Sysco 2010 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2010 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

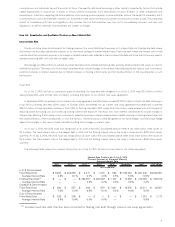

than one month; therefore, amounts deferred against inventory do not require long-term estimation. In the situations where the vendor consideration

is not related directly to specific product purchases, we will recognize these as a reduction of cost of sales when the earnings process is complete, the

related service is performed and the amounts realized. Historically, adjustments to our estimates related to vendor consideration have not been

significant.

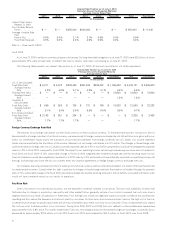

Goodwill and Intangible Assets

Goodwill and intangible assets represent the excess of consideration paid over the fair value of tangible net assets acquired. Certain

assumptions and estimates are employed in determining the fair value of assets acquired, including goodwill and other intangible assets, as well as

determining the allocation of goodwill to the appropriate reporting unit.

In addition, annually or more frequently as needed, we assess the recoverability of goodwill and indefinite-lived intangibles by determining

whether the fair values of the applicable reporting units exceed the carrying values of these assets. The reporting units used in assessing goodwill

impairment are our eight operating segments as described in Note 19, “Business Segment Information,” to the Consolidated Financial Statements in

Item 8. The components within each of our eight operating segments have similar economic characteristics and therefore are aggregated into eight

reporting units.

We arrive at our estimates of fair value using a combination of discounted cash flow and earnings multiple models. The results from each of

these models are then weighted and combined into a single estimate of fair value for each of our eight operating segments.The primary assumptions

used in these various models include estimated earnings multiples of comparable acquisitions in the industry including control premiums, earnings

multiples on acquisitions completed by Sysco in the past, future cash flow estimates of the reporting units, which are dependent on internal forecasts

and projected growth rates, and weighted average cost of capital, along with working capital and capital expenditure requirements. When possible,

we use observable market inputs in our models to arrive at the fair values of our reporting units. We update our projections used in our discounted

cash flow model based on historical performance and changing business conditions for each of our reporting units.

Actual results could differ from these assumptions and projections, resulting in the company revising its assumptions and, if required,

recognizing an impairment loss. There were no impairments of goodwill or indefinite-lived intangibles recorded as a result of assessment in fiscal

2010, 2009 and 2008. Our past estimates of fair value for fiscal 2010, 2009 and 2008 have not been materially different when revised to include

subsequent years’ actual results. Sysco has not made any material changes in its impairment assessment methodology during the past three fiscal

years. We do not believe the estimates used in the analysis are reasonably likely to change materially in the future but we will continue to assess the

estimates in the future based on the expectations of the reporting units. In the fiscal 2010 analysis, we would have performed additional analysis to

determine if an impairment existed for our lodging industry products reporting unit if the estimated fair value for this reporting unit had been 20%

lower. For the remainder of our reporting units, we would have performed additional analysis to determine if an impairment existed for a reporting

unit if the estimated fair value for any of these reporting units had declined by greater than 40%.

The reporting units aggregated as “Other” in the financial statement disclosures (specialty produce, custom-cut meat, lodging industry

products and international distribution operations) have a greater proportion of goodwill recorded to estimated fair value as compared to the

Broadline or SYGMA reporting units. This is primarily due to these businesses having been recently acquired, and as a result there has been less

history of organic growth than in the Broadline and SYGMA reporting units. In addition, these businesses also have lower levels of cash flow than the

Broadline reporting units. As such, these “Other” reporting units have a greater risk of future impairment if their operations were to suffer a

significant downturn.

Share-Based Compensation

We provide compensation benefits to employees and non-employee directors under several share-based payment arrangements including

various employee stock incentive plans, the Employees’ Stock Purchase Plan, the Management Incentive Plan and various non-employee director

plans.

As of July 3, 2010, there was $66.2 million of total unrecognized compensation cost related to share-based compensation arrangements. That

cost is expected to be recognized over a weighted-average period of 2.76 years.

The fair value of each option award is estimated on the date of grant using a Black-Scholes option pricing model. Expected volatility is based on

historical volatility of Sysco’s stock, implied volatilities from traded options on Sysco’s stock and other factors. We utilize historical data to estimate

option exercise and employee termination behavior within the valuation model; separate groups of employees that have similar historical exercise

behavior are considered separately for valuation purposes. Expected dividend yield is estimated based on the historical pattern of dividends and the

average stock price for the year preceding the option grant. The risk-free rate for the expected term of the option is based on the U.S. Treasury yield

curve in effect at the time of grant.

The fair value of each restricted stock unit award granted with a dividend equivalent is based on the company’s stock price as of the date of

grant. For restricted stock units granted without dividend equivalents, the fair value is reduced by the present value of expected dividends during the

vesting period.

The fair value of the stock issued under the Employee Stock Purchase Plan is calculated as the difference between the stock price and the

employee purchase price.

29