Sysco 2010 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2010 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

For guidance in determining the discount rate, Sysco calculates the implied rate of return on a hypothetical portfolio of high-quality fixed-

income investments for which the timing and amount of cash outflows approximates the estimated payouts of the company-sponsored pension

plans.The discount rate assumption is reviewed annually and revised as deemed appropriate.The discount rate to be used for the calculation of fiscal

2011 net company-sponsored benefit costs for the Retirement Plan is 6.15%. The discount rate to be used for the calculation of fiscal 2011 net

company-sponsored benefit costs for the SERP is 6.35%. The discount rate to be used for the calculation of fiscal 2011 net company-sponsored

benefit costs for the Other Postretirement Plans is 6.32%.

The expected long-term rate of return on plan assets is derived from a mathematical asset model that incorporates assumptions as to the

various asset class returns, reflecting a combination of rigorous historical performance analysis and the forward-looking views of the financial

markets regarding the yield on bonds, the historical returns of the major stock markets and returns on alternative investments. The rate of return

assumption is reviewed annually and revised as deemed appropriate. In fiscal 2009, the expected long-term rate of return on plan assets assumption

was changed to a net return on assets assumption, which contributed to the 0.50% decrease in the assumption to 8.00% in fiscal 2009. Prior to

fiscal 2009, this assumption represented gross return on assets, and plan expenses were reflected within service cost. Due to this change, beginning

in fiscal 2009, actual expenses are no longer reflected in the change in benefit obligation and change in plan assets sections of funded status table

above.The expected long-term rate of return to be used in the calculation of fiscal 2011 net company-sponsored benefit costs for the Retirement Plan

is 8.00%.

Plan Assets

Investment Strategy

The company’s overall strategic investment objectives for the Retirement Plan are to preserve capital for future benefit payments and to balance

risk and return. In order to accomplish these objectives, the company oversees the Retirement Plan’s investment objectives and policy design,

decides proper plan asset class strategies and structures, monitors the performance of plan investment managers and investment funds and

determines the proper investment allocation of pension plan contributions and withdrawals.The company has created a set of investment guidelines

for the Retirement Plan’s investment managers.These guidelines are tailored to the investment strategy of each manager and state limits of holdings

in any single issuer, industry or country and also the minimum number of holdings for each portfolio. These guidelines also specify prohibited

transactions, including borrowing of money except for real estate portfolios or opportunistic funds, the purchase of securities on margin unless fully

collateralized by cash or cash equivalents or short sales, pledging or mortgaging of any securities except for loans of securities that are fully

collateralized, market timing transactions and the purchase of the securities of Sysco or the investment manager. The purchase or sale of derivatives

for speculation or leverage is also prohibited; however, investment managers are allowed to use derivative securities so long as they do not increase

the risk profile or leverage of the manager’s portfolio.

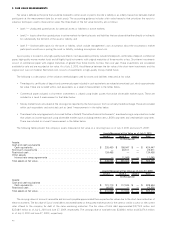

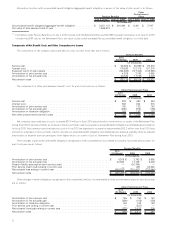

The company’s target and actual investment allocation as of July 3, 2010 is as follows:

Target Asset

Allocation Range

Actual Asset

Allocation

U.S. equity .............................................................. 23-31% 37%

International equity ......................................................... 23-31 18

Fixed income long duration ................................................... 23-31 37

Fixed income high yield...................................................... 6-12 7

Alternative investments ..................................................... 3-13 1

100%

Sysco’s investment strategy is implemented through a combination of balanced and specialist investment managers, passive investment funds

and actively-managed investment funds. U.S. equity consists of both large-cap and small-to-mid-cap securities. Fixed income long duration

investments include U.S. government and agency securities, corporate bonds from diversified industries, asset-backed securities, mortgage-backed

securities, other debt securities and derivative securities. Fixed income high yield consists of below investment grade corporate debt securities and

may include derivative securities. Alternative investments may include private equity, private real estate, timberland, and commodities investments.

Investment funds are selected based on each fund’s stated investment strategy to align with Sysco’s overall target mix of investments. Actual asset

allocation is regularly reviewed and periodically rebalanced to the target allocation when considered appropriate. As of July 3, 2010, actual asset

allocation varied significantly from the stated target in certain categories, as the company had recently completed an asset allocation study and

rebalancing of the portfolio to the revised target allocation range was not yet complete as of July 3, 2010.

As discussed above, the Retirement Plan’s investments in equity, fixed income and real estate provide a range of returns and also expose the

plan to investment risk. However, the investment policies put in place by the company require diversification of plan assets across issuers, industries

and countries. As such, the Retirement Plan does not have significant concentrations of risk in plan assets.

Fair Value of Plan Assets

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market

participants at the measurement date (i.e. an exit price). See Note 3, “Fair Value Measurements,” for a description of the fair value hierarchy that

prioritizes the inputs to valuation techniques used to measure fair value. The following is a description of the valuation methodologies used for assets

and liabilities measured at fair value.

54