Sysco 2010 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2010 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

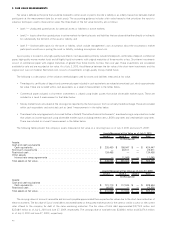

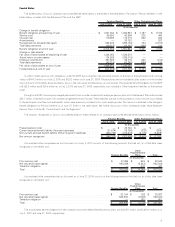

Shipping and Handling Costs

Shipping and handling costs include costs associated with the selection of products and delivery to customers. Included in operating expenses

are shipping and handling costs of approximately $2,103.3 million in fiscal 2010, $2,136.8 million in fiscal 2009, and $2,155.8 million in fiscal 2008.

Insurance Program

Sysco maintains a self-insurance program covering portions of workers’ compensation, general and vehicle liability costs. The amounts in

excess of the self-insured levels are fully insured by third party insurers. The company also maintains a fully self-insured group medical program.

Liabilities associated with these risks are estimated in part by considering historical claims experience, medical cost trends, demographic factors,

severity factors and other actuarial assumptions.

Share-Based Compensation

Sysco recognizes expense for its share-based compensation based on the fair value of the awards that are granted. The fair value of stock

options is estimated at the date of grant using the Black-Scholes option pricing model. Option pricing methods require the input of highly subjective

assumptions, including the expected stock price volatility. The fair value of restricted stock and restricted stock unit awards are based on the

company’s stock price on the date of grant. Measured compensation cost is recognized ratably over the vesting period of the related share-based

compensation award. Cash flows resulting from tax deductions in excess of the compensation cost recognized for those options (excess tax

benefits) are classified as financing cash flows on the consolidated cash flows statements.

Acquisitions

Acquisitions of businesses are accounted for using the purchase method of accounting, and the financial statements include the results of the

acquired operations from the respective dates of acquisition.

The purchase price of the acquired entities is allocated to the net assets acquired and liabilities assumed based on the estimated fair value at the

dates of acquisition, with any excess of cost over the fair value of net assets acquired, including intangibles, recognized as goodwill. The balances

included in the consolidated balance sheets related to recent acquisitions are based upon preliminary information and are subject to change when

final asset and liability valuations are obtained. Subsequent changes to the preliminary balances are reflected retrospectively, if material. Material

changes to the preliminary allocations are not anticipated by management.

Reclassifications

Prior year amounts within the consolidated balance sheets and consolidated cash flows have been reclassified to conform to the current year

presentation as it relates to the presentation of cash and accounts payable within these statements. The impact of these reclassifications were

immaterial to all periods presented.

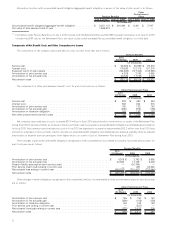

2. CHANGES IN ACCOUNTING

Fair Value Measurements

In September 2006, the Financial Accounting Standards Board (FASB) issued FASB Statement No. 157, “Fair Value Measurements”, which was

subsequently codified within Accounting Standards Codification (ASC) 820, “Fair Value Measurements.” This standard established a common

definition for fair value under generally accepted accounting principles, established a framework for measuring fair value and expanded disclosure

requirements about such fair value measurements. As of June 29, 2008, Sysco adopted the provisions of this fair value measurement guidance for

financial assets and liabilities carried at fair value and non-financial assets and liabilities that are recognized or disclosed at fair value on a recurring

basis.

The adoption of the fair value measurement provisions for financial assets and liabilities carried at fair value and non-financial assets and

liabilities that are recognized or disclosed at fair value on a recurring basis did not have a material impact on the company’s financial statements. As

of June 28, 2009, Sysco adopted the provisions of this fair value measurements guidance for non-recurring, non-financial assets and liabilities that

are recognized or disclosed at fair value. Sysco’s only non-recurring, non-financial asset fair value measurements are those used in its annual test of

recoverability of goodwill and indefinite-lived intangibles, in which it determines whether estimated fair values of the applicable reporting units

exceed their carrying values. The fair value measurements guidance was applied beginning in fiscal 2010 to this fair value estimation.

Disclosure About Derivative Instruments and Hedging Activities

In March 2008, the FASB issued FASB Statement No. 161, “Disclosure about Derivative Instruments and Hedging Activities, an amendment of

FASB Statement No. 133,” which was subsequently codified within ASC 815, “Derivatives and Hedging”. Effective for Sysco in the third quarter of

fiscal 2009, this standard requires enhanced disclosures about an entity’s derivative and hedging activities and thereby improves the transparencyof

financial reporting. Sysco has provided the required disclosures for this standard in Note 8, “Derivative Financial Instruments.”

44