Sysco 2010 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2010 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

(6)

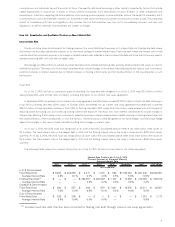

For purposes of this table, purchase obligations include agreements for purchases of product in the normal course of business, for which

all significant terms have been confirmed, including minimum quantities resulting from our sourcing initiative. Such amounts included

in the table above are based on estimates. Purchase obligations also includes amounts committed with a third party to provide

hardware and hardware hosting services over a ten year period ending in fiscal 2015 (See discussion under Note 18, “Commitments and

Contingencies”, to the Notes to Consolidated Financial Statements in Item 8), fixed electricity agreements and fixed fuel purchase

commitments. Purchase obligations exclude full requirements electricity contracts where no stated minimum purchase volume is

required.

Certain acquisitions involve contingent consideration, typically payable only in the event that certain operating results are attained or certain

outstanding contingencies are resolved. Aggregate contingent consideration amounts outstanding as of July 3, 2010 included $52.8 million in cash.

This amount is not included in the table above.

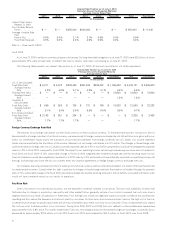

Critical Accounting Policies and Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires us to make estimates and

assumptions that affect the reported amounts of assets, liabilities, sales and expenses in the accompanying financial statements. Significant

accounting policies employed by Sysco are presented in the notes to the financial statements.

Critical accounting policies and estimates are those that are most important to the portrayal of our financial condition and results of operations.

These policies require our most subjective or complex judgments, often employing the use of estimates about the effect of matters that are

inherently uncertain. We have reviewed with the Audit Committee of the Board of Directors the development and selection of the critical accounting

policies and estimates and this related disclosure. Our most critical accounting policies and estimates pertain to the allowance for doubtful accounts

receivable, self-insurance programs, company-sponsored pension plans, income taxes, vendor consideration, goodwill and intangible assets and

share-based compensation.

Allowance for Doubtful Accounts

We evaluate the collectability of accounts receivable and determine the appropriate reserve for doubtful accounts based on a combination of

factors. We utilize specific criteria to determine uncollectible receivables to be written off, including whether a customer has filed for or has been

placed in bankruptcy, has had accounts referred to outside parties for collection or has had accounts past due over specified periods. Allowances are

recorded for all other receivables based on analysis of historical trends of write-offs and recoveries. In addition, in circumstances where we are aware

of a specific customer’s inability to meet its financial obligation, a specific allowance for doubtful accounts is recorded to reduce the receivable to the

net amount reasonably expected to be collected. Our judgment is required as to the impact of certain of these items and other factors as to ultimate

realization of our accounts receivable. If the financial condition of our customers were to deteriorate, as was the case in fiscal 2009, additional

allowances may be required.

Self-Insurance Program

We maintain a self-insurance program covering portions of workers’ compensation, general liability and vehicle liability costs. The amounts in

excess of the self-insured levels are fully insured by third party insurers. We also maintain a fully self-insured group medical program. Liabilities

associated with these risks are estimated in part by considering historical claims experience, medical cost trends, demographic factors, severity

factors and other actuarial assumptions. Projections of future loss expenses are inherently uncertain because of the random nature of insurance

claims occurrences and could be significantly affected if future occurrences and claims differ from these assumptions and historical trends. In an

attempt to mitigate the risks of workers’ compensation, vehicle and general liability claims, safety procedures and awareness programs have been

implemented.

Company-Sponsored Pension Plans

Amounts related to defined benefit plans recognized in the financial statements are determined on an actuarial basis. Three of the more critical

assumptions in the actuarial calculations are the discount rate for determining the current value of plan benefits, the assumption for the rate of

increase in future compensation levels and the expected rate of return on plan assets.

For guidance in determining the discount rates, we calculate the implied rate of return on a hypothetical portfolio of high-quality fixed-income

investments for which the timing and amount of cash outflows approximates the estimated payouts of the pension plan. The discount rate

assumption is reviewed annually and revised as deemed appropriate. The discount rate for determining fiscal 2010 net pension costs for the

Retirement Plan, which was determined as of the June 27, 2009 measurement date, increased 108 basis points to 8.02%. The discount rate for

determining fiscal 2010 net pension costs for the SERP, which was determined as of the June 27, 2009 measurement date, increased 11 basis points

to 7.14%.The combined effect of these discount rate changes decreased our net company-sponsored pension costs for all plans for fiscal 2010 by an

estimated $38.6 million. The discount rate for determining fiscal 2011 net pension costs for the Retirement Plan, which was determined as of the

July 3, 2010 measurement date, decreased 187 basis points to 6.15%. The discount rate for determining fiscal 2011 net pension costs for the SERP,

which was determined as of the July 3, 2010 measurement date, decreased 79 basis points to 6.35%. The combined effect of these discount rate

changes will increase our net company-sponsored pension costs for all plans for fiscal 2011 by an estimated $85.6 million. A 100 basis point increase

in the discount rates for fiscal 2011 would decrease Sysco’s net company-sponsored pension cost by $50.9 million, while a 100 basis point decrease

27