therefore, a

100 basis point increase in the discount rate will not generate the same magnitude of change as a 100 basis point decrease in the discount rate.

We look to actual plan experience in determining the rates of increase in compensation levels. We used a plan specific age-related set of rates

for the Retirement Plan, which are equivalent to a single rate of 5.30% as of July 3, 2010 and 5.21% as of June 27, 2009. For determining the benefit

obligations as of July 3, 2010, the SERP calculations use an age-graded salary growth assumption. As of June 27, 2009, the SERP calculations use an

age-graded salary growth assumption with reductions taken for determining fiscal 2010 pay due to base salary freezes in effect for fiscal 2010.

The expected long-term rate of return on plan assets of the Retirement Plan was 8.00% for fiscal 2010 and fiscal 2009. The expectations of

future returns are derived from a mathematical asset model that incorporates assumptions as to the various asset class returns, reflecting a

combination of historical performance analysis and the forward-looking views of the financial markets regarding the yield on bonds, historical

returns of the major stock markets and returns on alternative investments. Although not determinative of future returns, the effective annual rate of

return on plan assets, developed using geometric/compound averaging, was approximately 7.1%, 2.5%, 1.8%, and 19.5%, over the 20-year, 10-year,

5-year and 1-year periods ended December 31, 2009, respectively. In addition, in nine of the last 15 years, the actual return on plan assets has

exceeded 10.0%. The rate of return assumption is reviewed annually and revised as deemed appropriate.

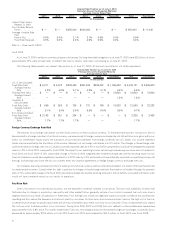

The expected return on plan assets impacts the recorded amount of net pension costs. The expected long-term rate of return on plan assets of

the Retirement Plan is 8.00% for fiscal 2011. A 100 basis point increase (decrease) in the assumed rate of return for fiscal 2011 would decrease

(increase) Sysco’s net company-sponsored pension costs for fiscal 2011 by approximately $16.5 million.

Pension accounting standards require the recognition of the funded status of our defined benefit plans in the statement of financial position,

with a corresponding adjustment to accumulated other comprehensive income, net of tax. The amount reflected in accumulated other compre-

hensive loss related to the recognition of the funded status of our defined benefit plans as of July 3, 2010 was a charge, net of tax, of $598.8 million.

The amount reflected in accumulated other comprehensive loss related to the recognition of the funded status of our defined benefit plans as of

June 27, 2009 was a charge, net of tax, of $346.1 million.

Changes in the assumptions, including changes to the discount rate discussed above, together with the normal growth of the plans, the impact

of actuarial losses from prior periods and the timing and amount of contributions, increased net company-sponsored pension costs by approximately

$37.4 million in fiscal 2010. Changes in the assumptions, including changes to the discount rate discussed above, together with the normal growth of

the plans, the impact of actuarial losses from prior periods and the timing and amount of contributions are expected to increase net company-

sponsored pension costs in fiscal 2011 by approximately $60.3 million.

We made cash contributions to our company-sponsored pension plans of $297.9 million and $95.8 million in fiscal years 2010 and 2009,

respectively. The contributions in fiscal 2010 of $280.0 million to the Retirement Plan included the minimum required contribution for the calendar

2009 plan year to meet ERISA minimum funding requirements. The contributions in fiscal 2009 of $80.0 million to the Retirement Plan were

voluntary contributions. We do not have a minimum required contribution to the Retirement Plan for the calendar 2010 plan year to meet ERISA

minimum funding requirements. We contributed $140.0 million to the Retirement Plan in fiscal 2010 for contributions that would normally have

been made in fiscal 2011. Additional contributions to the Retirement Plan are not currently anticipated in fiscal 2011. The estimated fiscal 2011

contributions to fund benefit payments for the SERP plan is approximately $22.2 million.

Income Taxes

The determination of our provision for income taxes requires significant judgment, the use of estimates and the interpretation and application of

complex tax laws. Our provision for income taxes primarily reflects a combination of income earned and taxed in the various U.S. federal and state, as

well as foreign jurisdictions. Jurisdictional tax law changes, increases or decreases in permanent differences between book and tax items, accrualsor

adjustments of accruals for unrecognized tax benefits or valuation allowances, and our change in the mix of earnings from these taxing jurisdictions

all affect the overall effective tax rate.

Our liability for unrecognized tax benefits contains uncertainties because management is required to make assumptions and to apply judgment

to estimate the exposures associated with our various filing positions. We believe that the judgments and estimates discussed herein are reasonable;

however, actual results could differ, and we may be exposed to losses or gains that could be material.To the extent we prevail in matters for which a

liability has been established, or pay amounts in excess of recorded liabilities, our effective income tax rate in a given financial statement period could

be materially affected. An unfavorable tax settlement generally would require use of our cash and may result in an increase in our effective income

tax rate in the period of resolution. A favorable tax settlement may be recognized as a reduction in our effective income tax rate in the period of

resolution.

Vendor Consideration

We recognize consideration received from vendors when the services performed in connection with the monies received are completed and

when the related product has been sold by Sysco.There are several types of cash consideration received from vendors. In many instances, the vendor

consideration is in the form of a specified amount per case or per pound. In these instances, we will recognize the vendor consideration as a reduction

of cost of sales when the product is sold. In some instances, vendor consideration is received upon receipt of inventory in our distribution facilities.

We estimate the amount needed to reduce our inventory based on inventory turns until the product is sold. Our inventory turnover is usually less

28