Sysco 2010 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2010 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

BSCC Cooperative Structure

Sysco’s affiliate, Baugh Supply Chain Cooperative (BSCC), is a cooperative taxed under subchapter T of the United States Internal Revenue

Code, the operation of which has resulted in a deferral of tax payments. The IRS, in connection with its audits of our 2003 through 2006 federal

income tax returns, proposed adjustments that would have accelerated amounts that we had previously deferred and would have resulted in the

payment of interest on those deferred amounts. Sysco reached a settlement with the IRS in the first quarter of fiscal 2010 to cease paying U.S. federal

taxes related to BSCC on a deferred basis, pay the amounts that were recorded within deferred taxes related to BSCC over a three-year period and

make a one-time payment of $41.0 million, of which approximately $39.0 million is non-deductible.The settlement addresses the BSCC deferred tax

issue as it relates to the IRS audit of our 2003 through 2006 federal income tax returns, and settles the matter for all subsequent periods, including

the 2007 and 2008 federal income tax returns already under audit. As a result of the settlement, we will pay the amounts owed in the following

schedule:

Amounts paid annually: (In thousands)

Fiscal 2010 . . .................................................................................... $ 528,000

Fiscal 2011 . . . .................................................................................... 212,000

Fiscal 2012 . . .................................................................................... 212,000

As noted in the table above, $528.0 million was paid related to settlement in fiscal 2010. Amounts to be paid in fiscal 2011 and 2012 will be paid

in connection with our quarterly tax payments, two of which fall in the second quarter, one in the third quarter and one in the fourth quarter. We

believe we have access to sufficient cash on hand, cash flows from operations and current access to capital to make payments on all of the amounts

noted above.

Off-Balance Sheet Arrangements

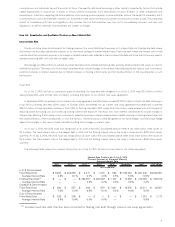

We have no off-balance sheet arrangements.

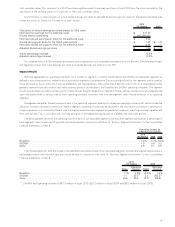

Contractual Obligations

The following table sets forth, as of July 3, 2010, certain information concerning our obligations and commitments to make contractual future

payments:

Total G1 Year 1-3 Years 3-5 Years

More Than

5 Years

Payments Due by Period

(In thousands)

Recorded Contractual Obligations:

Long-term debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 2,441,372 $ 196 $ 453,130 $ 209,493 $ 1,778,553

Capital lease obligations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39,260 7,774 8,906 3,723 18,857

Deferred compensation

(1)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . 93,022 14,271 18,672 11,572 48,507

SERP and other postretirement plans

(2)

. . . . . . . . . . . . . . . . . . . 271,488 22,592 47,692 51,515 149,689

Unrecognized tax benefits and interest

(3)

. . . . . . . . . . . . . . . . . . 130,445 24,624

IRS deferred tax settlement

(3)

. . . . . . . . . . . . . . . . . . . . . . . . . 424,000 212,000 212,000 — —

Unrecorded Contractual Obligations:

Interest payments related to commercial paper and debt

(4)

. . . . . . 1,453,115 125,005 237,809 207,957 882,344

Retirement plan

(5)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,035,593 — 283,287 277,569 474,737

Long-term non-capitalized leases . . . . . . . . . . . . . . . . . . . . . . . 212,646 48,845 67,412 41,333 55,056

Purchase obligations

(6)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,863,973 1,378,397 358,231 127,345 —

Total contractual cash obligations . . . . . . . . . . . . . . . . . . . . . $ 7,964,914 $ 1,833,704 $ 1,687,139 $ 930,507 $ 3,407,743

(1)

The estimate of the timing of future payments under the Executive Deferred Compensation Plan involves the use of certain

assumptions, including retirement ages and payout periods.

(2)

Includes estimated contributions to the unfunded SERP and other postretirement benefit plans made in amounts needed to fund benefit

payments for vested participants in these plans through fiscal 2020, based on actuarial assumptions.

(3)

Unrecognized tax benefits relate to uncertain tax positions recorded under accounting standards related to uncertain tax positions. As

of July 3, 2010, we had a liability of $89.9 million for unrecognized tax benefits for all tax jurisdictions and $40.6 million for related

interest that could result in cash payment, of which $24.6 million is expected to be paid during fiscal 2011. Sysco reached a settlement

with the IRS in the first quarter of fiscal 2010 related to timing of tax payments. Apart from these items, we are not able to reasonably

estimate the timing of non-current payments or the amount by which the liability will increase or decrease over time. Accordingly, the

related non-current balances have not been reflected in the “Payments Due by Period” section of the table.

(4)

Includes payments on floating rate debt based on rates as of July 3, 2010, assuming amount remains unchanged until maturity, and

payments on fixed rate debt based on maturity dates. The impact of our outstanding fixed-to-floating interest rate swaps on the fixed

rate debt interest payments is included as well based on the floating rates in effect as of July 3, 2010.

(5)

Provides the estimated minimum contribution to the Retirement Plan through fiscal 2020 to meet ERISA minimum funding

requirements under the assumption that we only make minimum funding requirement contributions each year, based on actuarial

assumptions.

26